Question: please correct treynor values and explain Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period

please correct treynor values and explain

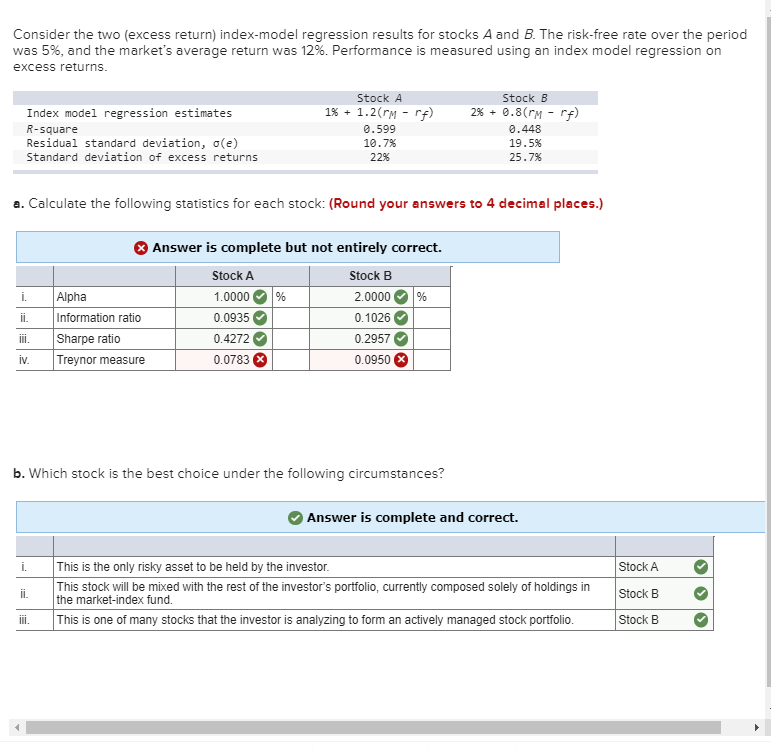

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 5%, and the market's average return was 12%. Performance is measured using an index model regression on excess returns. Index model regression estimates R-square Residual standard deviation, o(e) Standard deviation of excess returns Stock A 1% + 1.2 (rm -rf 0.599 10.7% 22% Stock B 2% + 0.8( rm -rf) 0.448 19.5% 25.7% a. Calculate the following statistics for each stock: (Round your answers to 4 decimal places.) Alpha Answer is complete but not entirely correct. Stock A Stock B 1.0000 % 2.0000 % 0.0935 0.1026 0.4272 0.2957 0.0783 X 0.0950 X Information ratio Sharpe ratio Treynor measure iv. b. Which stock is the best choice under the following circumstances? Answer is complete and correct. Stock A This is the only risky asset to be held by the investor. This stock will be mixed with the rest of the investor's portfolio, currently composed solely of holdings in the market-index fund. Stock B Stock B This is one of many stocks that the investor is analyzing to form an actively managed stock portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts