Question: Please explain how to do #3 by hand WITHOUT USING EXCEL Use this data for problems 1-4. The monthly returns for securities A, B, C,

Please explain how to do #3 by hand WITHOUT USING EXCEL

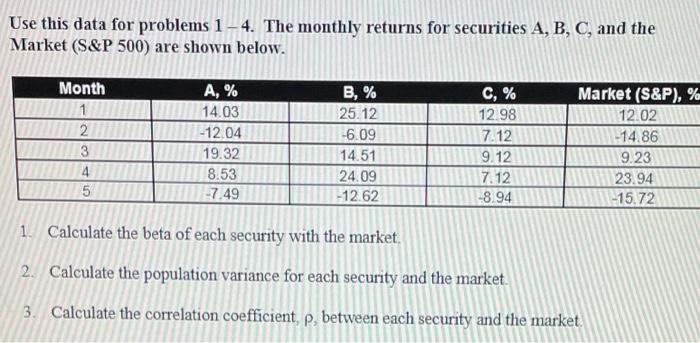

Use this data for problems 1-4. The monthly returns for securities A, B, C, and the Market (S&P 500) are shown below. Month 1 2 3 4 5 A, % 14.03 -12.04 19.32 8.53 -7.49 B, % 25.12 -6.09 14.51 24.09 -12.62 C, % 12.98 7.12 9.12 7.12 -8.94 Market (S&P), % 12.02 -14.86 9.23 23.94 -15.72 1. Calculate the beta of each security with the market. 2. Calculate the population variance for each security and the market. 3. Calculate the correlation coefficient, p, between each security and the market

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock