Question: please explain the rows on the table dividends from hybrid tax loss carry-forwardsetc. Question 1) I dont know where the numbers were derived from .

please explain the rows on the table "dividends from hybrid" "tax loss carry-forwards"etc. Question 1) I dont know where the numbers were derived from . For example how was the year 2 dividends calculated as 12,800,000. Please show full calculations and dont skip steps

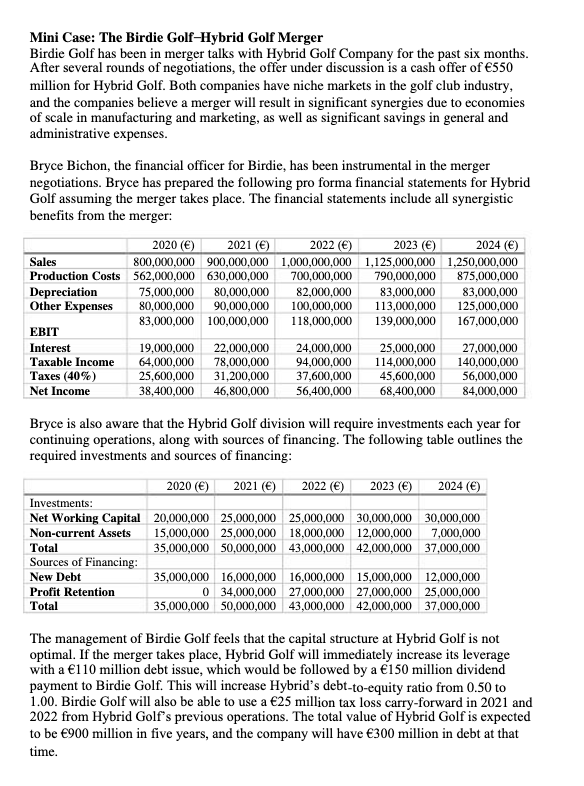

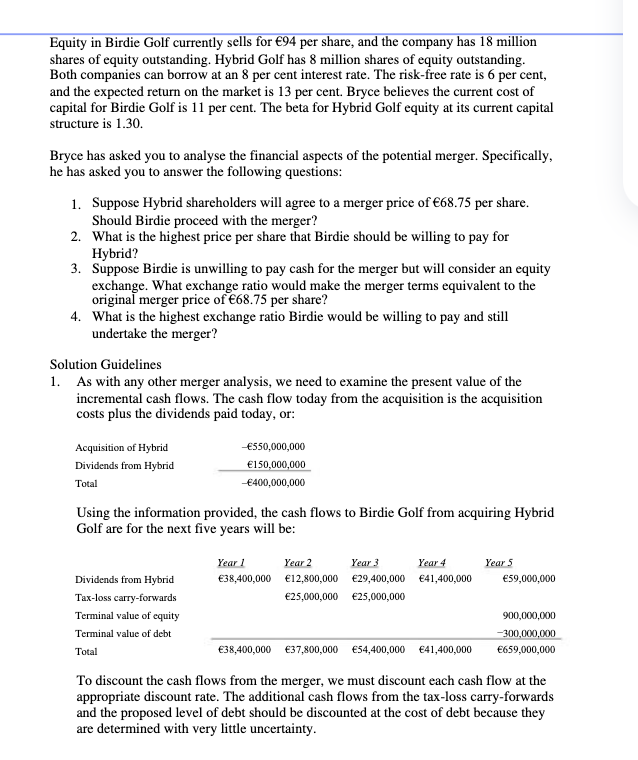

Mini Case: The Birdie GolfHybrid Golf Merger Birdie Golf has been in merger talks with Hybrid Golf Company for the past six months. After several rounds of negotiations, the offer under discussion is a cash offer of 550 million for Hybrid Golf. Both companies have niche markets in the golf club industry, and the companies believe a merger will result in significant synergies due to economies of scale in manufacturing and marketing, as well as significant savings in general and administrative expenses. Bryce Bichon, the financial officer for Birdie, has been instrumental in the merger negotiations. Bryce has prepared the following pro forma financial statements for Hybrid Golf assuming the merger takes place. The financial statements include all synergistic benefits from the merger: 2020 () 2021 () 2022 () 2023 () 2024 () Sales 00,000,000 900,000,000 1,000,000,000 1,125,000,000 1,250,000,000 Production Costs 562,000.000 630,000,000 700,000,000 790,000,000 875,000,000 Depreciation 75,000,000 80,000,000 #2,000,000 83,000,000 3,000,000 Other Expenses 80,000,000 90,000,000 100,000,000 113,000,000 125,000,000 83,000,000 100,000,000 118,000,000 139,000,000 167,000,000 EBIT Interest 19,000,000 22,000,000 24,000,000 25,000,000 27,000,000 Taxable Income 64,000,000 78,000,000 94,000,000 114,000,000 140,000,000 Taxes (40%) 25,600,000 31,200,000 37,600,000 43,600,000 56,000,000 Net Income 38,400,000 46,800,000 56,400,000 65,400,000 84,000,000 Bryce is also aware that the Hybrid Golf division will require investments each year for continuing operations, along with sources of financing. The following table outlines the required investments and sources of financing: 2020 () 2021 () 2022 () 2023 () 2024 () Investments: Net Working Capital 20,000,000 25,000,000 25,000,000 30,000,000 30,000,000 Non-current Assets 15,000,000 25,000,000 18,000,000 12,000,000 7,000,000 Total 35,000,000 50,000,000 43,000,000 42,000,000 37,000,000 Sources of Financing: New Debt 35,000,000 16,000,000 16,000,000 15,000,000 12,000,000 Profit Retention 0 34,000,000 27,000,000 27,000,000 25,000,000 Total 35,000,000 50,000,000 43,000,000 42,000,000 37,000,000 The management of Birdie Golf feels that the capital structure at Hybrid Golf is not optimal. If the merger takes place, Hybrid Golf will immediately increase its leverage with a 110 million debt issue, which would be followed by a 150 million dividend payment to Birdie Golf. This will increase Hybrid's debt-to-equity ratio from 0.50 1o 1.00. Birdie Golf will also be able to use a 25 million tax loss carry-forward in 2021 and 2022 from Hybrid Golf's previous operations. The total value of Hybrid Golf is expected to be 900 million in five years, and the company will have 300 million in debt at that time. Equity in Birdie Golf currently sells for 94 per share, and the company has 18 million shares of equity outstanding. Hybrid Golf has 8 million shares of equity outstanding, Both companies can borrow at an 8 per cent interest rate. The risk-free rate is 6 per cent, and the expected return on the market is 13 per cent. Bryce believes the current cost of capital for Birdie Golf is 11 per cent. The beta for Hybrid Golf equity at its current capital structure is 1.30. Bryce has asked you to analyse the financial aspects of the potential merger. Specifically, he has asked you to answer the following questions: 1. Suppose Hybrid sharecholders will agree to a merger price of 68.75 per share. Should Birdie proceed with the merger? 2. What is the highest price per share that Birdie should be willing to pay for Hybrid? 3. Suppose Birdie is unwilling to pay cash for the merger but will consider an equity exchange. What exchange ratio would make the merger terms equivalent to the original merger price of 68.75 per share? 4. What is the highest exchange ratio Birdie would be willing to pay and still undertake the merger? Solution Guidelines 1. As with any other merger analysis, we need to examine the present value of the incremental cash flows. The cash flow today from the acquisition is the acquisition costs plus the dividends paid today, or: Acquisition of Hybrid 550,000,000 Dividends from Hybrid ~ 150,000, 000 Total E4040, 000,000 Using the information provided, the cash flows to Birdie Golf from acquiring Hybrid Golf are for the next five years will be: Year 1 Year 2 Year 3 Yeard Year 5 Dividends from Hybrid 38,400,000 12,300,00 29.400,000 41,400,000 39,000,000 Tax-loss carry-forwards 25,000,000 25, 000,000 Terminal value of equity SO0, 00N, 000 Terminal value of debt 300, D00, 000 Toeal 38400,000 37,800,000 54,400,000 41,400,000 659,000,000 To discount the cash flows from the merger, we must discount each cash flow at the appropriate discount rate. The additional cash flows from the tax-loss carry-forwards and the proposed level of debt should be discounted at the cost of debt because they are determined with very little uncertainty

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!