Question: Please do question 5 based on information from question 4. Thank you 4. A stock price is currently $30. Every 6 months the price will

Please do question 5 based on information from question 4. Thank you

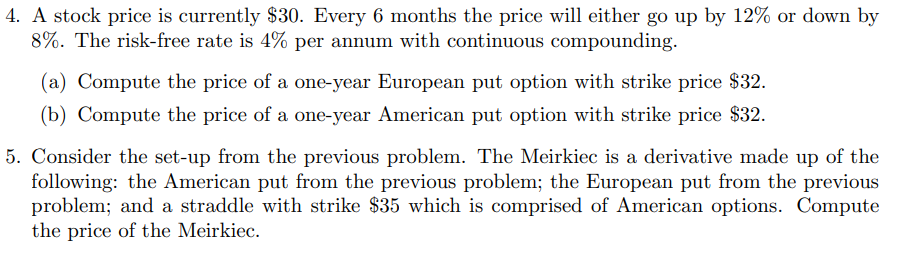

4. A stock price is currently $30. Every 6 months the price will either go up by 12% or down by 8%. The risk-free rate is 4% per annum with continuous compounding. (a) Compute the price of a one-year European put option with strike price $32. (b) Compute the price of a one-year American put option with strike price $32. 5. Consider the set-up from the previous problem. The Meirkiec is a derivative made up of the following: the American put from the previous problem; the European put from the previous problem; and a straddle with strike $35 which is comprised of American options. Compute the price of the Meirkiec. 4. A stock price is currently $30. Every 6 months the price will either go up by 12% or down by 8%. The risk-free rate is 4% per annum with continuous compounding. (a) Compute the price of a one-year European put option with strike price $32. (b) Compute the price of a one-year American put option with strike price $32. 5. Consider the set-up from the previous problem. The Meirkiec is a derivative made up of the following: the American put from the previous problem; the European put from the previous problem; and a straddle with strike $35 which is comprised of American options. Compute the price of the Meirkiec

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts