Question: Please explain steps in exel Question 2: Three assets have the following means and variance-covariance matrix. The portfolio weights on the three assets for Portfolio

Please explain steps in exel

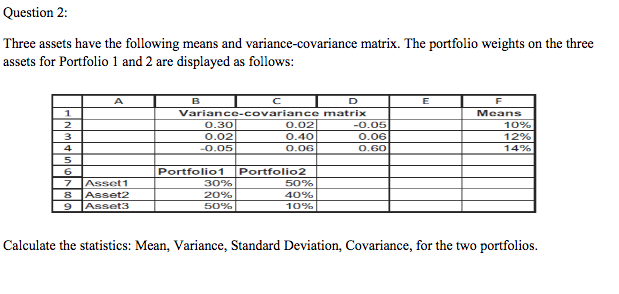

Question 2: Three assets have the following means and variance-covariance matrix. The portfolio weights on the three assets for Portfolio 1 and 2 are displayed as follows Variance-covariance matrix Means 0.02 0.40 0.06 0.05 0.06 0.60 0.30 10% 0.02 0.05 14% 5 6 7 Asset 1 8 Asset2 9 Asset3 Portfolio1 Portfolio2 30% 2096 50% 40% Calculate the statistics: Mean, Variance, Standard Deviation, Covariance, for the two portfolios

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock