Question: Please do solve in detail ASAP. Do not copy paste. I will downvote if not answered properly. Thanks in advance. and include the last point

Please do solve in detail ASAP. Do not copy paste. I will downvote if not answered properly. Thanks in advance. and include the last point in your calculations

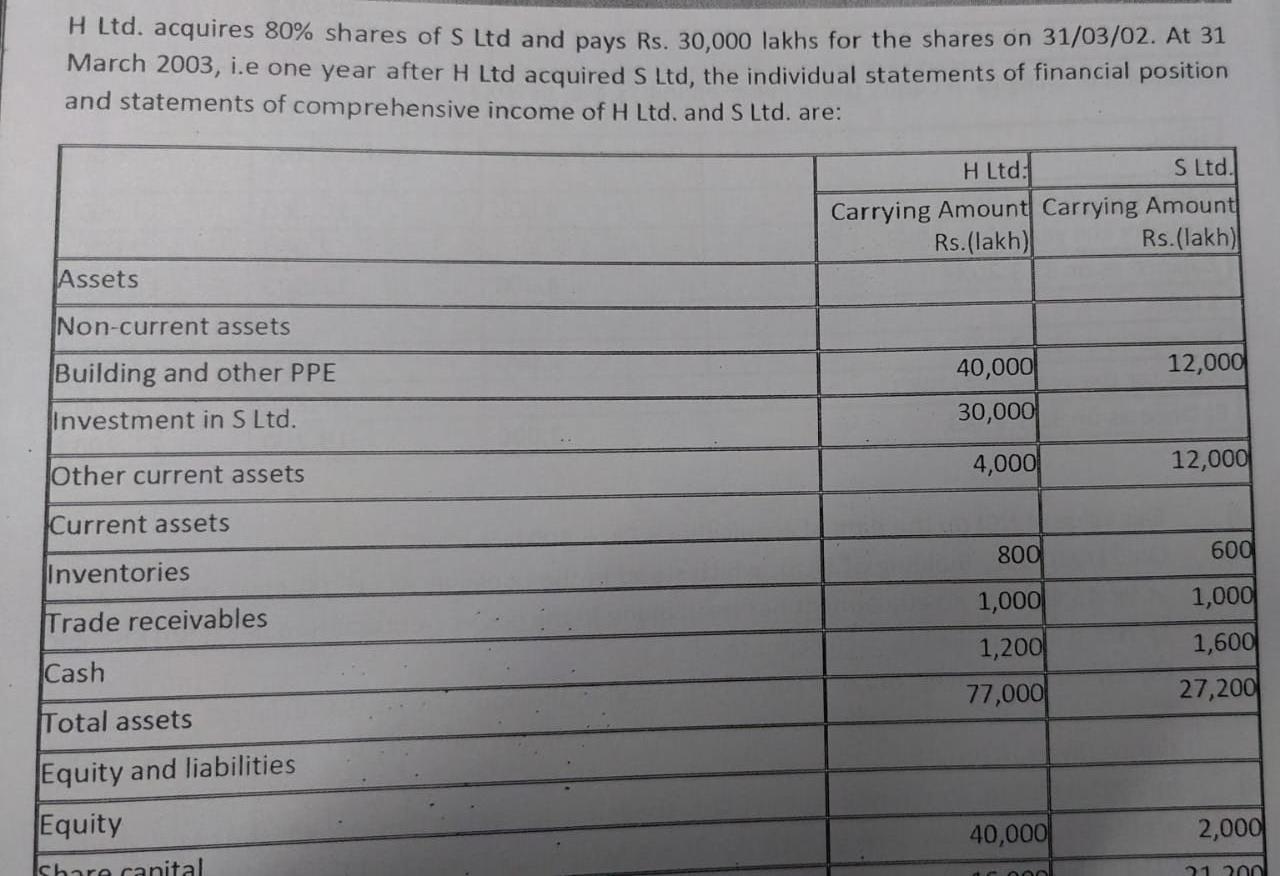

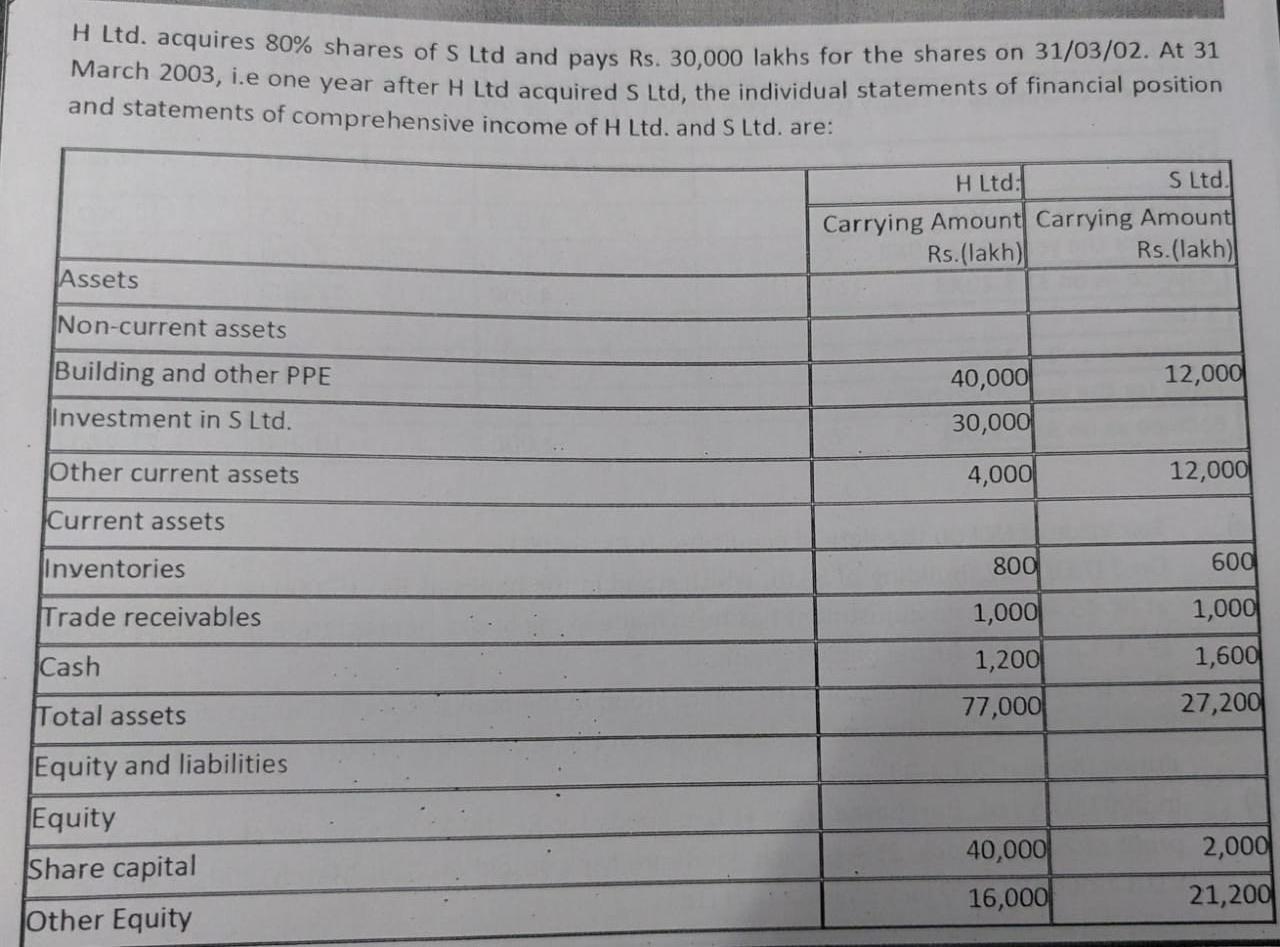

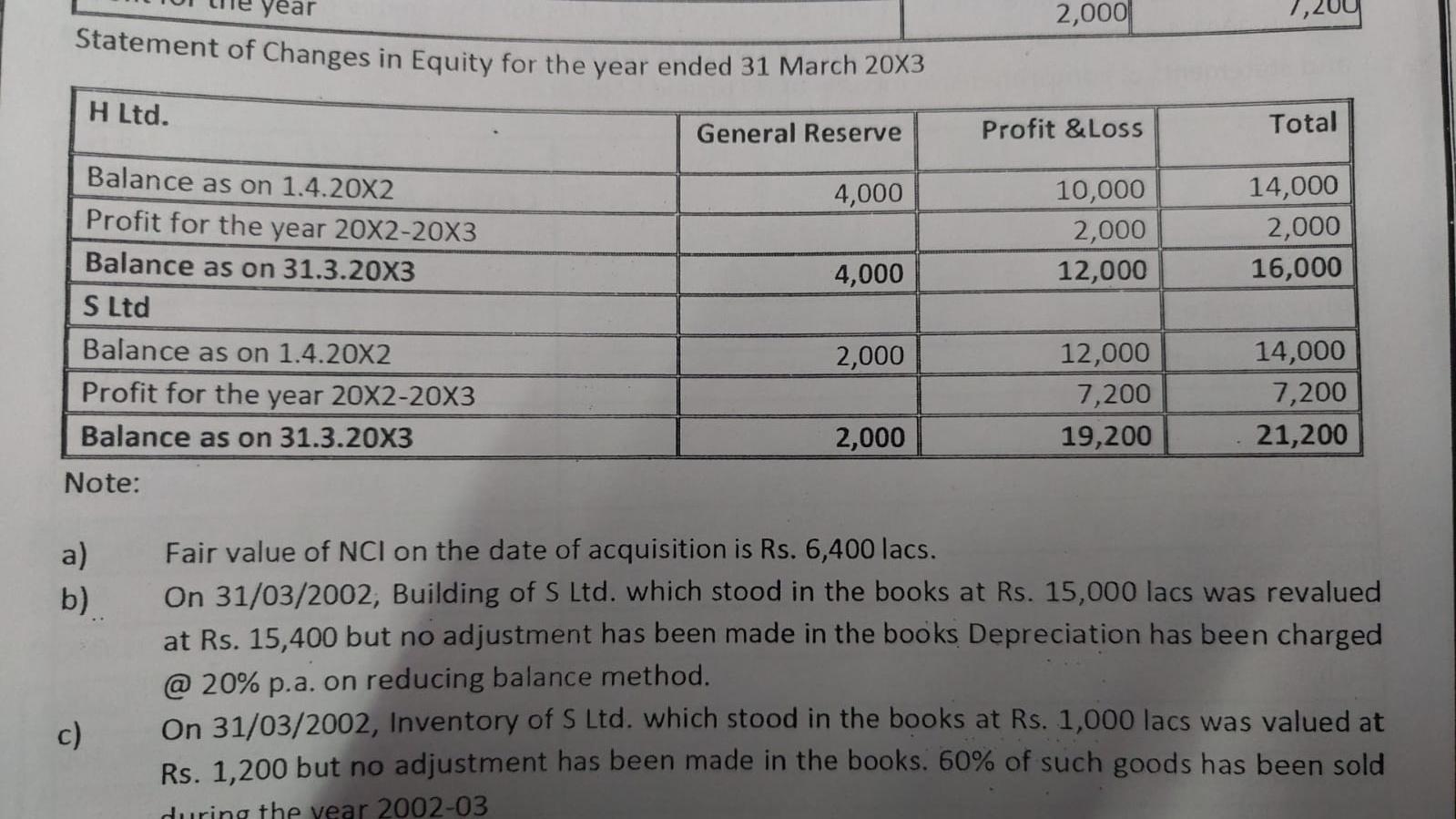

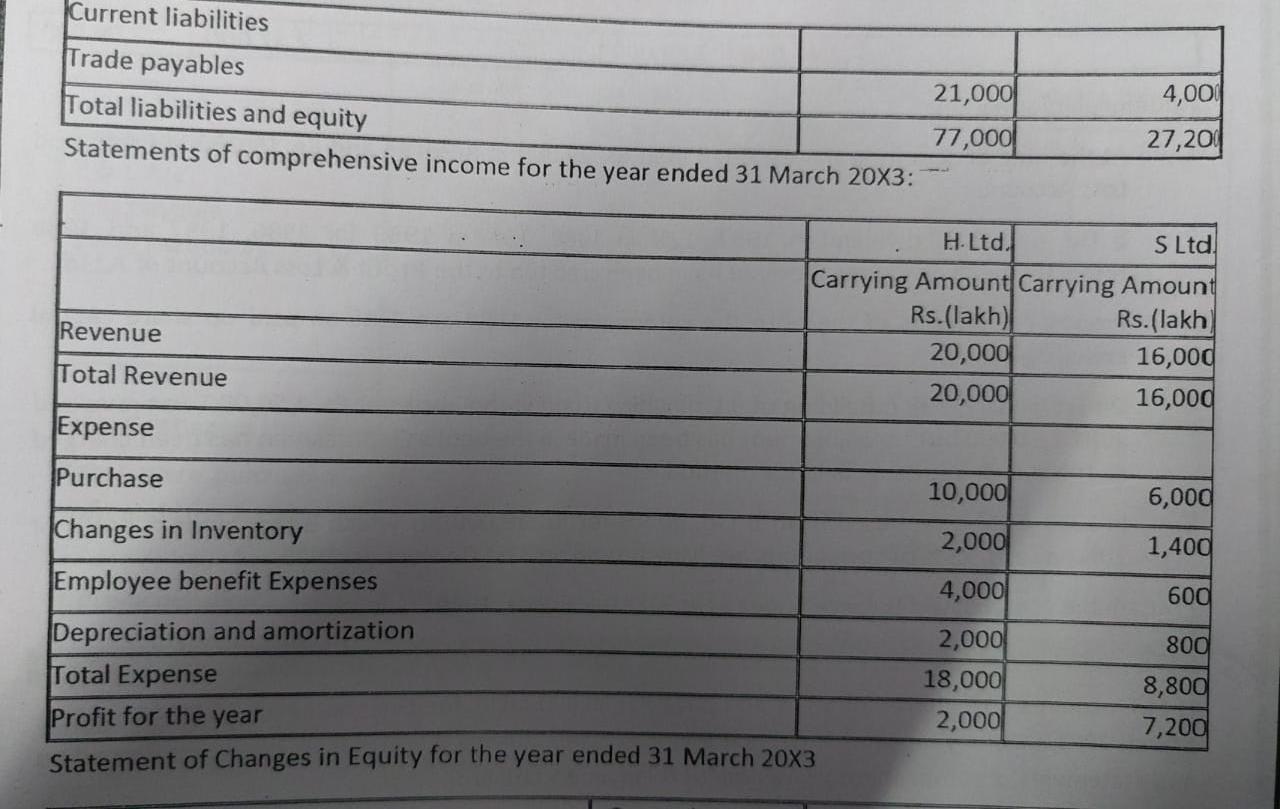

H Ltd. acquires 80% shares of S Ltd and pays Rs. 30,000 lakhs for the shares on 31/03/02. At 31 March 2003, i.e one year after H Ltd acquired S Ltd, the individual statements of financial position and statements of comprehensive income of H Ltd. and S Ltd. are: H Ltd: S Ltd. Carrying Amount Carrying Amount Rs.(lakh) Rs.(lakh) Assets INon-current assets Building and other PPE 12,000 40,000 30,000 Investment in S Ltd. 4,000 12,000 Other current assets Current assets 800 600 Inventories Trade receivables 1,000 1,000 1,600 27,200 1,200 77,000 Cash Total assets Equity and liabilities Equity Ishare canital 40,000 2,000 21 20 H Ltd. acquires 80% shares of S Ltd and pays Rs. 30,000 lakhs for the shares on 31/03/02. At 31 March 2003, i.e one year after H Ltd acquired s Ltd, the individual statements of financial position and statements of comprehensive income of H Ltd. and S Ltd. are: H Ltd: Carrying Amount Carrying Amount Rs.(lakh) Rs.(lakh) S Ltd Assets Non-current assets Building and other PPE 40,000 12,000 Investment in S Ltd. 30,000 Other current assets 4,000 12,000 Current assets Inventories 800 600 Trade receivables 1,000 Cash 1,200 1,000 1,600 27,200 Total assets 77,000 Equity and liabilities Equity Share capital Other Equity 40,000 16,000 2,000 21,200 year 2,000 Statement of Changes in Equity for the year ended 31 March 20X3 H Ltd. General Reserve Profit & Loss Total 4,000 10,000 2,000 12,000 14,000 2,000 16,000 4,000 Balance as on 1.4.20X2 Profit for the year 20X2-20X3 Balance as on 31.3.20X3 S Ltd Balance as on 1.4.20X2 Profit for the year 20X2-20X3 Balance as on 31.3.20X3 2,000 12,000 7,200 19,200 14,000 7,200 21,200 2,000 Note: a) b) Fair value of NCI on the date of acquisition is Rs. 6,400 lacs. On 31/03/2002, Building of S Ltd. which stood in the books at Rs. 15,000 lacs was revalued at Rs. 15,400 but no adjustment has been made in the books Depreciation has been charged @ 20% p.a. on reducing balance method. On 31/03/2002, Inventory of S Ltd. which stood in the books at Rs. 1,000 lacs was valued at Rs. 1,200 but no adjustment has been made in the books. 60% of such goods has been sold during the year 2002-03 c) Current liabilities Trade payables 21,000 4,001 Total liabilities and equity 77,000 27,201 Statements of comprehensive income for the year ended 31 March 20X3: H.Ltd. SLtd. Carrying Amount Carrying Amount Rs.(lakh) Rs.(lakh Revenue 20,000 16,000 Total Revenue 20,000 16,000 Expense Purchase 10,000 6,000 Changes in Inventory 2,000 1,400 4,000 600 Employee benefit Expenses Depreciation and amortization Total Expense Profit for the year Statement of Changes in Equity for the year ended 31 March 20x3 2,000 18,000 2,000 800 8,800 7,200 4,000 12,000 16,000 OX3 S Ltd Balance as on 1.4.20X2 Profit for the year 20X2-20X3 Balance as on 31.3.20X3 2,000 12,000 7,200 19,200 14,000 7,200 21,200 2,000 Note: a) b) c) Fair value of NCI on the date of acquisition is Rs. 6,400 lacs. On 31/03/2002, Building of s Ltd, which stood in the books at Rs. 15,000 lacs was revalued at Rs. 15,400 but no adjustment has been made in the books Depreciation has been charged @ 20% p.a. on reducing balance method. On 31/03/2002, Inventory of S Ltd. which stood in the books at Rs. 1,000 lacs was valued at Rs. 1,200 but no adjustment has been made in the books. 60% of such goods has been sold during the year 2002-03 In 2002-03 S Ltd. Purchased from H Ltd. goods for Rs. 1,000 lacs on which H Ltd. made a profit of 20% on sales, 25% of such goods are lying unsold on 31st March, 2003. Creditor of S Ltd include Rs. 200 lacs payable to H Ltd. d) e) H is unable to make a reliable estimate of the useful life of goodwill and consequently, the useful life is presumed to be ten years. H uses the straight-line amortisation method for goodwill. of hot sett (R) the Fear vale of building & other ren es upward revalined by a quo halda Prepare the Consolidated Balance Sheet as on March 31, 20X3 of group of entities A 200

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts