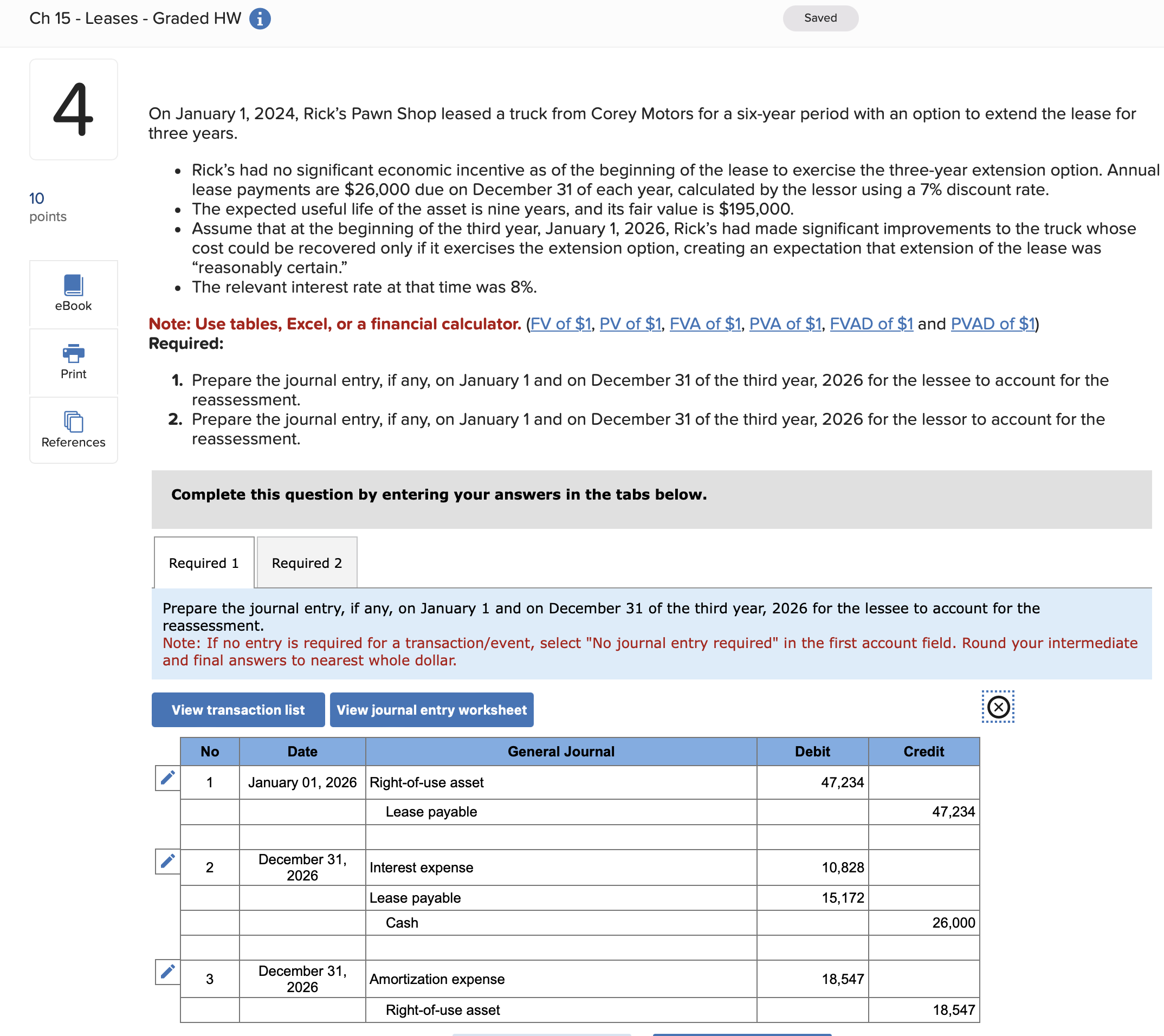

Question: please correct the ones wrong and solve the other ones missing Ch 15 - Leases - Graded HW i Saved 4 On January 1, 2024,

please correct the ones wrong and solve the other ones missing

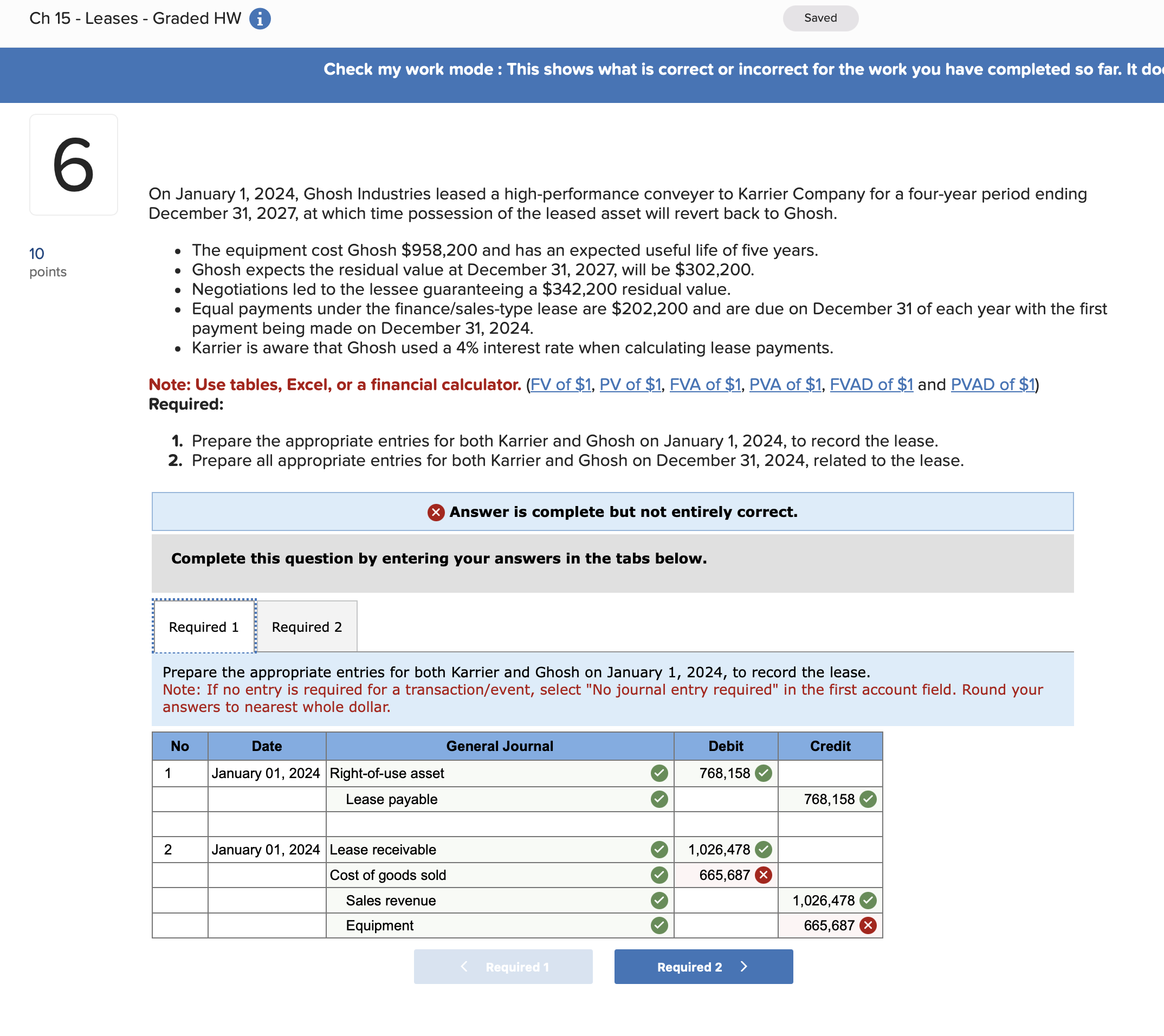

Ch 15 - Leases - Graded HW i Saved 4 On January 1, 2024, Rick's Pawn Shop leased a truck from Corey Motors for a six-year period with an option to extend the lease for three years. . Rick's had no significant economic incentive as of the beginning of the lease to exercise the three-year extension option. Annual 10 lease payments are $26,000 due on December 31 of each year, calculated by the lessor using a 7% discount rate. points . The expected useful life of the asset is nine years, and its fair value is $195,000. . Assume that at the beginning of the third year, January 1, 2026, Rick's had made significant improvements to the truck whose cost could be recovered only if it exercises the extension option, creating an expectation that extension of the lease was "reasonably certain." . The relevant interest rate at that time was 8%. eBook Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, EVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) Required: Print 1. Prepare the journal entry, if any, on January 1 and on December 31 of the third year, 2026 for the lessee to account for the reassessment. n 2. Prepare the journal entry, if any, on January 1 and on December 31 of the third year, 2026 for the lessor to account for the References reassessment. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Prepare the journal entry, if any, on January 1 and on December 31 of the third year, 2026 for the lessee to account for the reassessment. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Round your intermediate and final answers to nearest whole dollar. View transaction list View journal entry worksheet No Date General Journal Debit Credit 1 January 01, 2026 Right-of-use asset 47,234 ease payable 17,234 2 December 31, 2026 Interest expense 10,828 Lease payable 15, 172 Cash 26,000 3 December 31, Amortization expense 18,547 2026 Right-of-use asset 18,547Ch 15 - Leases - Graded HW i Saved Check my work mode : This shows what is correct or incorrect for the work you have completed so far. It do 6 On January 1, 2024, Ghosh Industries leased a high-performance conveyer to Karrier Company for a four-year period ending December 31, 2027, at which time possession of the leased asset will revert back to Ghosh. 10 . The equipment cost Ghosh $958,200 and has an expected useful life of five years. points . Ghosh expects the residual value at December 31, 2027, will be $302,200. . Negotiations led to the lessee guaranteeing a $342,200 residual value. Equal payments under the finance/sales-type lease are $202,200 and are due on December 31 of each year with the first payment being made on December 31, 2024. Karrier is aware that Ghosh used a 4% interest rate when calculating lease payments. Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) Required: 1. Prepare the appropriate entries for both Karrier and Ghosh on January 1, 2024, to record the lease. 2. Prepare all appropriate entries for both Karrier and Ghosh on December 31, 2024, related to the lease. x Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Prepare the appropriate entries for both Karrier and Ghosh on January 1, 2024, to record the lease. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Round your answers to nearest whole dollar. No Date General Journal Debit Credit January 01, 2024 Right-of-use asset 768, 158 Lease payable 768, 158 2 January 01, 2024 Lease receivable 1,026,478 Cost of goods sold 665,687 X Sales revenue 1,026,478 Equipment 665,687 X

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts