Question: Please explain this as simple as possible (ii) Let P(t) denote the time 0 price for a European put option maturing at time t and

Please explain this as simple as possible

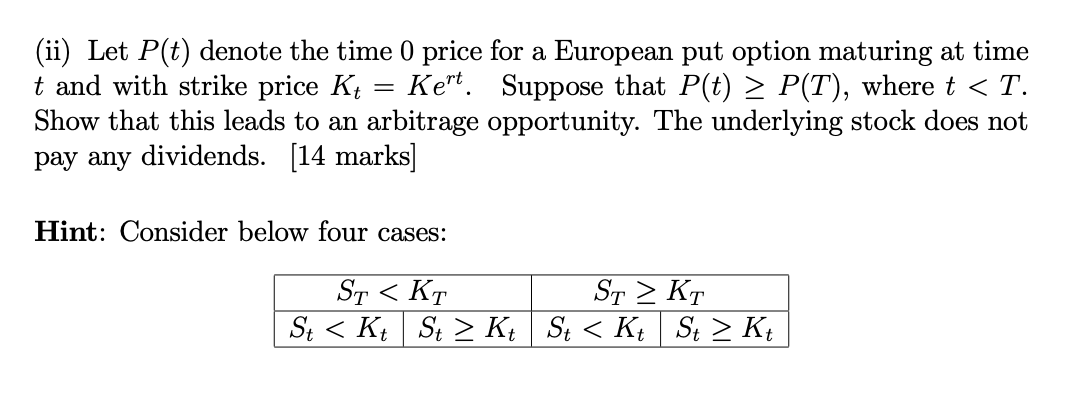

(ii) Let P(t) denote the time 0 price for a European put option maturing at time t and with strike price Kt=Kert. Suppose that P(t)P(T), where t

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock