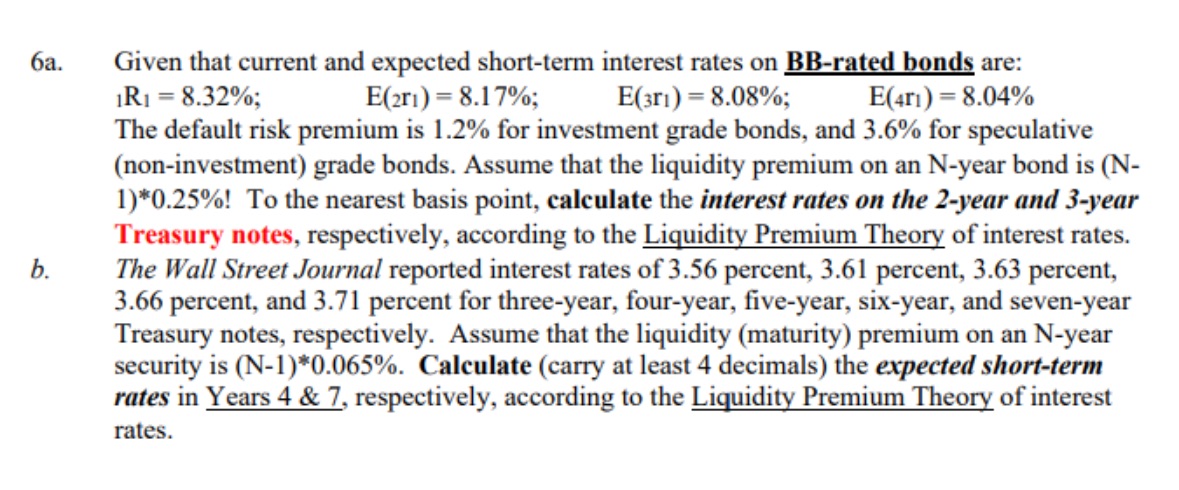

Question: Please don't use ChatGPT - please show your work- handwritten would be preferable. Also, please round to 4 decimal points. ? 6a. Given that current

Please don't use ChatGPT - please show your work- handwritten would be preferable. Also, please round to 4 decimal points. ?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock