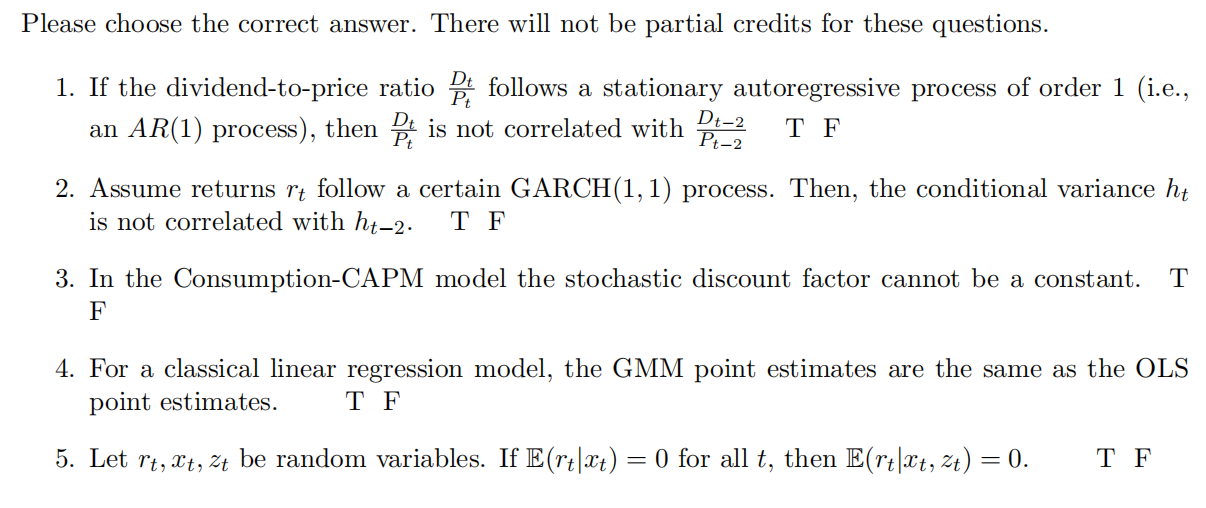

Question: Please choose the correct answer. There will not be partial credits for these questions. 1. If the dividend-toprice ratio %' follows a stationary autoregressive process

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock