Question: please complete question number 4. I will thumbs up correct answer. please include excel equation and references so I can know where the numbers came

please complete question number 4. I will thumbs up correct answer. please include excel equation and references so I can know where the numbers came from! thank you

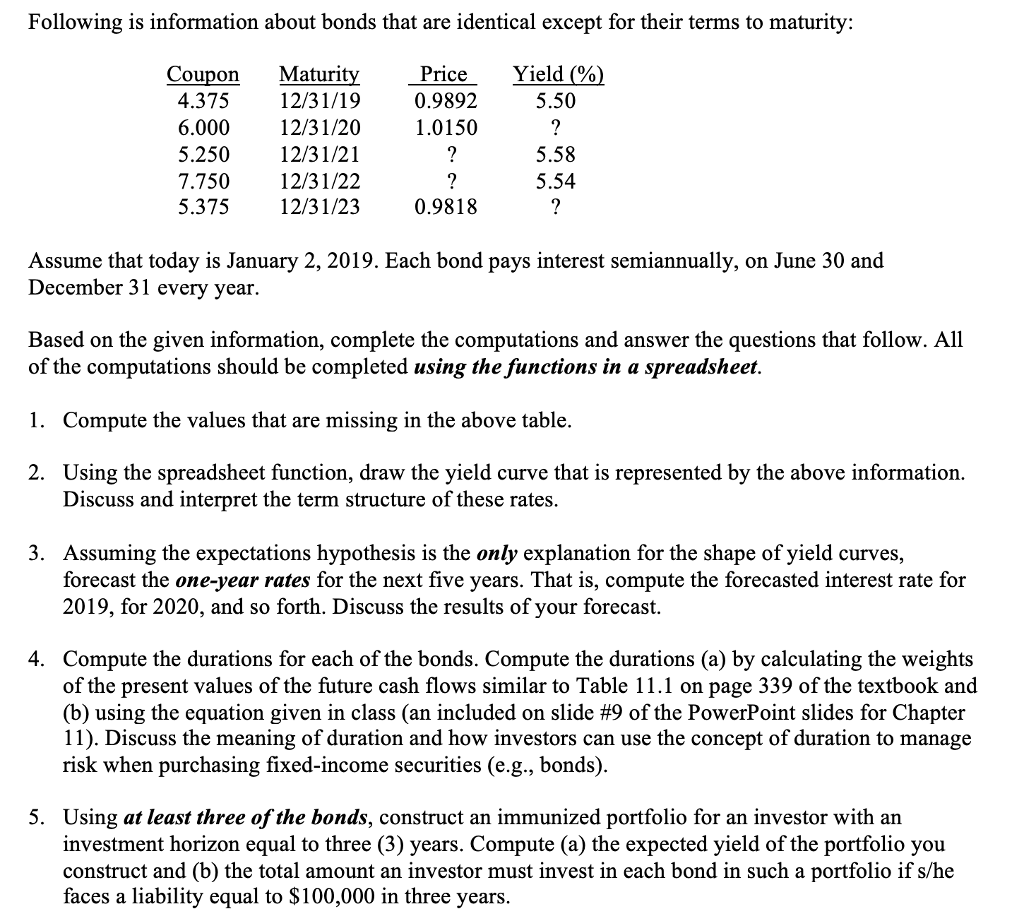

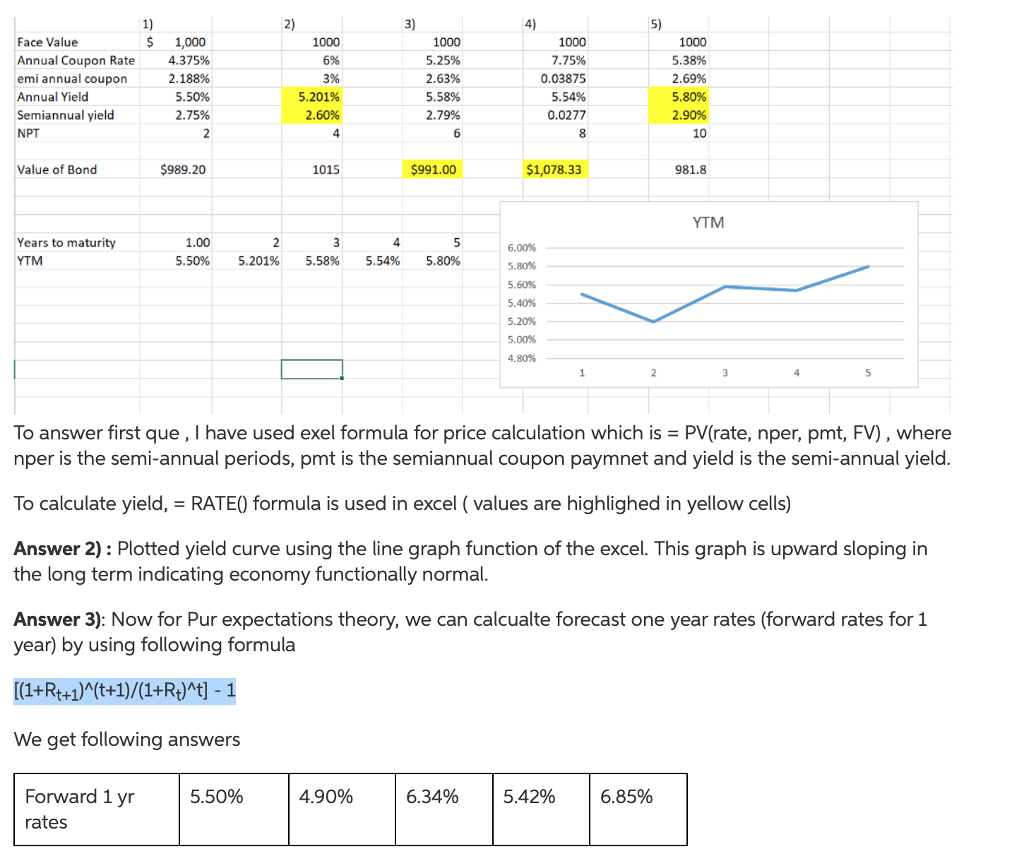

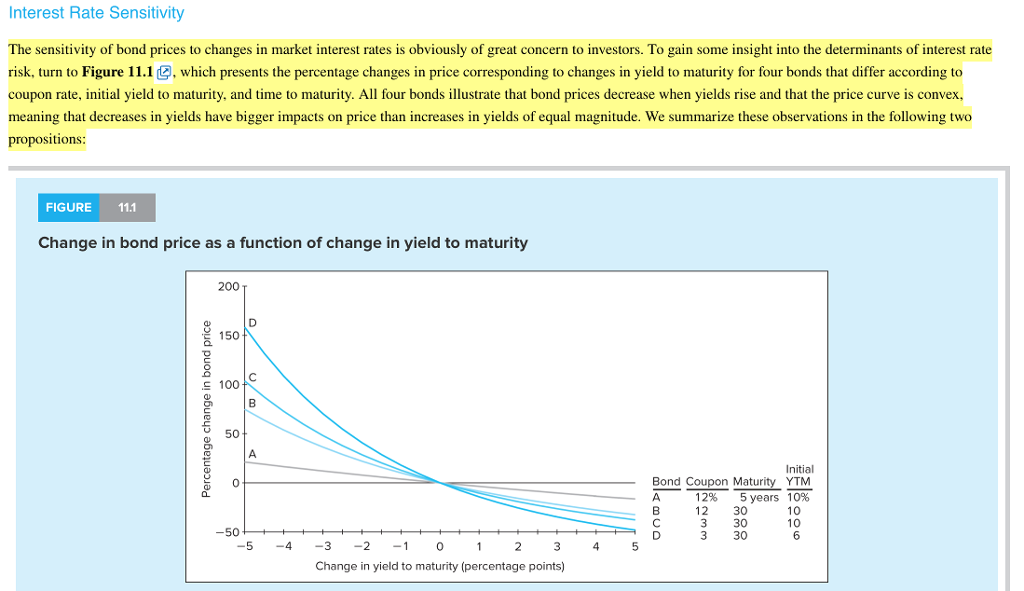

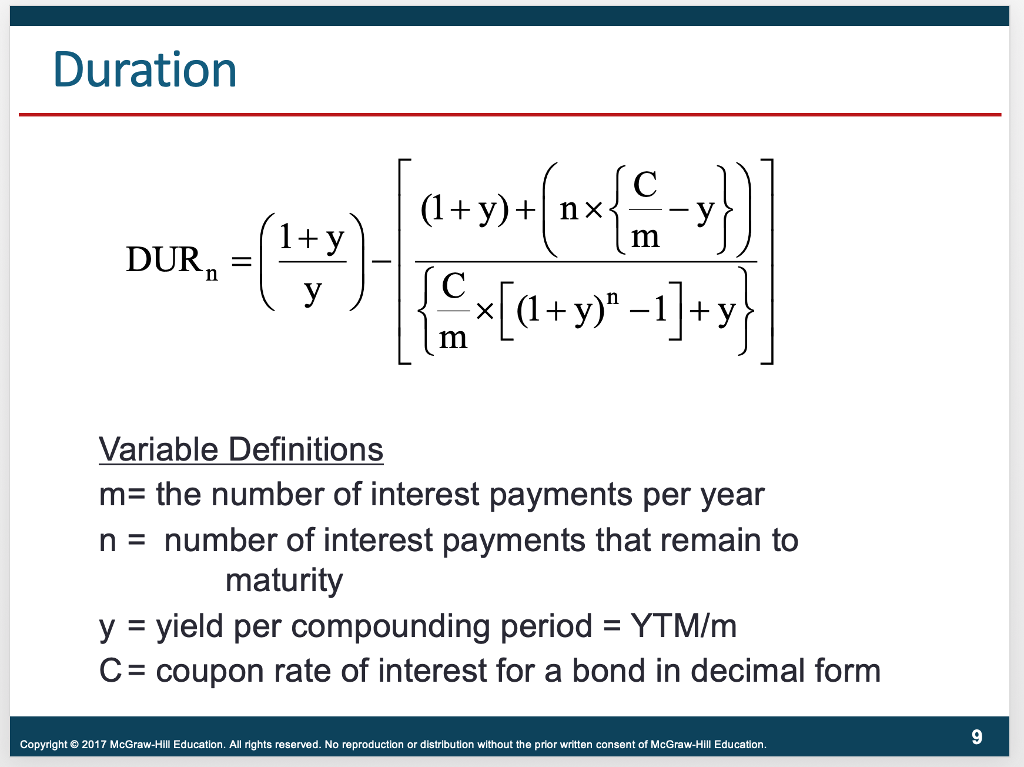

Following is information about bonds that are identical except for their terms to maturity: Price 0.9892 1.0150 Coupon Maturi 0 0 4.37512/31/19 6.00012/31/20 5.250 12/31/21 7.75012/31/22 5.375 12/31/23 5.50 5.58 5.54 0.9818 Assume that today is January 2, 2019. Each bond pays interest semiannually, on June 30 and December 31 every year. Based on the given information, complete the computations and answer the questions that follow. All of the computations should be completed using the functions in a spreadsheet. 1. Compute the values that are missing in the above table. 2. Using the spreadsheet function, draw the yield curve that is represented by the above information. Discuss and interpret the term structure of these rates. 3. Assuming the expectations hypothesis is the only explanation for the shape of yield curves, forecast the one-year rates for the next five years. That is, compute the forecasted interest rate for 2019, for 2020, and so forth. Discuss the results of your forecast. 4. Compute the durations for each of the bonds. Compute the durations (a) by calculating the weights of the present values of the future cash flows similar to Table 11.1 on page 339 of the textbook and (b) using the equation given in class (an included on slide #9 of the PowerPoint slides for Chapter 11). Discuss the meaning of duration and how investors can use the concept of duration to manage risk when purchasing fixed-income securities (e.g., bonds). Using at least three of the bonds, construct an immunized portfolio for an investor with an investment horizon equal to three (3) years. Compute (a) the expected yield of the portfolio you construct and (b) the total amount an investor must invest in each bond in such a portfolio if s/he faces a liability equal to $100,000 in three years 5. Following is information about bonds that are identical except for their terms to maturity: Price 0.9892 1.0150 Coupon Maturi 0 0 4.37512/31/19 6.00012/31/20 5.250 12/31/21 7.75012/31/22 5.375 12/31/23 5.50 5.58 5.54 0.9818 Assume that today is January 2, 2019. Each bond pays interest semiannually, on June 30 and December 31 every year. Based on the given information, complete the computations and answer the questions that follow. All of the computations should be completed using the functions in a spreadsheet. 1. Compute the values that are missing in the above table. 2. Using the spreadsheet function, draw the yield curve that is represented by the above information. Discuss and interpret the term structure of these rates. 3. Assuming the expectations hypothesis is the only explanation for the shape of yield curves, forecast the one-year rates for the next five years. That is, compute the forecasted interest rate for 2019, for 2020, and so forth. Discuss the results of your forecast. 4. Compute the durations for each of the bonds. Compute the durations (a) by calculating the weights of the present values of the future cash flows similar to Table 11.1 on page 339 of the textbook and (b) using the equation given in class (an included on slide #9 of the PowerPoint slides for Chapter 11). Discuss the meaning of duration and how investors can use the concept of duration to manage risk when purchasing fixed-income securities (e.g., bonds). Using at least three of the bonds, construct an immunized portfolio for an investor with an investment horizon equal to three (3) years. Compute (a) the expected yield of the portfolio you construct and (b) the total amount an investor must invest in each bond in such a portfolio if s/he faces a liability equal to $100,000 in three years 5

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts