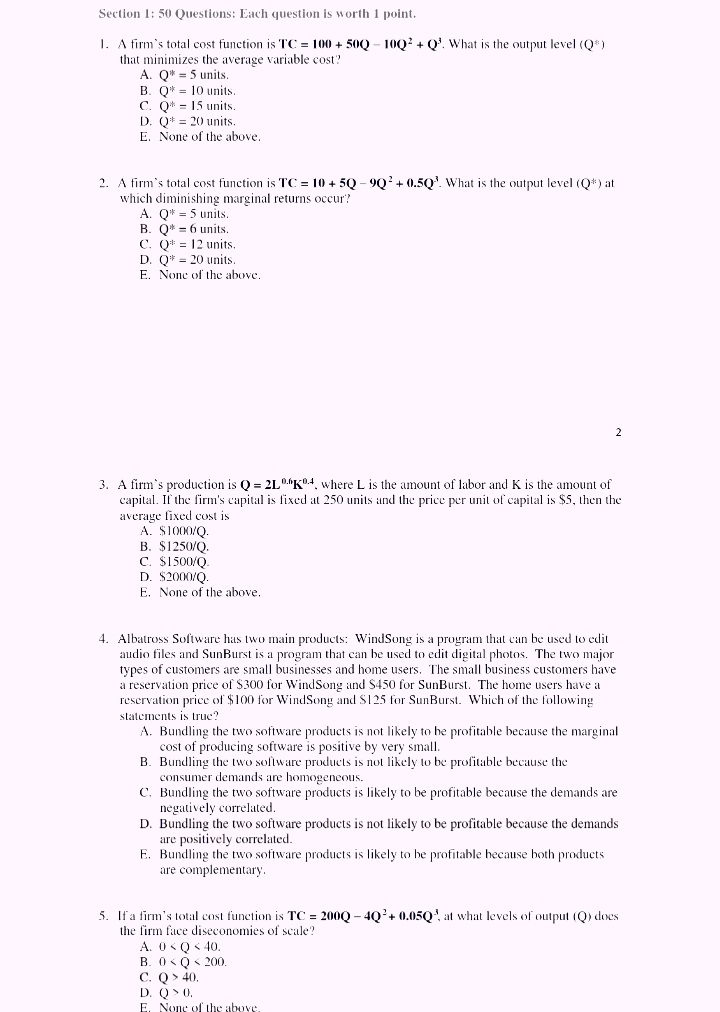

Question: Please find the attached multiple choice questions: Answers and explanations please. 25. A firm in monopolistic market faces the following demand and total cost equations

Please find the attached multiple choice questions:

Answers and explanations please.

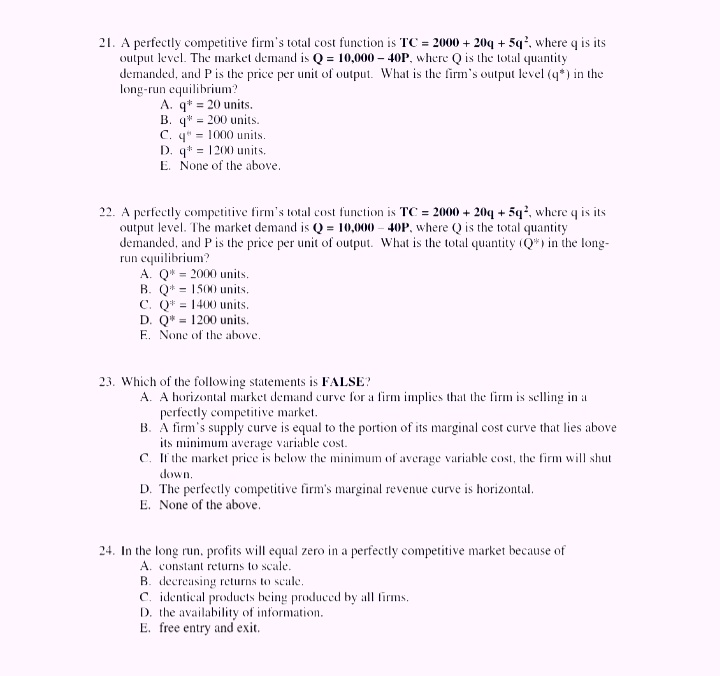

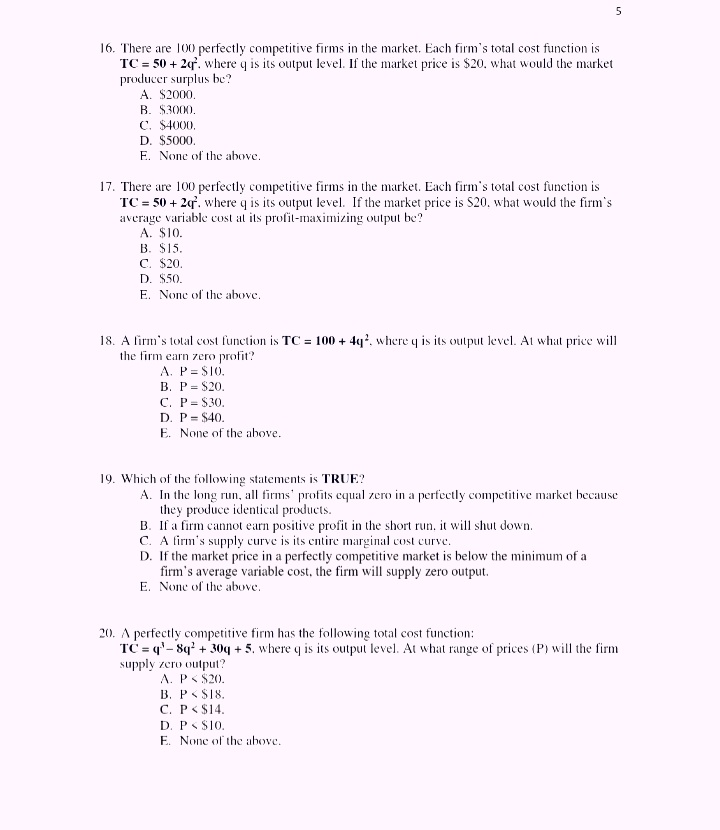

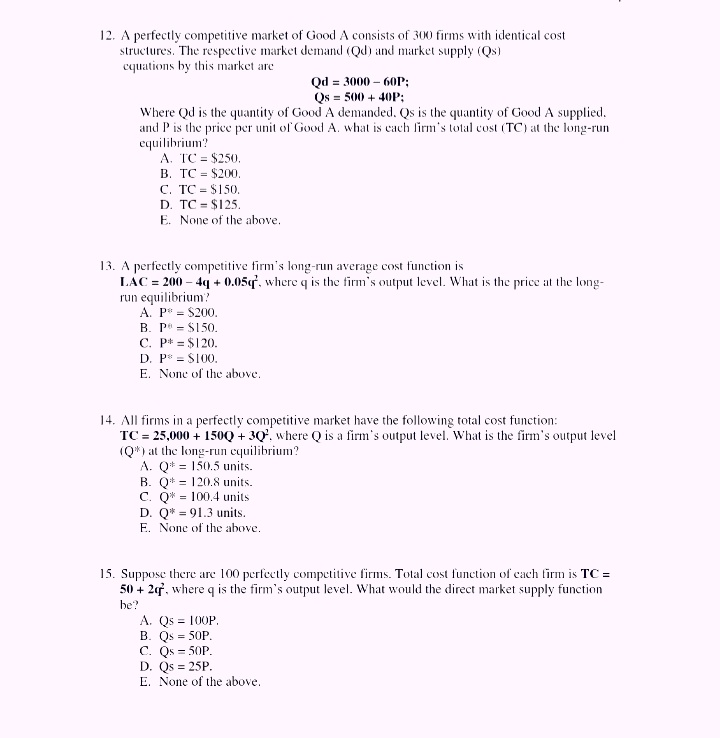

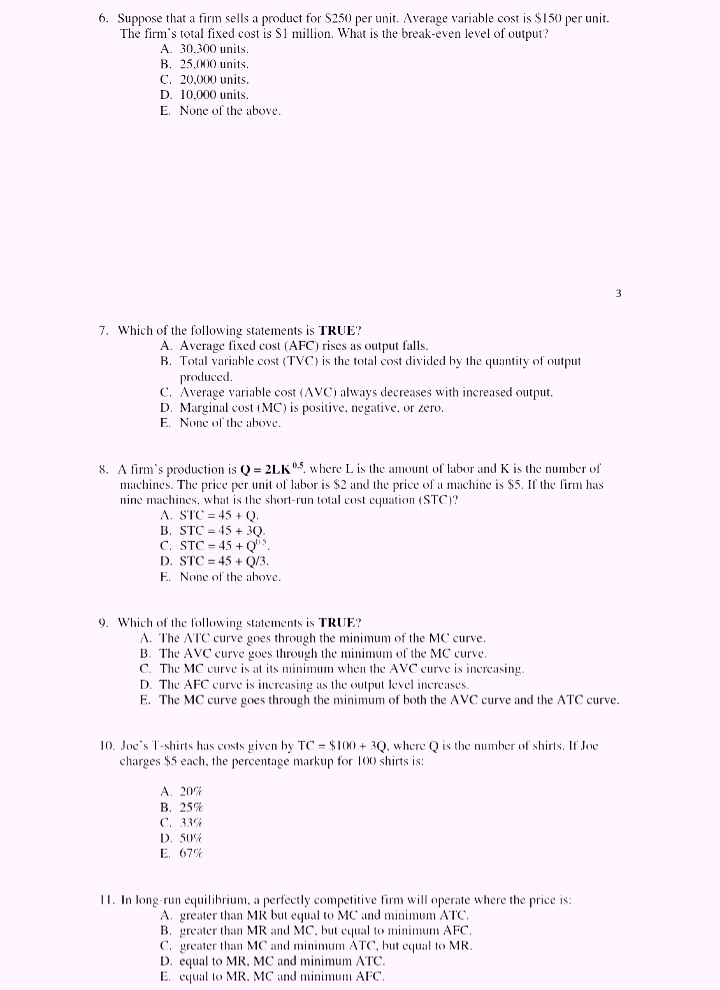

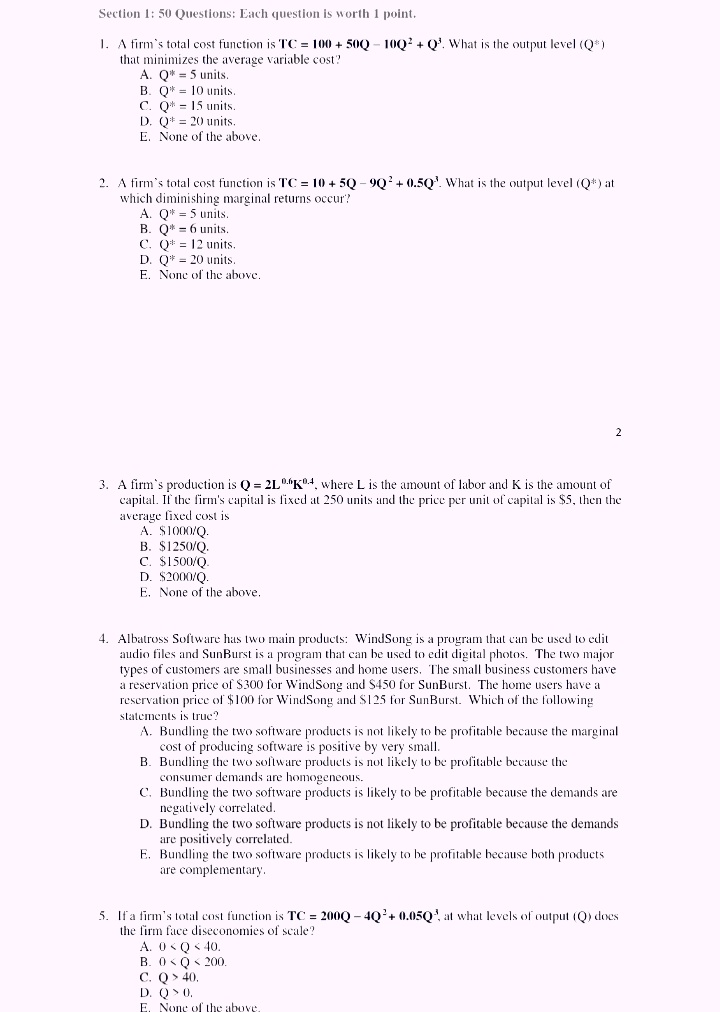

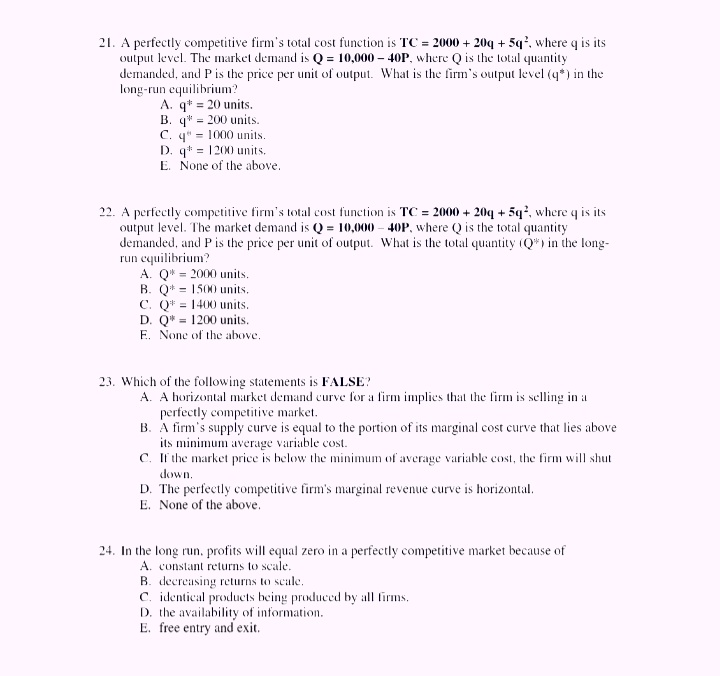

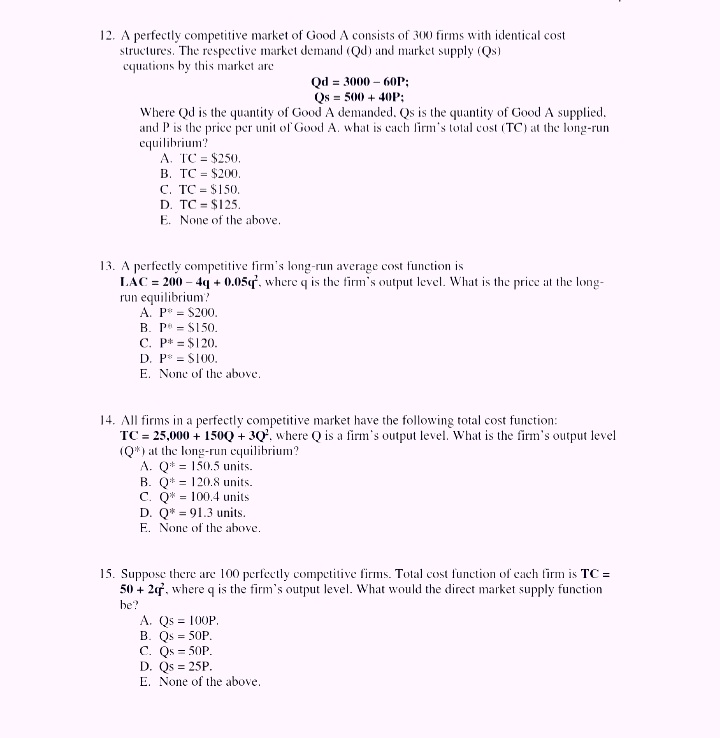

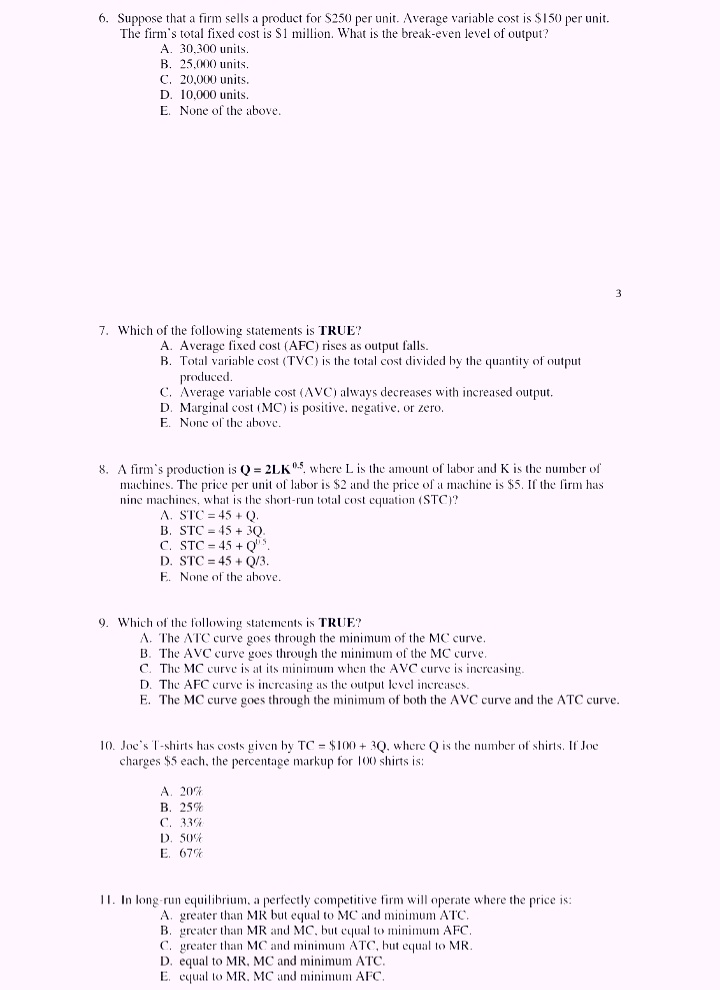

25. A firm in monopolistic market faces the following demand and total cost equations for its product as follows: Q) = 25 - 0.5P. TC = 144 +50 + 0.250-. What are the firm's short-run profit-maximizing output (Q*) and price (P*)? A. Q* = 20 units and P* = $10. B. Q" = 18 units and P* = $14. C. Q* = 15 units and P* = $20. D. Q* = 10 units and P* = $30. E. None of the above. 26. Consider a monopolist with a demand function q = 120 -2p and a marginal cost of $40. There is no total fixed cost. If the monopolist uses a single-price strategy, what would its producer surplus be? A. $400. B. $200. C $100. D. $50. E. None of the above. 27. Suppose that for each firm in the perfectly competitive market for potatoes, a firm's long-run average cost is minimized at 50. I when ten units of potatoes are grown. The market demand for potatoes is Q = 200/P. where Q is the total quantity, and P is the price per unit of potatoes. How many firms (N$) are in the long-run equilibrium? A. N* = 500. B. N* = 400. C. N* = 200. D. N* = 100. E. None of the above. 28. When firms in monopolistic competition are earning a negative profit in the short-run. firms will A. enter the industry, and demand will decrease for the original firms. B. enter the industry, and demand will increase for the original firms. C. exit the industry, and demand will increase for the firms that remain. D. exit the industry, and demand will decrease for the firms that remain. E. None of the above.21. A perfectly competitive firm's total cost function is TC = 2000 + 20q + 5q*, where q is its output level. The market demand is Q = 10,000 - 40P, where Q is the total quantity demanded, and P is the price per unit of output. What is the firm's output level (q* ) in the long-run equilibrium? A. q* = 20 units. B. q* = 200 units. C. q" = 1000 units. D. q* = 1200 units. E. None of the above. 12. A perfectly competitive firm's total cost function is TC = 2000 + 20q + 5q', where q is its output level. The market demand is Q = 10,000 - 40P. where Q is the total quantity demanded, and P is the price per unit of output. What is the total quantity (Q") in the long- run equilibrium? A. Q* = 2000 units. B. Q* = 1500 units. C. Q* = 1400 units. D. Q)* = 1200 units. E. None of the above. 23. Which of the following statements is FALSE? A. A horizontal market demand curve for a firm implies that the firm is selling in a perfectly competitive market. B. A firm's supply curve is equal to the portion of its marginal cost curve that lies above its minimum average variable cost. C. If the market price is below the minimum of average variable cost, the firm will shut down. D. The perfectly competitive firm's marginal revenue curve is horizontal. E. None of the above. 24. In the long run. profits will equal zero in a perfectly competitive market because of A. constant returns to scale. B. decreasing returns to scale. C. identical products being produced by all firms. D. the availability of information. E. free entry and exit.5 16. There are 100 perfectly competitive firms in the market. Each firm's total cost function is TC = 50 + 2q. where q is its output level. If the market price is $20. what would the market producer surplus be? A. $2000. B. $3000. C. $4000. D. $5000. E. None of the above. 17. There are 100 perfectly competitive firms in the market. Each firm's total cost function is TC = 50 + 2q'. where q is its output level. If the market price is $20, what would the firm's average variable cost at its profit-maximizing output be? A. $10. B. $15. C. $20. D. $50. E. None of the above. 18. A firm's total cost function is TC = 100 + 4q'. where q is its output level. At what price will the firm earn zero profit? A. P =$10. B. P = $20. C. P= $30. D. P = $40. E. None of the above. 19. Which of the following statements is TRUE? A. In the long run, all firms' profits equal zero in a perfectly competitive market because they produce identical products. B. If a firm cannot earn positive profit in the short run. it will shut down. C. A firm's supply curve is its entire marginal cost curve. D. If the market price in a perfectly competitive market is below the minimum of a firm's average variable cost. the firm will supply zero output. E. None of the above. 20. A perfectly competitive firm has the following total cost function: TC = q'-8q' + 30q + 5. where q is its output level. At what range of prices (P) will the firm supply zero output? A. P 40. D. Q>O

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts