Question: PLEASE COMPLETE THE PRELIMINARY ANALYTICAL PROCEDURES CHART FULLY. THAT'S ALL I NEED. THANK YOU! WILL THUMBS UP YOUR ANSWER. I NEED THIS BY WEDNESDAY OCT

PLEASE COMPLETE THE PRELIMINARY ANALYTICAL PROCEDURES CHART FULLY. THAT'S ALL I NEED. THANK YOU! WILL THUMBS UP YOUR ANSWER. I NEED THIS BY WEDNESDAY OCT 27TH AT 9PM.

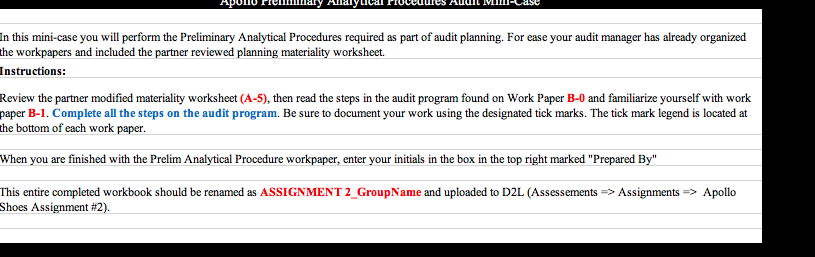

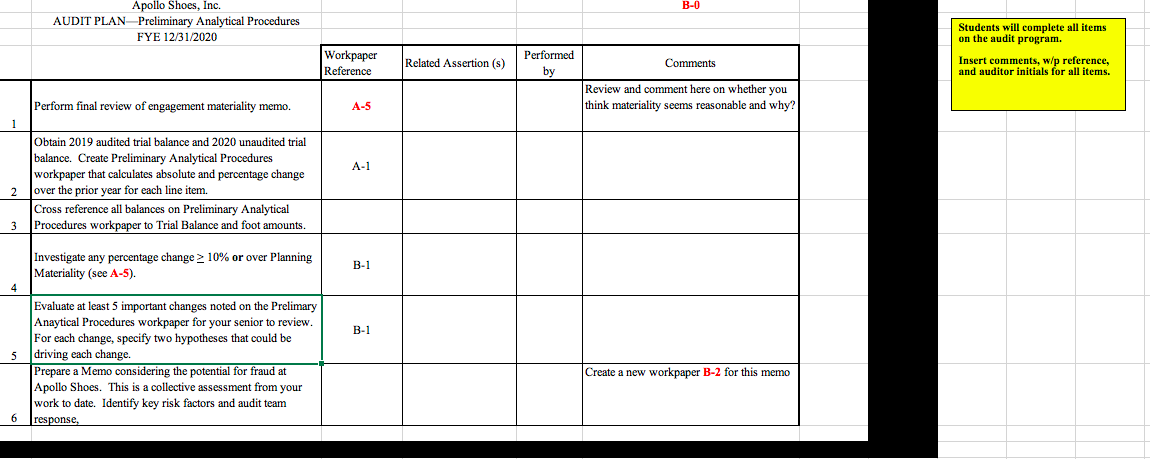

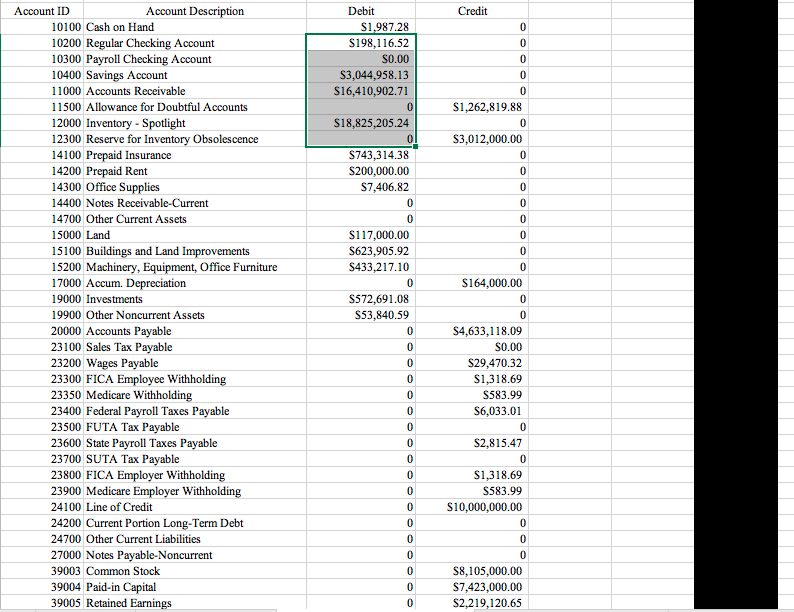

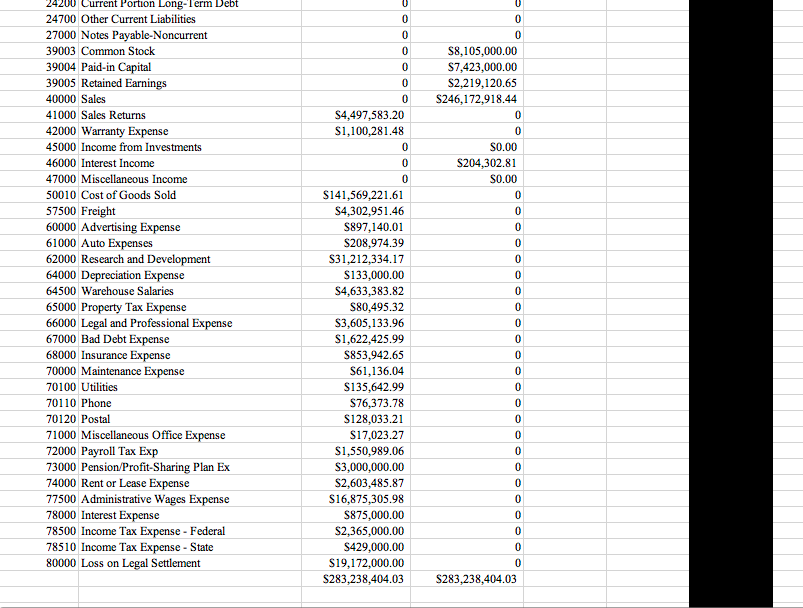

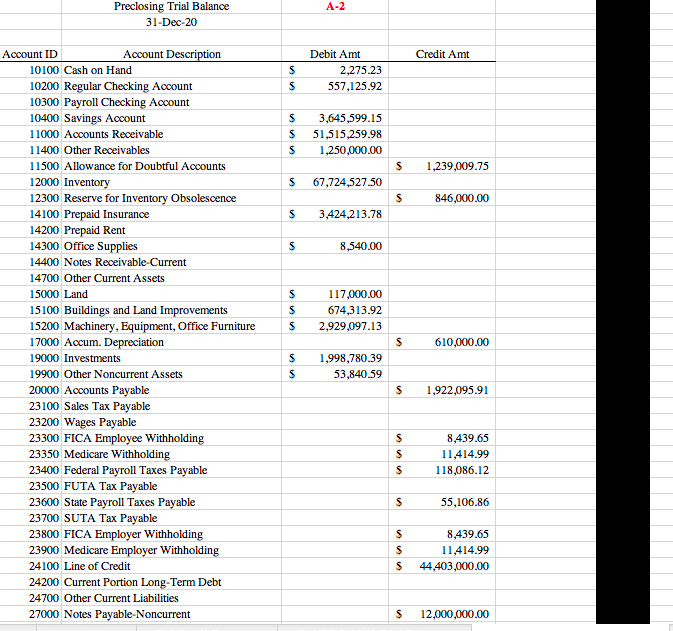

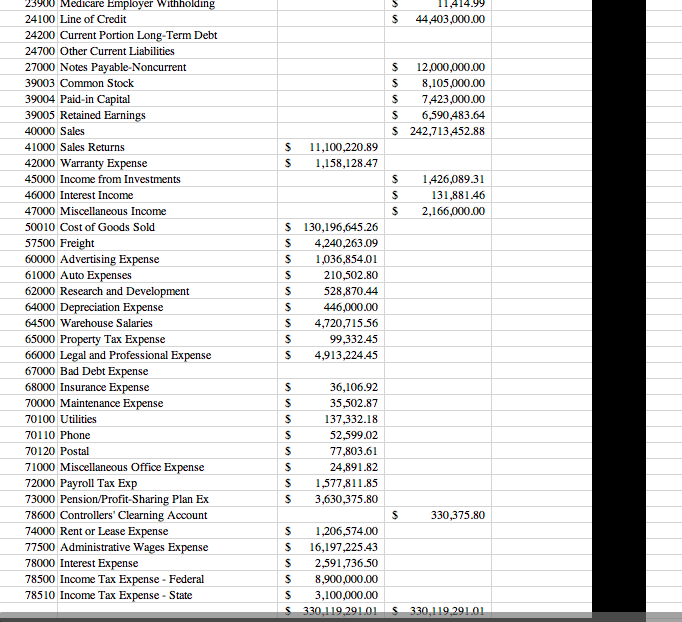

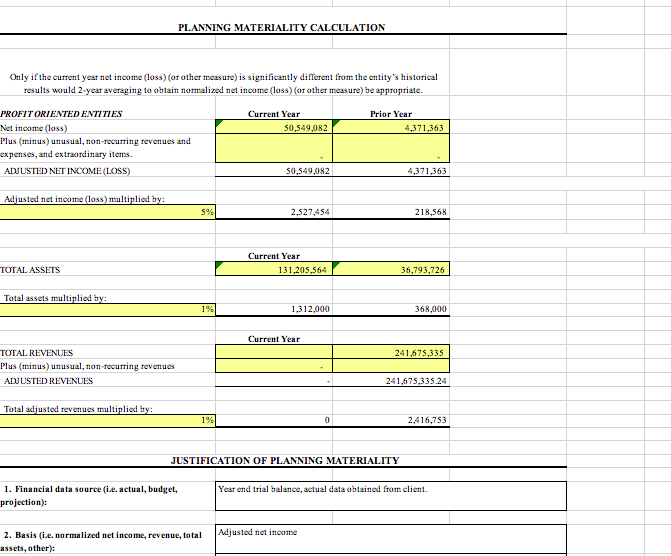

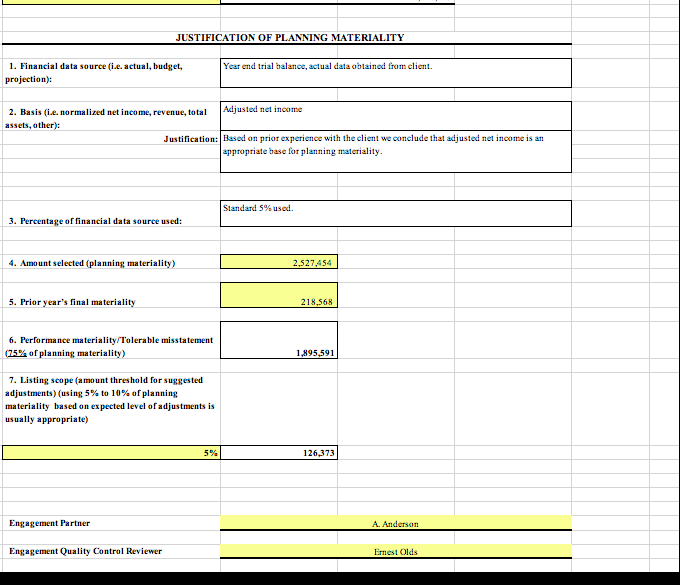

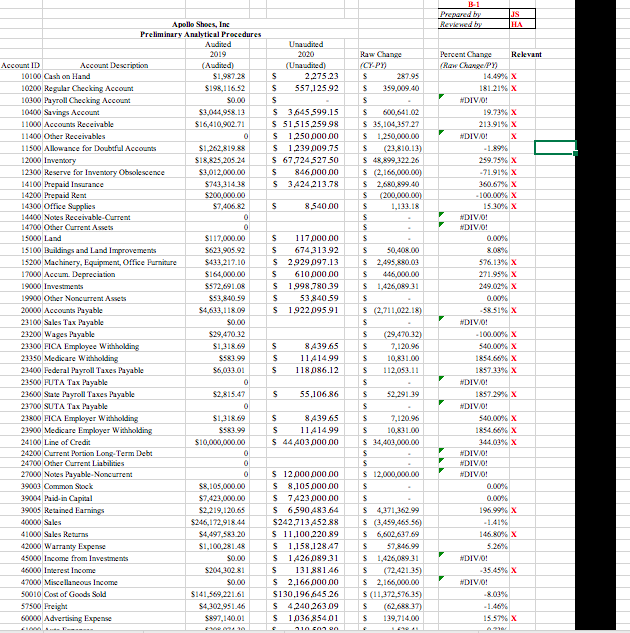

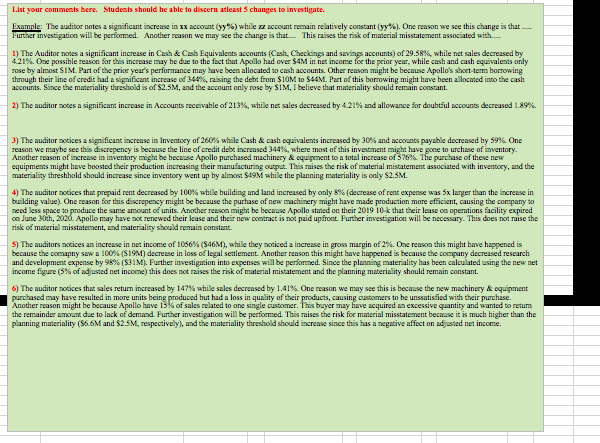

Allaly In this mini-case you will perform the Preliminary Analytical Procedures required as part of audit planning. For ease your audit manager has already organized he workpapers and included the partner reviewed planning materiality worksheet. Instructions: Review the partner modified materiality worksheet (A-5), then read the steps in the audit program found on Work Paper B-0 and familiarize yourself with work paper B-1. Complete all the steps on the audit program. Be sure to document your work using the designated tick marks. The tick mark legend is located at the bottom of each work paper. When you are finished with the Prelim Analytical Procedure workpaper, enter your initials in the box in the top right marked "Prepared By" This entire completed workbook should be renamed as ASSIGNMENT 2_GroupName and uploaded to D2L (Assessements => Assignments => Apollo Shoes Assignment #2).Apollo Shoes, Inc. B-0 AUDIT PLAN-Preliminary Analytical Procedures Students will complete all items FYE 12/31/2020 on the audit program Workpaper Performed Reference Related Assertion (s) by Comments Insert comments, w/p reference, and auditor initials for all items. Review and comment here on whether you Perform final review of engagement materiality memo. A-5 think materiality seems reasonable and why? Obtain 2019 audited trial balance and 2020 unaudited trial balance. Create Preliminary Analytical Procedures A-1 workpaper that calculates absolute and percentage change 2 over the prior year for each line item. Cross reference all balances on Preliminary Analytical 3 Procedures workpaper to Trial Balance and foot amounts. Investigate any percentage change 2 10% or over Planning B-1 Materiality (see A-5). 4 Evaluate at least 5 important changes noted on the Prelimary Anaytical Procedures workpaper for your senior to review. B-1 For each change, specify two hypotheses that could be driving each change. Prepare a Memo considering the potential for fraud at Create a new workpaper B-2 for this memo Apollo Shoes. This is a collective assessment from your work to date. Identify key risk factors and audit team response,Account ID Account Description Debit Credit 10100 Cash on Hand $1,987.28 10200 Regular Checking Account $198,116.52 10300 Payroll Checking Account 50.00 10400 Savings Account $3,044,958.13 11000 Accounts Receivable $16,410,902.71 1 1500 Allowance for Doubtful Accounts $1,262,819.88 12000 Inventory - Spotlight $18,825,205.24 0 12300 Reserve for Inventory Obsolescence $3,012,000.00 14100 Prepaid Insurance $743,314.38 14200 Prepaid Rent $200,000.00 14300 Office Supplies $7,406.82 14400 Notes Receivable-Current 14700 Other Current Assets 15000 Land $117,000.00 15100 Buildings and Land Improvements $623,905.92 15200 Machinery, Equipment, Office Furniture $433,217.10 17000 Accum. Depreciation $164,000.00 19000 Investments $572,691.08 19900 Other Noncurrent Assets $53,840.59 20000 Accounts Payable $4,633,118.09 23100 Sales Tax Payable 50.00 23200 Wages Payable $29,470.32 23300 FICA Employee Withholding $1,318.69 23350 Medicare Withholding $583.99 23400 Federal Payroll Taxes Payable $6,033.01 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable $2,815.47 23700 SUTA Tax Payable 23800 FICA Employer Withholding $1,318.69 23900 Medicare Employer Withholding $583.99 24100 Line of Credit $10,000,000.00 24200 Current Portion Long-Term Debt 0 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 0 39003 Common Stock $8,105,000.00 39004 Paid-in Capital $7,423,000.00 39005 Retained Earnings $2,219,120.6524200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock $8,105,000.00 39004 Paid-in Capital $7,423,000.00 39005 Retained Earnings $2,219,120.65 40000 Sales $246,172,918.44 41000 Sales Returns $4,497,583.20 42000 Warranty Expense $1,100,281.48 45000 Income from Investments $0.00 46000 Interest Income $204,302.81 47000 Miscellaneous Income 0 50.00 50010 Cost of Goods Sold $141,569,221.61 57500 Freight $4,302,951.46 60000 Advertising Expense $897,140.01 61000 Auto Expenses $208,974.39 62000 Research and Development $31,212,334.17 64000 Depreciation Expense $133,000.00 64500 Warehouse Salaries $4,633,383.82 65000 Property Tax Expense $80,495.32 66000 Legal and Professional Expense $3,605,133.96 67000 Bad Debt Expense $1,622,425.99 68000 Insurance Expense $853,942.65 70000 Maintenance Expense $61,136.04 70100 Utilities $135,642.99 70110 Phone $76,373.78 70120 Postal $128,033.21 71000 Miscellaneous Office Expense $17,023.27 72000 Payroll Tax Exp $1,550,989.06 73000 Pension/Profit-Sharing Plan Ex $3,000,000.00 74000 Rent or Lease Expense $2,603,485.87 77500 Administrative Wages Expense $16,875,305.98 78000 Interest Expense $875,000.00 78500 Income Tax Expense - Federal $2,365,000.00 78510 Income Tax Expense - State $429,000.00 80000 Loss on Legal Settlement $19,172,000.00 $283,238,404.03 $283,238,404.03Preclosing Trial Balance A-2 31-Dec-20 Account ID Account Description Debit Amt Credit Amt 10100 Cash on Hand 2,275.23 10200 Regular Checking Account 557,125.92 10300 Payroll Checking Account 10400 Savings Account 3,645,599.15 1 1000 Accounts Receivable 51,515,259.98 1 1400 Other Receivables 1,250,000.00 11500 Allowance for Doubtful Accounts 1,239,009.75 12000 Inventory $ 67,724,527.50 12300 Reserve for Inventory Obsolescence 846,000.00 14100 Prepaid Insurance 3,424,213.78 14200 Prepaid Rent 14300 Office Supplies 8,540.00 14400 Notes Receivable-Current 14700 Other Current Assets 15000 Land 117,000.00 15100 Buildings and Land Improvements 674,313.92 15200 Machinery, Equipment, Office Furniture 2,929,097.13 17000 Accum. Depreciation S 610,000.00 19000 Investments 1,998,780.39 19900 Other Noncurrent Assets 53,840.59 20000 Accounts Payable $ 1,922,095.91 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 8,439.65 23350 Medicare Withholding 11,414.99 23400 Federal Payroll Taxes Payable 1 18,086.12 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 55,106.86 23700 SUTA Tax Payable 23800 FICA Employer Withholding 8,439.65 23900 Medicare Employer Withholding 11,414.99 24100 Line of Credit 44,403,000.00 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent $ 12,000,000.0023900 Medicare Employer Withholding 24100 Line of Credit 44.403,000.00 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 12,000,000.00 39003 Common Stock 8,105,000.00 39004 Paid-in Capital 7,423,000.00 39005 Retained Earnings 6,590,483.64 40000 Sales $ 242,713,452.88 41000 Sales Returns 11,100,220.89 42000 Warranty Expense 1,158,128.47 45000 Income from Investments 1,426,089.31 46000 Interest Income 131,881.46 47000 Miscellaneous Income 2,166,000.00 50010 Cost of Goods Sold 130,196,645.26 57500 Freight 4,240,263.09 60000 Advertising Expense 1,036,854.01 61000 Auto Expenses 210,502.80 62000 Research and Development 528,870.44 64000 Depreciation Expense 446,000.00 64500 Warehouse Salaries 4,720,715.56 65000 Property Tax Expense 99,332.45 66000 Legal and Professional Expense 4,913,224.45 67000 Bad Debt Expense 68000 Insurance Expense 36,106.92 70000 Maintenance Expense 35,502.87 70100 Utilities 137,332.18 70110 Phone 52,599.02 70120 Postal 77,803.61 71000 Miscellaneous Office Expense 24,891.82 72000 Payroll Tax Exp 1,577,811.85 73000 Pension/Profit-Sharing Plan Ex 3,630,375.80 78600 Controllers' Clearning Account 330,375.80 74000 Rent or Lease Expense 1,206,574.00 77500 Administrative Wages Expense 16,197,225.43 78000 Interest Expense 2,591,736.50 78500 Income Tax Expense - Federal 8,900,000.00 78510 Income Tax Expense - State 3,100,000.00 330 119 29101 5 330 119 291.01PLANNING MATERIALITY CALCULATION Only if the current year net income (loss) (or other measure) is significantly different from the entity's historical results would 2-year averaging to obtain normalized net income (loss) (or other measure) be appropriate. PROFIT ORIENTED ENTITIES Current Year Prior Year Net income (loss) 50,5-49,082 4,371,363 Plus (minus) unusual, non-recurring revenues and expenses, and extraordinary items. ADJUSTED NET INCOME (LOSS) 50.549 082 4,371,363 Adjusted net income (loss) multiplied by: 59% 2,527,454 218,568 Current Year TOTAL ASSETS 131,205,564 86,793,726 Total assets multiplied by: 1,312,000 368,000 Current Year TOTAL REVENUES 241,675,335 Plus (minus) unusual, non-recurring revenues ADJUSTED REVENUES 241,675,335.24 Total adjusted revenues multiplied by: 1% 0 2,416,753 JUSTIFICATION OF PLANNING MATERIALITY 1. Financial data source (i.e. actual, budget, Year end trial balance, actual data obtained from client. projection): 2. Basis (i.c. normalized net income, revenue, total Adjusted net income assets, other):JUSTIFICATION OF PLANNING MATERIALITY 1. Financial data source (i.c. actual, budget, Year end trial balance, actual data obtained from client. projection): 2. Basis (i.c. normalized net income, revenue, total Adjusted net income assets, other): Justification: Based on prior experience with the client we conclude that adjusted net income is an appropriate base for planning materiality. Standard 5% used. 3. Percentage of financial data source used: 4. Amount selected (planning materiality) 2,527,454 5. Prior year's final materiality 218,568 6. Performance materiality/ Tolerable misstatement (75% of planning materiality) 1,895,591 7. Listing scope (amount threshold for suggested adjustments) (using 5% to 10% of planning materiality based on expected level of adjustments is usually appropriate) 5% 126,373 Engagement Partner A. Anderson Engagement Quality Control Reviewer Ernest OldsB-1 Prepared by JS Apollo Shoes, Inc Reviewed by THA Preliminary Analytical Procedures Audited Unaudited 2019 2020 Raw Change Percent Change Relevant Account ID Account Description (Audited) (Unaudited) 10100 Cash on Hand $1,987 28 2.275.23 287.95 14.49% X 10300 Regular Checking Account $198,116 52 557.125.92 359,009.40 181 21% X 10300 Payroll Checking Account 50.00 #DIVO! 10400 Savings Account $3,044,958.13 $ 3.645,599.15 600,641 02 1971%% X 1 1000 Accounts Receivable $16,410,902.71 $ 51 ,515,259.98 5 35,104,357.27 213.91% X 11400 Other Receivables $ 1250 000 00 S 1,250,000.00 #DIV/O! 11500 Allowance for Doubtful Accounts $1,262 819 88 $ 1,239.009.75 (21,810.13) -1 89% 12000 Inventory $18 825,205 24 $ 67,724 527 50 5 48,899 322.26 259.75% X 12100 Reserve for Inventory Obsolescence $3,012,000.00 846 000 00 5 (2,165,000.00) -71.91% X 14100 Prepaid Insurance $743,314 38 3424 213.78 2,680,899.40 160.67% X 14200 Prepaid Rent $200.000.00 (200,000.00) 100 00%% X 14300 Office Supplies $7,406.82 $ 540.00 1,133.18 15 10%% X 14400 Notes Receivable Current NDIVO 4700 Other Current Assets #DIVO! 15000 Land $1 17,000.00 1 17 000 00 15100 Buildings and Land Improvements $621 905.92 674313.92 10,408.00 15200 Machinery, Equipment, Office Furniture $413 217.10 2929 097.13 2,495,850103 576.13% X 17000 Accum. Depreciation $164,000.00 610 000 00 446,000.00 271.95% X 19000 Investments $572,691 08 1,998,780.39 1,426,069 31 249 02% X 19900 Other Noncurrent Assets $51,840 59 53 ,840.59 0.00%% 20000 Accounts Payable $4,613,1 18 09 S 1,922 095.91 5 (2711,03218) 23100 Sales Tax Payable 50100 #DIVO! 23200 Wages Payable $29,470 12 (29,470 12 100.00% X 21300 FICA Employee Withholding $1,318 69 8 439.65 7,120.96 21350 Medicare Withholding $581 99 11 414.99 10,831.00 1854 60% X 21400 Federal Payroll Taxes Payable $6,031 01 1 18 086.12 112,053.1 1 1857 13%% X 23500 FUTA Tax Payable #DIVO! 21600 State Payroll Taxes Payable 52,815.47 55,106.86 52,291.19 1857 29% X 23700 SUTA Tax Payable 0 #DIVO! 21800 FICA Employer Withholding $1,318.69 8 439.65 7,120.96 MOOOM X 23900 Medicare Employer Withholding $581 99 11414.99 10,831 00 1854.60% X 24100 Line of Credit $10,000,060.00 44 403 000 .D0 34,403,000.00 24200 Current Portion Long Term Deb: #DIVO! 24700 Other Current Liabilities 0 DIVO! 27000 Notes Payable-Noncurrent $ 12 000 000 00 12 000,000.00 #DIV/O! 39003 Common Stock 58,105,000.00 $ 8,105 000 00 19004 Paid in Capital $7,421,000.00 $ 7423 000.00 0.00% 19005 Retained Earnings 52,219,120.65 $ 6,590483.64 5 4,371,362.99 195 99%% X 40000 Sales $246,172,918 44 $242.713 452.88 5 (3,459,465 56) -1.41% 41000 Sales Returns $4,497 583 20 $ 11,100.220.89 6,602 617 69 146 80% X 42000 Warranty Expense $1,100,281.48 $ 1.158.128.47 57,846.99 5.20% 45000 Income from Investments 50100 $ 142608931 5 1,426,089 31 #DIV/O! 16000 Interest Income $204 300 81 131 881 46 (72 421 35) -35 45% X 47000 Miscellaneous Income $ 2,166,000.00 5 2,165,000.00 #DIVO! 50010 Cost of Goods Sold $141,569 221.61 $130.196.645.26 5 (11,372,576 35) $7500 Freight 54,302,951.46 $ 4240 263.09 -1.46% 60000 Advertising Expense $897,140.01 1 036,85401 139,714.00 15 57% X46000 Interest Income 3204 302 81 131,881 46 (72 421.39) -3549% X 47000 Miscellaneous Income 50.00 $ 2.166.000.00 5 2,165,000.00 #DIVO! 50010 Cost of Goods Sold $141,569,221 61 $130,196.645.26 5 (11,372 576 35) $7500 Freight $4,302 951.46 4.240 .263.09 (62 68 8 37) -1.40% 50000 Advertising Expense 5897,140.01 1 036.85401 139,71400 15 57% X 51000 Auto Expenses 5208 974 19 210,502.80 1,528.41 0.73% 52000 Research and Development $31,212 134 17 528 87044 $ (30,683 463.73) 98 31% X 54000 Depreciation Expense $133 000.00 446 000 00 313,000.00 215 14% X 64500 Warehouse Salaries $4,631,181 82 4,720.715.56 $7 131.74 1.85% 65000 Property Tax Expense 580 495 12 99 332 45 18,817.13 2140K X 65000 Legal and Professional Expense 53,605,133.96 4913 .224.45 $ 1 108 090.49 16 28% X 57000 Bad Debt Expense $1,622,425.99 (1,622,425.99) 100 00%% X 58000 Insurance Expense $851 942 65 S 36.106.92 (817,835 73) 95 7TH X 70000 Maintenance Expense $61,136.04 35,502.87 (25,61217 41 91% X To100 Utilities $135 642.99 137 332.18 1,689.19 1.2:9%% 701 10 Phone $76,371 78 52,599.02 (23,734.35) 31.13%% X 10120 Postal $128 013 21 77 803.61 (50,229.60) -19 21%% X 71000 Miscellaneous Office Expense $17,031 27 24.891.82 7,868 55 46 22% X 72000 Payroll Tax Exp $1,550,989 06 1 577 811.85 26,822.79 1.73% 73000 Pension Profit Sharing Plan Ex $3,000,000.00 3 630 375.80 630,375.80 21 01% X 78600 Controllers' Clearning Account 5 330 375.80 130,375.80 #DIVO! 74000 Rent or Lease Expense 62,603 485 87 1 206 574.00 5 (1,395,91187) 51 60% X 73500 Administrative Wages Expense $16,875,305.98 $ 16,197 225.43 $ (678 060 55) 4102% 78000 Interest Expense 5875,000.00 $ 2591,73650 $ 1,716,736 50 196 20%% X 78500 Income Tax Expense . Federal $2,365,000100 $ 8900 000.00 $ 6,535,000.00 276 12%% X 78510 Income Tax Expense . State $429 000.00 $ 3.100 000.00 $ 2671,000.00 522 61%% X 30000 Loss on Legal Settlement $19,172 000.00 ($19,172 060.00) 100 00%% X F F PY TE Tickmark Legend (students can'should add to this list, as untamed) - Footed without exception TB . Agrees to Trial Balance without exception PY - Agrees to prior year wadited trial balance without exception Instructions: Complete the Analytical Review (above). Evaluate your findings and comment on the relationships within the trial balance identified and make decisions about possible audit approaches or significance. Students should be able to discern at least 'S changes to investigate and hypothesize at least two reasons we see the change we do, as well as if you think Materiality should increase, decrease or remain neutral. Use your GAAP knowledge and your business acumen to appropriately address what may or may not be expected. You are free to use any information available to you either via the memos or the competitor financial statements. Don't know where to begin? Mar. It is useful to re-read the BOD minutes, 10-K and first figure out what the company does.List your comments here. Students should be able to discern atleast $ changes to investigate. Example: The auditor notes a significant increase in xx account (yy56) while oz account remain relatively constant (yy76). One reason we see this change is that .. Further investigation will be performed. Another reason we may see the change is that.. This raises the risk of material misstatement associated with... !) The Auditor notes a significant increase in Cash & Cash Equivalents accounts (Cash, Checkings and savings accounts) of 29.58%, while net sales decreased by 4.21%%. One possible reason for this increase may be due to the fact that Apollo had over $4M in net income for the prior year, while cash and cash equivalents only rose by almost $ IM. Part of the prior year's performance may have been allocated to cash accounts. Other reason might be because Apollo's short-team borrowing through their line of credit had a significant increase of 340%%, raising the debt from $10M to $44M. Part of this borrowing might have been allocated into the cash accounts. Since the materiality threshold is of $.5M, and the account only rose by $1M, I believe that materiality should remain constant. 2) The auditor notes a significant increase in Accounts receivable of 213%%, while net sales decreased by 4 21%% and allowance for doubtful accounts decreased 1.89%% 3) The auditor notices a significant increase in Inventory of 260%% while Cash & cash equivalents increased by 30%% and accounts payable decreased by 59%% One reason we maybe see this discrepancy is because the line of credit debt increased 34416, where most of this investment might have gone to urchase of inventory. Another reason of increase in inventory might be because Apollo purchased machinery & equipment to a total increase of 570 6. The purchase of these new equipments might have boosted their production increasing their manufacturing output. This raises the risk of material mistatement associated with inventory, and the materiality threshhold should increase since inventory went up by almost $49M while the planning materiality is only $2.3M. 4) The auditor notices that prepaid rent decreased by 100% while building and land increased by only $%% (decrease of rent expense was 5x larger than the increase in building value). One reason for this discrepancy might be because the purhase of new machinery might have made production more efficient, causing the company to need less space to produce the same amount of units. Another reason might be because Apollo stated on their 2019 10-k that their lease on operations facility expired on June 30th, 2020. Apollo may have not renewed their lease and their new contract is not paid upfront. Further investigation will be necessary. This does not raise the risk of material misstatement, and materiality should remain constant. 3/ The auditors notices an increase in net income of 1086% (346M1), while they noticed a increase in gross margin of 2%%. One reason this might have happened is because the comapny saw a 100%% ( 1961) decrease in loss of legal settlement. Another reason this might have happened is because the company decreased research and development expense by 98%% ($31M). Further investigation into expenses will be performed. Since the planning materiality has been calculated using the nee net income figure (bla of adjusted net income) this does not raises the risk of material mistatement and the planning materiality should remain constant. " The auditor notices that sales return increased by 147%% while sales decreased by 1.41%% One reason we may see this is because the new machinery & equipment purchased may have resulted in more units being produced but had a loss in quality of their products, causing customers to be unssatisfied with their purchase. Another reason might be because Apollo have 15is of sales related to one single customer. This bayer may have acquired an excessive quantity and wanted to return the remainder amount due to lack of demand. Further investigation will be performed. This mises the risk for material misstatement because it is much higher than the planning materiality ($5.GM and $2.5M, respectively), and the materiality threshold should increase since this has a negative affect on adjusted net income

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!