Question: Please don't use excel and write in clear handwriting Question 2 You were in making met and the free rate of returns and the manner.

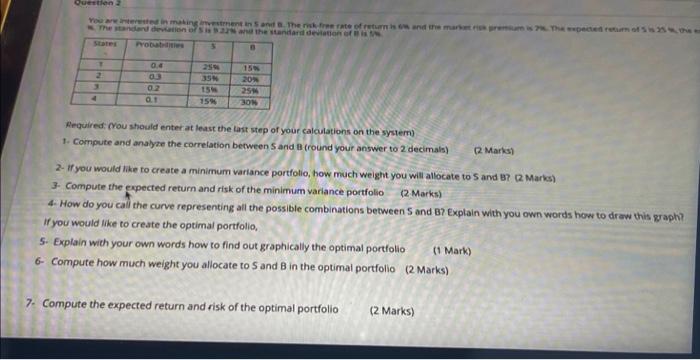

Question 2 You were in making met and the free rate of returns and the manner. The secret of the The standard deviation on the standard deviation of Proba 5 2 elele 02 QT 259 35 154 15% 15 20 25 30 Required you should enter at least the last step of your calculations on the system) 1. Compute and analyze the correlation between Sanid (round your answer to 2 decimals) 2 Marks) 2. If you would like to create a minimum variance portfolio, how much weight you will allocate to S avd B? (2. Marks) 3- Compute the expected return and risk of the minimum variance portfolio 2 Marks) 4. How do you call the curve representing all the possible combinations between S and B? Explain with you own words how to draw this graphia If you would like to create the optimal portfolio S- Explain with your own words how to find out graphically the optimal portfolio (1 Mark) 6- Compute how much weight you allocate to S and B in the optimal portfolio (2 Marks) 7. Compute the expected return and risk of the optimal portfolio (2 Marks) Question 2 You were in making met and the free rate of returns and the manner. The secret of the The standard deviation on the standard deviation of Proba 5 2 elele 02 QT 259 35 154 15% 15 20 25 30 Required you should enter at least the last step of your calculations on the system) 1. Compute and analyze the correlation between Sanid (round your answer to 2 decimals) 2 Marks) 2. If you would like to create a minimum variance portfolio, how much weight you will allocate to S avd B? (2. Marks) 3- Compute the expected return and risk of the minimum variance portfolio 2 Marks) 4. How do you call the curve representing all the possible combinations between S and B? Explain with you own words how to draw this graphia If you would like to create the optimal portfolio S- Explain with your own words how to find out graphically the optimal portfolio (1 Mark) 6- Compute how much weight you allocate to S and B in the optimal portfolio (2 Marks) 7. Compute the expected return and risk of the optimal portfolio (2 Marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts