Question: please explain (c) and (d) to me Question 3 (8 marks) Karim is deciding whether to invest his capital in the Carletto Fund or the

please explain (c) and (d) to me

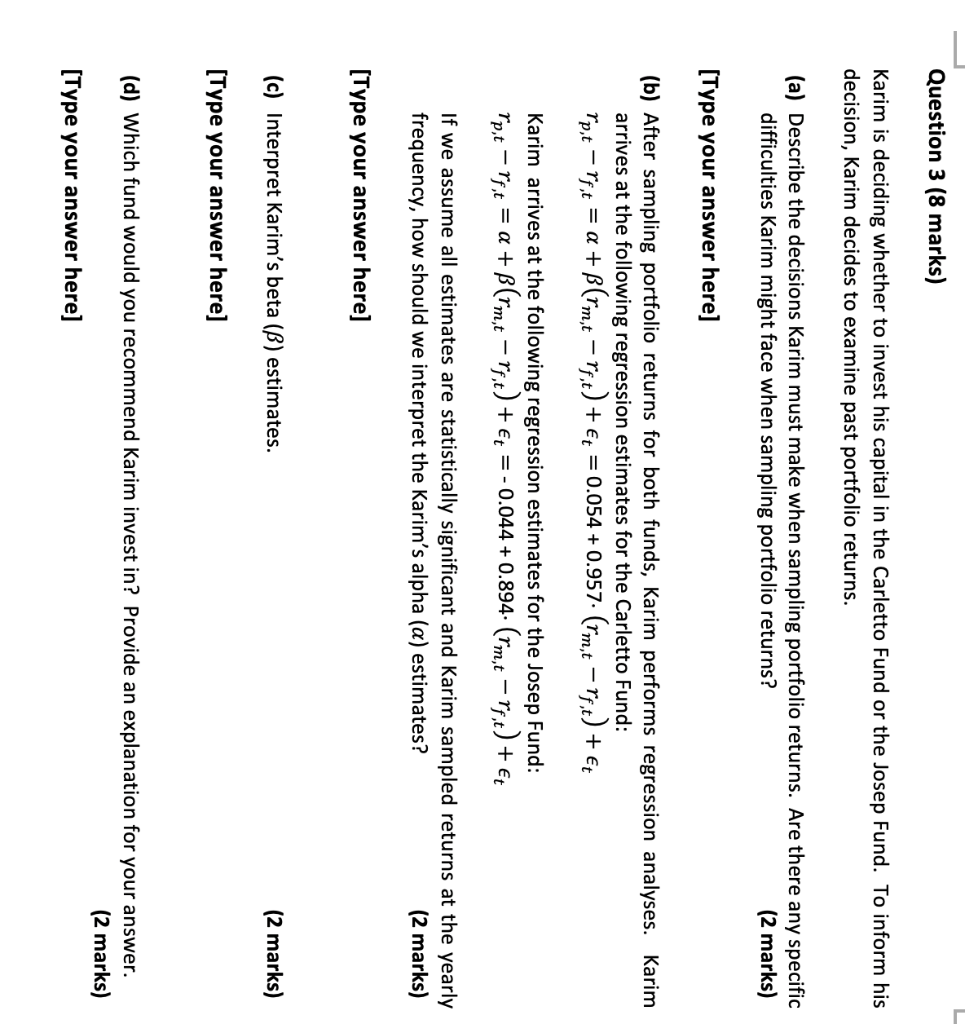

Question 3 (8 marks) Karim is deciding whether to invest his capital in the Carletto Fund or the Josep Fund. To inform his decision, Karim decides to examine past portfolio returns. (a) Describe the decisions Karim must make when sampling portfolio returns. Are there any specific difficulties Karim might face when sampling portfolio returns? (2 marks) [Type your answer here] (b) After sampling portfolio returns for both funds, Karim performs regression analyses. Karim arrives at the following regression estimates for the Carletto Fund: rp,t = rft = a + (rmt - rft) + = 0.054 +0.957. (rm,t Tt) + Karim arrives at the following regression estimates for the Josep Fund: Tp,t = rft = + (rm,t rft) + t = -0.044 +0.894. (rmt rf,t) + Et - - If we assume all estimates are statistically significant and Karim sampled returns at the yearly frequency, how should we interpret the Karim's alpha (a) estimates? (2 marks) [Type your answer here] (c) Interpret Karim's beta (B) estimates. (2 marks) [Type your answer here] (d) Which fund would you recommend Karim invest in? Provide an explanation for your answer. (2 marks) [Type your answer here] Question 3 (8 marks) Karim is deciding whether to invest his capital in the Carletto Fund or the Josep Fund. To inform his decision, Karim decides to examine past portfolio returns. (a) Describe the decisions Karim must make when sampling portfolio returns. Are there any specific difficulties Karim might face when sampling portfolio returns? (2 marks) [Type your answer here] (b) After sampling portfolio returns for both funds, Karim performs regression analyses. Karim arrives at the following regression estimates for the Carletto Fund: rp,t = rft = a + (rmt - rft) + = 0.054 +0.957. (rm,t Tt) + Karim arrives at the following regression estimates for the Josep Fund: Tp,t = rft = + (rm,t rft) + t = -0.044 +0.894. (rmt rf,t) + Et - - If we assume all estimates are statistically significant and Karim sampled returns at the yearly frequency, how should we interpret the Karim's alpha (a) estimates? (2 marks) [Type your answer here] (c) Interpret Karim's beta (B) estimates. (2 marks) [Type your answer here] (d) Which fund would you recommend Karim invest in? Provide an explanation for your answer. (2 marks) [Type your answer here]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts