Question: Please explain how this answer is reached. Without the use of appendix tables or a financial calculator or excel - for an exam. can use

Please explain how this answer is reached. Without the use of appendix tables or a financial calculator or excel - for an exam.

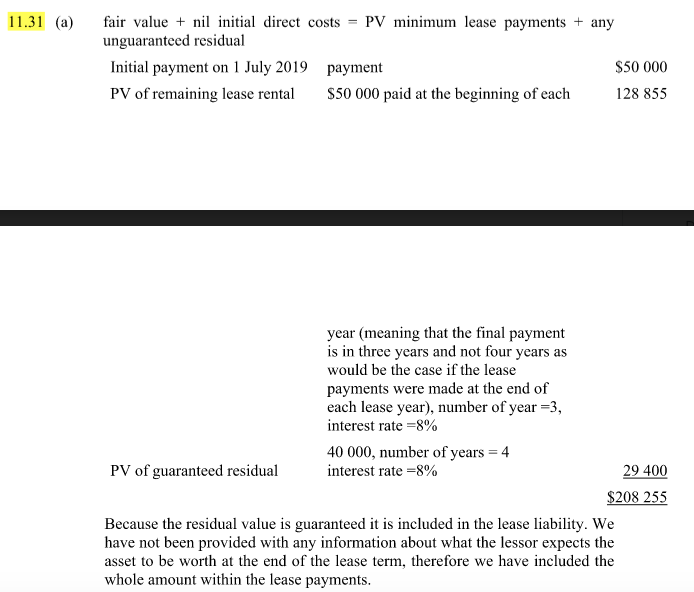

31. Hopeful Ltd leased a portable sound recording studio from Lessor Ltd. Lessor has no material initial direct costs. Hopeful Ltd does not plan to acquire the portable studio at the end of the lease because it expects that, by then, it will need a larger studio. The terms of the lease are as follows: Date of entering lease: 1 July 2019. Duration of lease: four years. Life of leased asset: five years. Lease payments: $50 000 at the beginning of each year. First lease payment: 1 July 2019. Lease expires: 1 July 2023. Interest rate implicit in the lease: 8 per cent Guaranteed residual: $40 000. REQUIRED (a) Determine the fair value of the portable sound recording studio at 1 July 2019. LO 11.7 11.10 fair valuenil initial direct costs = unguaranteed residual PV minimum lease payments + any 11.31 (a) Initial payment on 1 July 2019 payment $50 000 128 855 PV of remaining lease rental $50 000 paid at the beginning of each year (meaning that the final payment is in three years and not four years as would be the case if the lease payments were made at the end of each lease year), number of year 3, interest rate 8% 40 000, number of years interest rate-8% 4 29 400 PV of guaranteed residual $208 255 Because the residual value is guaranteed it is included in the lease liability. We have not been provided with any information about what the lessor expects the asset to be worth at the end of the lease term, therefore we have included the whole amount within the lease payments. 31. Hopeful Ltd leased a portable sound recording studio from Lessor Ltd. Lessor has no material initial direct costs. Hopeful Ltd does not plan to acquire the portable studio at the end of the lease because it expects that, by then, it will need a larger studio. The terms of the lease are as follows: Date of entering lease: 1 July 2019. Duration of lease: four years. Life of leased asset: five years. Lease payments: $50 000 at the beginning of each year. First lease payment: 1 July 2019. Lease expires: 1 July 2023. Interest rate implicit in the lease: 8 per cent Guaranteed residual: $40 000. REQUIRED (a) Determine the fair value of the portable sound recording studio at 1 July 2019. LO 11.7 11.10 fair valuenil initial direct costs = unguaranteed residual PV minimum lease payments + any 11.31 (a) Initial payment on 1 July 2019 payment $50 000 128 855 PV of remaining lease rental $50 000 paid at the beginning of each year (meaning that the final payment is in three years and not four years as would be the case if the lease payments were made at the end of each lease year), number of year 3, interest rate 8% 40 000, number of years interest rate-8% 4 29 400 PV of guaranteed residual $208 255 Because the residual value is guaranteed it is included in the lease liability. We have not been provided with any information about what the lessor expects the asset to be worth at the end of the lease term, therefore we have included the whole amount within the lease payments

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts