Question: please complete the question long hand! please! Expected Cash In flows of Annual Period in Which Cash Receipts Principal and Interest Are Expected Payments $1,275,600

please complete the question long hand! please!

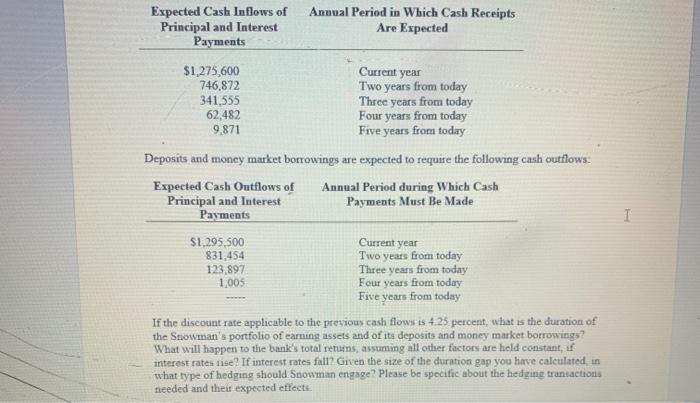

please complete the question long hand! please! Expected Cash In flows of Annual Period in Which Cash Receipts Principal and Interest Are Expected Payments $1,275,600 Current year 746,872 Two years from today 341,555 Three years from today 62,482 Four years from today 9,871 Five years from today Deposits and money market borrowings are expected to require the following cash outflows. Expected Cash Outflows of Annual Period during Which Cash Principal and Interest Payments Must Be Made Payments $1,295,500 Current year 831.454 Two years from today 123,897 Three years from today 1,005 Four years from today Five years from today If the discount rate applicable to the previous cash flows is 4.25 percent, what is the duration of the Snowman's portfolio of earning assets and of its deposits and money market borrowings? What will happen to the bank's total retums, assuming all other factors are held constant, if interest rates rise? If interest rates fall? Given the size of the duration gap you have calculated, in what type of hedging should Snowman engage? Please be specific about the hedging transactions needed and their expected effects. I Expected Cash In flows of Annual Period in Which Cash Receipts Principal and Interest Are Expected Payments $1,275,600 Current year 746,872 Two years from today 341,555 Three years from today 62,482 Four years from today 9,871 Five years from today Deposits and money market borrowings are expected to require the following cash outflows. Expected Cash Outflows of Annual Period during Which Cash Principal and Interest Payments Must Be Made Payments $1,295,500 Current year 831.454 Two years from today 123,897 Three years from today 1,005 Four years from today Five years from today If the discount rate applicable to the previous cash flows is 4.25 percent, what is the duration of the Snowman's portfolio of earning assets and of its deposits and money market borrowings? What will happen to the bank's total retums, assuming all other factors are held constant, if interest rates rise? If interest rates fall? Given the size of the duration gap you have calculated, in what type of hedging should Snowman engage? Please be specific about the hedging transactions needed and their expected effects

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts