Question: Please do not show or use excel, thank you. Problem 10. [4 pts] Mr. Slow is the chief investment officer of the S&B Endowment based

Please do not show or use excel, thank you.

Please do not show or use excel, thank you.

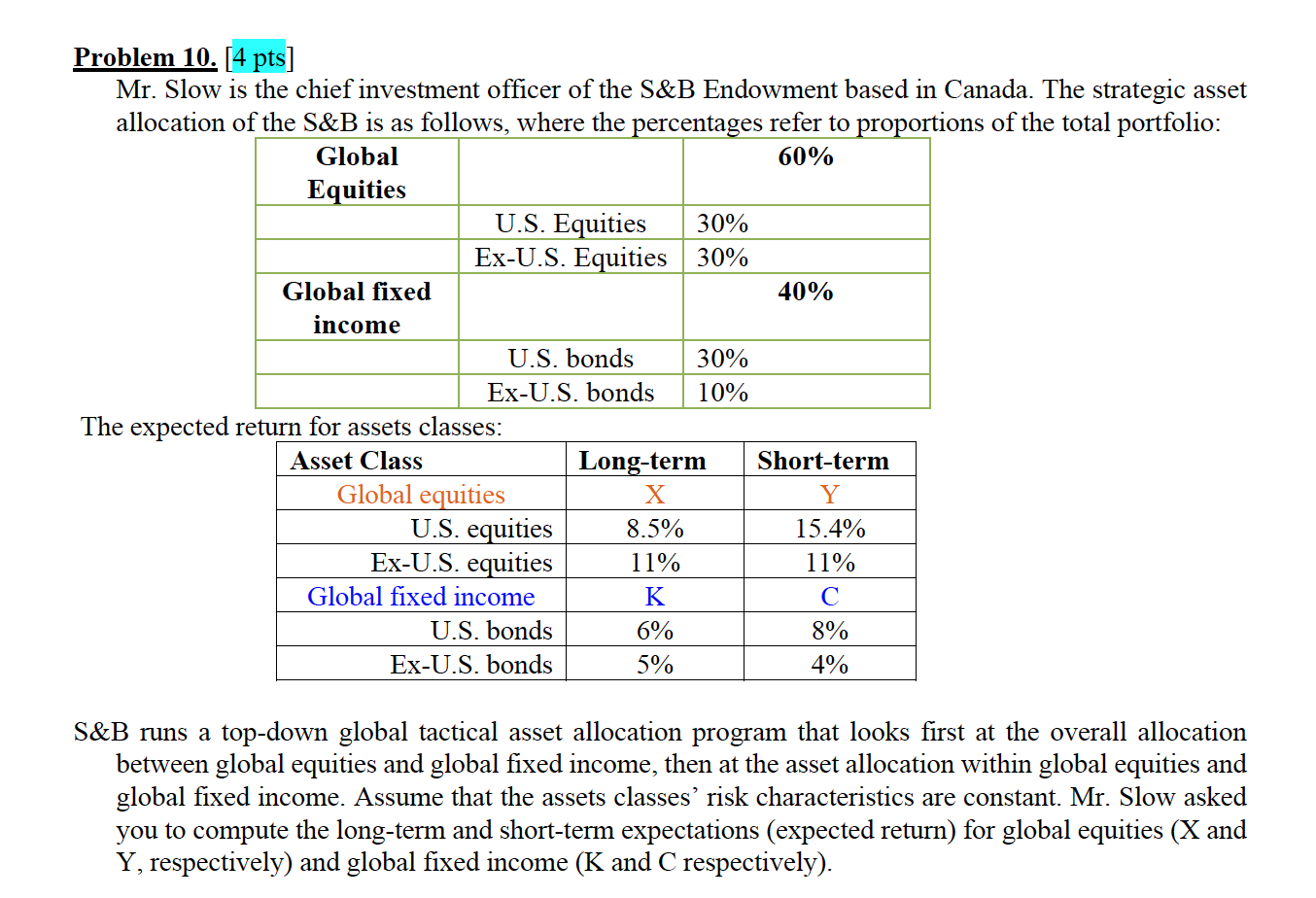

Problem 10. [4 pts] Mr. Slow is the chief investment officer of the S&B Endowment based in Canada. The strategic asset allocation of the S&B is as follows, where the percentages refer to proportions of the total portfolio: Global 60% Equities U.S. Equities 30% Ex-U.S. Equities 30% Global fixed 40% income U.S. bonds 30% Ex-U.S. bonds 10% The expected return for assets classes: Asset Class Long-term Short-term Global equities X Y U.S. equities 8.5% 15.4% Ex-U.S. equities 11% 11% Global fixed income K U.S. bonds 6% 8% Ex-U.S. bonds 5% 4% S&B runs a top-down global tactical asset allocation program that looks first at the overall allocation between global equities and global fixed income, then at the asset allocation within global equities and global fixed income. Assume that the assets classes' risk characteristics are constant. Mr. Slow asked you to compute the long-term and short-term expectations (expected return) for global equities (X and Y, respectively) and global fixed income (K and C respectively)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts