Question: please do it by hand, its due in two hours Price Data Period Stock 1 Stock 2 Stock 3 1 10 5 1 2 5

please do it by hand, its due in two hours

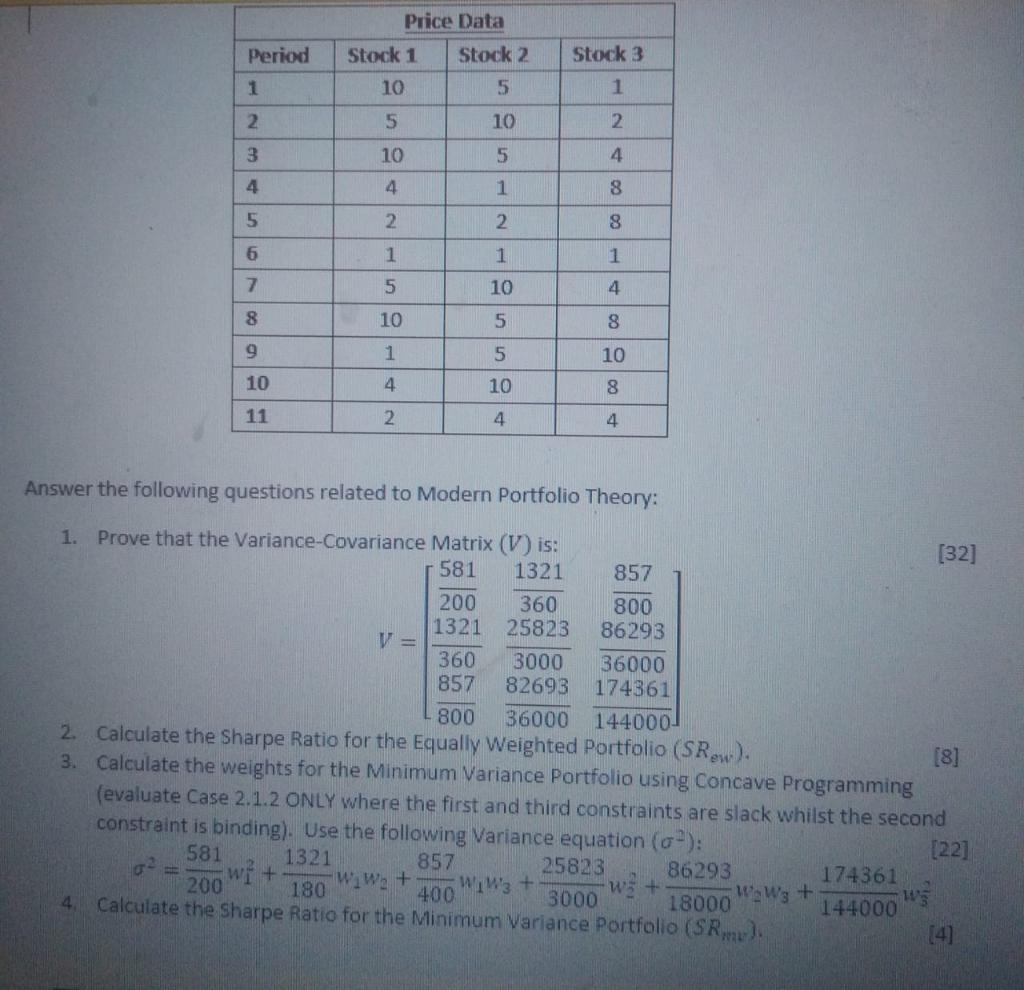

Price Data Period Stock 1 Stock 2 Stock 3 1 10 5 1 2 5 10 2 3 10 5 4 4 4 1 8 5 2 2 6 1 1 Aco 7 5 10 8 5 8 9 -|-|-| 5 10 10 10 8 11 2 4. 4 Answer the following questions related to Modern Portfolio Theory: 360 1. Prove that the Variance-Covariance Matrix (V) is: [32] 581 1321 857 200 360 800 1321 25823 86293 V = 3000 36000 857 82693 174361 800 36000 144000 2. Calculate the Sharpe Ratio for the Equally Weighted Portfolio (SR). [8] 3. Calculate the weights for the Minimum Variance Portfolio using Concave Programming (evaluate Case 2.1.2 ONLY where the first and third constraints are slack whilst the second constraint is binding). Use the following Variance equation (6"): [22] 581 1321 857 25823 86293 wf+ 174361 200 WiW. + WW'z + 180 w + 400 3000 18000 WWg + 4. Calculate the sharpe Ratio for the Minimum Variance Portfolio (SR). 144000 (4) ws Price Data Period Stock 1 Stock 2 Stock 3 1 10 5 1 2 5 10 2 3 10 5 4 4 4 1 8 5 2 2 6 1 1 Aco 7 5 10 8 5 8 9 -|-|-| 5 10 10 10 8 11 2 4. 4 Answer the following questions related to Modern Portfolio Theory: 360 1. Prove that the Variance-Covariance Matrix (V) is: [32] 581 1321 857 200 360 800 1321 25823 86293 V = 3000 36000 857 82693 174361 800 36000 144000 2. Calculate the Sharpe Ratio for the Equally Weighted Portfolio (SR). [8] 3. Calculate the weights for the Minimum Variance Portfolio using Concave Programming (evaluate Case 2.1.2 ONLY where the first and third constraints are slack whilst the second constraint is binding). Use the following Variance equation (6"): [22] 581 1321 857 25823 86293 wf+ 174361 200 WiW. + WW'z + 180 w + 400 3000 18000 WWg + 4. Calculate the sharpe Ratio for the Minimum Variance Portfolio (SR). 144000 (4) ws

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts