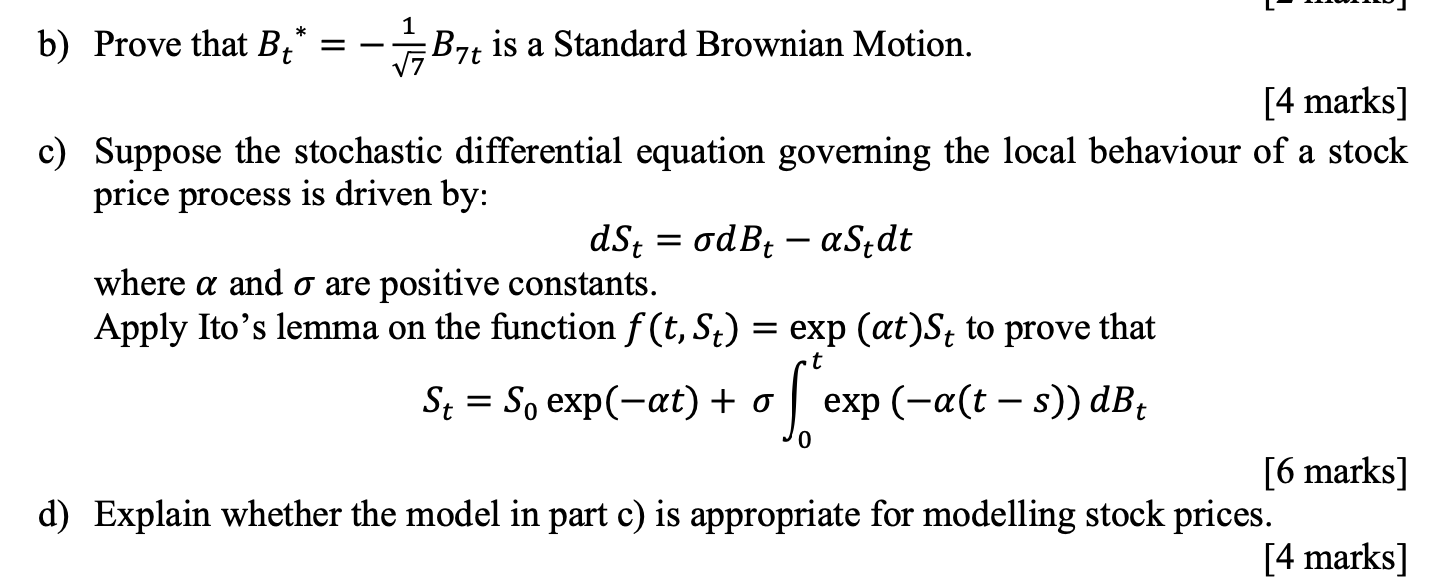

Question: please can you solve, there's no missing links or info, very urgent, thank you L_ ' 'W J b) Prove that 3; = % B7:

please can you solve, there's no missing links or info, very urgent, thank you

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock