Question: Please explain how to get the impairment loss Shown below are the Taccounts relating to equipment that was purchased for cash by a company on

Please explain how to get the impairment loss

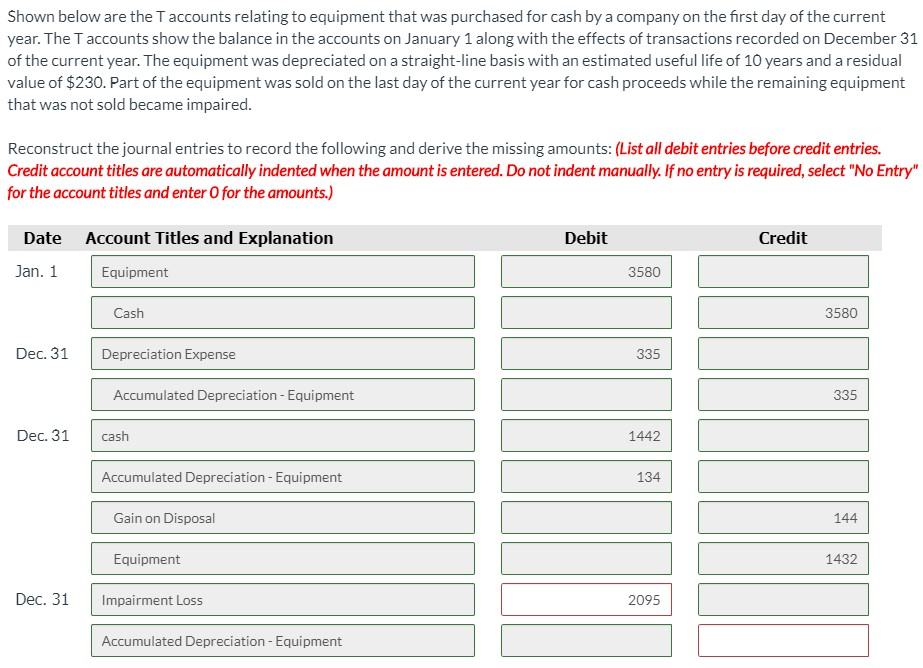

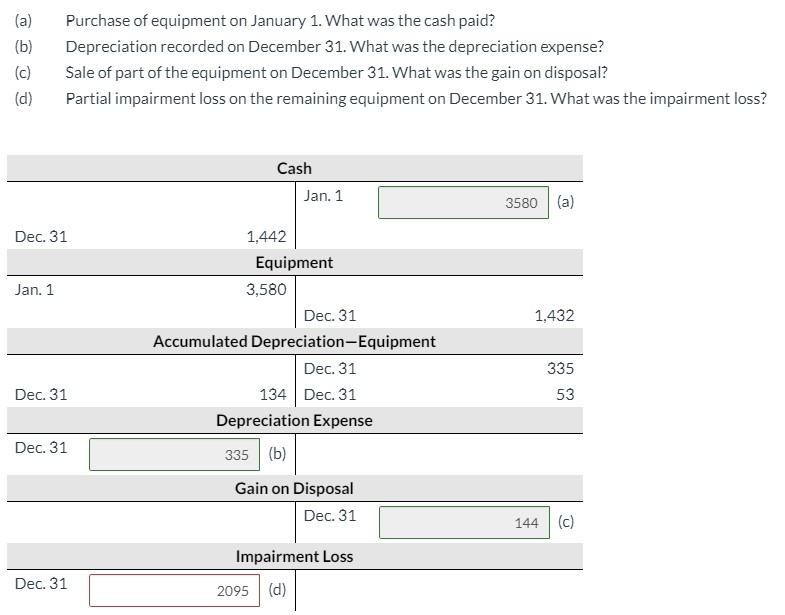

Shown below are the Taccounts relating to equipment that was purchased for cash by a company on the first day of the current year. The Taccounts show the balance in the accounts on January 1 along with the effects of transactions recorded on December 31 of the current year. The equipment was depreciated on a straight-line basis with an estimated useful life of 10 years and a residual value of $230. Part of the equipment was sold on the last day of the current year for cash proceeds while the remaining equipment that was not sold became impaired. Reconstruct the journal entries to record the following and derive the missing amounts: (List all debit entries before credit entries. Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter for the amounts.) Date Account Titles and Explanation Debit Credit Jan. 1 Equipment 3580 Cash 3580 Dec. 31 Depreciation Expense 335 Accumulated Depreciation - Equipment 335 Dec. 31 cash 1442 Accumulated Depreciation - Equipment 134 Gain on Disposal 144 Equipment 1432 Dec. 31 Impairment Loss 2095 Accumulated Depreciation - Equipment (a) (b) (c) (d) Purchase of equipment on January 1. What was the cash paid? Depreciation recorded on December 31. What was the depreciation expense? Sale of part of the equipment on December 31. What was the gain on disposal? Partial impairment loss on the remaining equipment on December 31. What was the impairment loss? Cash Jan. 1 3580 (a) Dec. 31 Jan. 1 1,432 335 1,442 Equipment 3,580 Dec. 31 Accumulated Depreciation-Equipment Dec. 31 134 Dec. 31 Depreciation Expense 335 (b) Gain on Disposal Dec. 31 Dec. 31 53 Dec. 31 144 (c) Impairment Loss Dec. 31 2095 (d)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts