Question: please do 2.2 question = 2.1 We invest according to a vector of weights w=(W1, W2, W3) = (0, 2, 1) where the weight w

please do 2.2 question

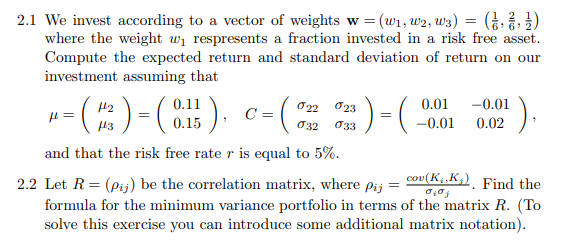

= 2.1 We invest according to a vector of weights w=(W1, W2, W3) = (0, 2, 1) where the weight w respresents a fraction invested in a risk free asset. Compute the expected return and standard deviation of return on our investment assuming that H2 0.11 022 0.01 -0.01 C 43 0.15 -0.01 0.02 and that the risk free rate r is equal to 5%. 2.2 Let R=(Pi) be the correlation matrix, where Pij = con (KK). Find the formula for the minimum variance portfolio in terms of the matrix R. (To solve this exercise you can introduce some additional matrix notation). -=( )=(). ----( hele ) c :); 032 033 = 2.1 We invest according to a vector of weights w=(W1, W2, W3) = (0, 2, 1) where the weight w respresents a fraction invested in a risk free asset. Compute the expected return and standard deviation of return on our investment assuming that H2 0.11 022 0.01 -0.01 C 43 0.15 -0.01 0.02 and that the risk free rate r is equal to 5%. 2.2 Let R=(Pi) be the correlation matrix, where Pij = con (KK). Find the formula for the minimum variance portfolio in terms of the matrix R. (To solve this exercise you can introduce some additional matrix notation). -=( )=(). ----( hele ) c :); 032 033

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts