Question: Please explain which steps I need to take to solve this with calculations. Hope you can help! The balance sheets of Parent Company and Subsid

Please explain which steps I need to take to solve this with calculations. Hope you can help!

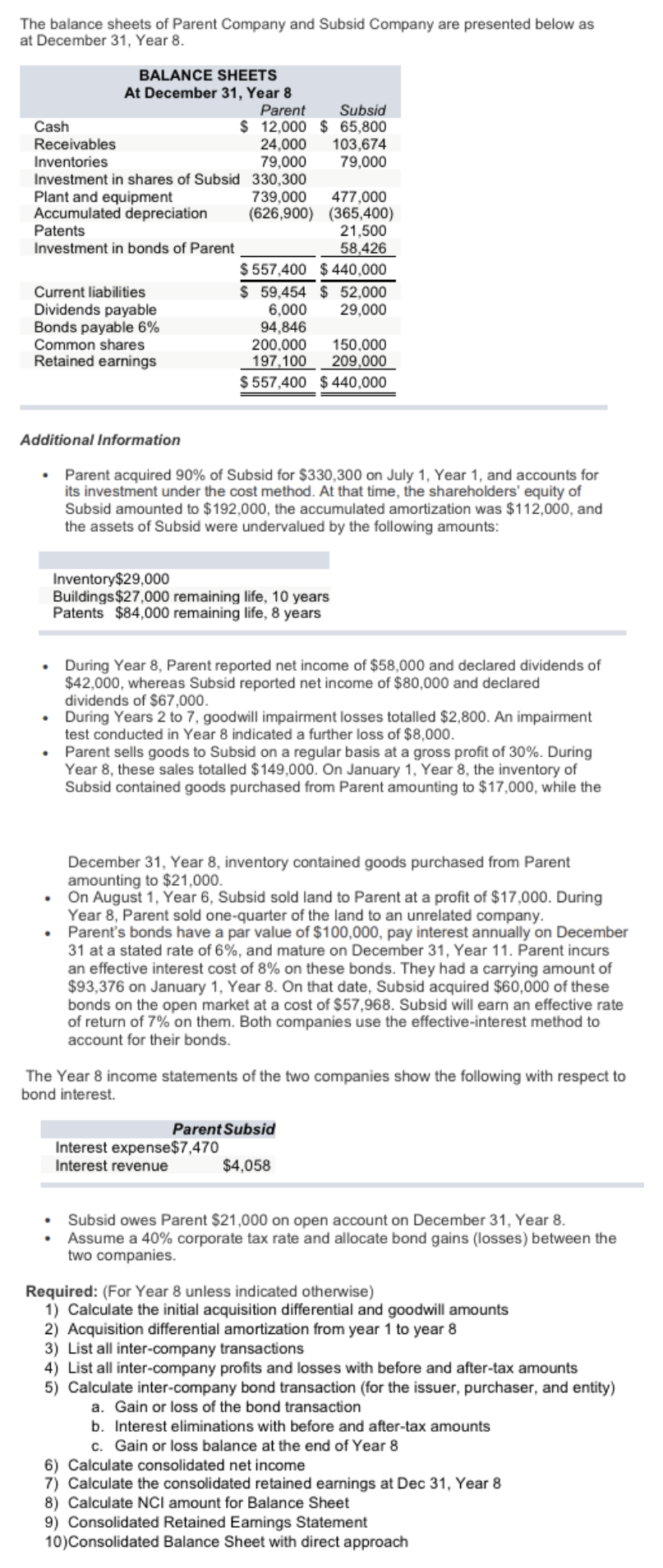

The balance sheets of Parent Company and Subsid Company are presented below as at December 31, Year 8. BALANCE SHEETS At December 31, Year 8 Parent Subsid $ 12,000 $ 65,800 Cash Receivables 24,000 103,674 Inventories 79,000 79,000 Investment in shares of Subsid 330,300 739,000 (626,900) Plant and equipment Accumulated depreciation Patents Investment in bonds of Parent Current liabilities Dividends payable Bonds payable 6% Common shares Retained earnings . 477,000 (365,400) 21,500 58,426 $557,400 $ 440,000 Additional Information Parent acquired 90% of Subsid for $330,300 on July 1, Year 1, and accounts for its investment under the cost method. At that time, the shareholders' equity of Subsid amounted to $192,000, the accumulated amortization was $112,000, and the assets of Subsid were undervalued by the following amounts: $ 59,454 $ 52,000 29,000 6,000 94,846 200,000 150,000 197,100 209,000 $557,400 $440,000 Inventory$29,000 Buildings $27,000 remaining life, 10 years Patents $84,000 remaining life, 8 years During Year 8, Parent reported net income of $58,000 and declared dividends of $42,000, whereas Subsid reported net income of $80,000 and declared dividends of $67,000. During Years 2 to 7, goodwill impairment losses totalled $2,800. An impairment test conducted in Year 8 indicated a further loss of $8,000. Parent sells goods to Subsid on a regular basis at a gross profit of 30%. During Year 8, these sales totalled $149,000. On January 1, Year 8, the inventory of Subsid contained goods purchased from Parent amounting to $17,000, while the December 31, Year 8, inventory contained goods purchased from Parent amounting to $21,000. On August 1, Year 6, Subsid sold land to Parent at a profit of $17,000. During Year 8, Parent sold one-quarter of the land to an unrelated company. Parent's bonds have a par value of $100,000, pay interest annually on December 31 at a stated rate of 6%, and mature on December 31, Year 11. Parent incurs an effective interest cost of 8% on these bonds. They had a carrying amount of $93,376 on January 1, Year 8. On that date, Subsid acquired $60,000 of these bonds on the open market at a cost of $57,968. Subsid will earn an effective rate of return of 7% on them. Both companies use the effective-interest method to account for their bonds. The Year 8 income statements of the two companies show the following with respect to bond interest. Interest expense$7,470 Interest revenue Parent Subsid $4,058 Subsid owes Parent $21,000 on open account on December 31, Year 8. Assume a 40% corporate tax rate and allocate bond gains (losses) between the two companies. Required: (For Year 8 unless indicated otherwise) 1) Calculate the initial acquisition differential and goodwill amounts 2) Acquisition differential amortization from year 1 to year 8 3) List all inter-company transactions 4) List all inter-company profits and losses with before and after-tax amounts 5) Calculate inter-company bond transaction (for the issuer, purchaser, and entity) a. Gain or loss of the bond transaction b. Interest eliminations with before and after-tax amounts c. Gain or loss balance at the end of Year 8 6) Calculate consolidated net income 7) Calculate the consolidated retained earnings at Dec 31, Year 8 8) Calculate NCI amount for Balance Sheet 9) Consolidated Retained Earnings Statement 10)Consolidated Balance Sheet with direct approach The balance sheets of Parent Company and Subsid Company are presented below as at December 31, Year 8. BALANCE SHEETS At December 31, Year 8 Parent Subsid $ 12,000 $ 65,800 Cash Receivables 24,000 103,674 Inventories 79,000 79,000 Investment in shares of Subsid 330,300 739,000 (626,900) Plant and equipment Accumulated depreciation Patents Investment in bonds of Parent Current liabilities Dividends payable Bonds payable 6% Common shares Retained earnings . 477,000 (365,400) 21,500 58,426 $557,400 $ 440,000 Additional Information Parent acquired 90% of Subsid for $330,300 on July 1, Year 1, and accounts for its investment under the cost method. At that time, the shareholders' equity of Subsid amounted to $192,000, the accumulated amortization was $112,000, and the assets of Subsid were undervalued by the following amounts: $ 59,454 $ 52,000 29,000 6,000 94,846 200,000 150,000 197,100 209,000 $557,400 $440,000 Inventory$29,000 Buildings $27,000 remaining life, 10 years Patents $84,000 remaining life, 8 years During Year 8, Parent reported net income of $58,000 and declared dividends of $42,000, whereas Subsid reported net income of $80,000 and declared dividends of $67,000. During Years 2 to 7, goodwill impairment losses totalled $2,800. An impairment test conducted in Year 8 indicated a further loss of $8,000. Parent sells goods to Subsid on a regular basis at a gross profit of 30%. During Year 8, these sales totalled $149,000. On January 1, Year 8, the inventory of Subsid contained goods purchased from Parent amounting to $17,000, while the December 31, Year 8, inventory contained goods purchased from Parent amounting to $21,000. On August 1, Year 6, Subsid sold land to Parent at a profit of $17,000. During Year 8, Parent sold one-quarter of the land to an unrelated company. Parent's bonds have a par value of $100,000, pay interest annually on December 31 at a stated rate of 6%, and mature on December 31, Year 11. Parent incurs an effective interest cost of 8% on these bonds. They had a carrying amount of $93,376 on January 1, Year 8. On that date, Subsid acquired $60,000 of these bonds on the open market at a cost of $57,968. Subsid will earn an effective rate of return of 7% on them. Both companies use the effective-interest method to account for their bonds. The Year 8 income statements of the two companies show the following with respect to bond interest. Interest expense$7,470 Interest revenue Parent Subsid $4,058 Subsid owes Parent $21,000 on open account on December 31, Year 8. Assume a 40% corporate tax rate and allocate bond gains (losses) between the two companies. Required: (For Year 8 unless indicated otherwise) 1) Calculate the initial acquisition differential and goodwill amounts 2) Acquisition differential amortization from year 1 to year 8 3) List all inter-company transactions 4) List all inter-company profits and losses with before and after-tax amounts 5) Calculate inter-company bond transaction (for the issuer, purchaser, and entity) a. Gain or loss of the bond transaction b. Interest eliminations with before and after-tax amounts c. Gain or loss balance at the end of Year 8 6) Calculate consolidated net income 7) Calculate the consolidated retained earnings at Dec 31, Year 8 8) Calculate NCI amount for Balance Sheet 9) Consolidated Retained Earnings Statement 10)Consolidated Balance Sheet with direct approach

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts