Question: Please do not round intermediate calculations, thank you! 4. Problem 18.04 (Black-Scholes Model) eBook Assume that you have been given the following information on Purcell

Please do not round intermediate calculations, thank you!

Please do not round intermediate calculations, thank you!

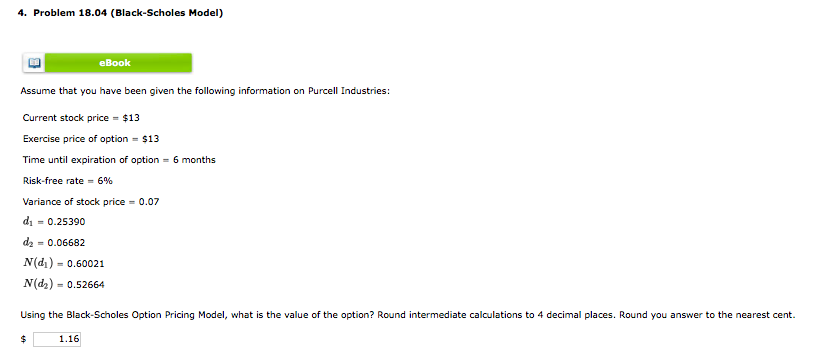

4. Problem 18.04 (Black-Scholes Model) eBook Assume that you have been given the following information on Purcell Industries: Current stock price = $13 Exercise price of option = $13 Time until expiration of option = 6 months Risk-free rate - 6% Variance of stock price = 0.07 di = 0.25390 d2 = 0.06682 N(di) = 0.50021 Nd) - 0.52664 Using the Black-Scholes Option Pricing Model, what is the value of the option? Round intermediate calculations to 4 decimal places. Round you answer to the nearest cent. $ 1.16

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock