Question: Please give an answer and explanation Problem 1 In this problem, you will use the following steps to show that Var(So CsdBs) = So E[C3]ds

Please give an answer and explanation

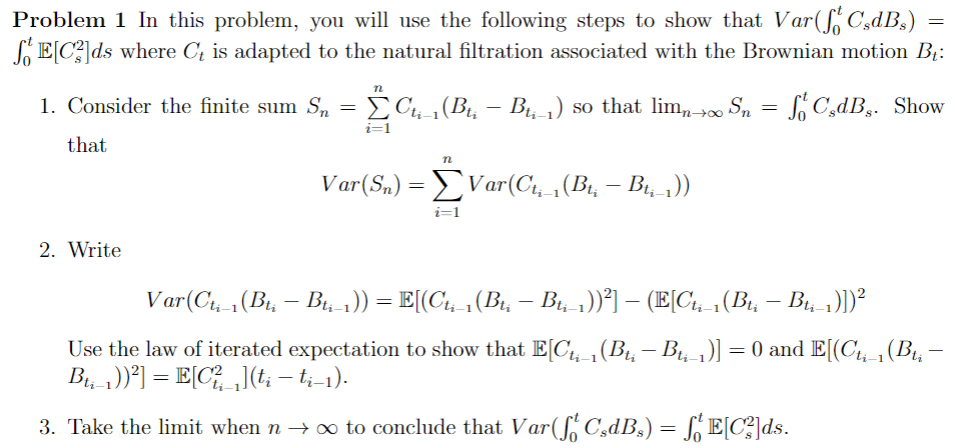

Problem 1 In this problem, you will use the following steps to show that Var(So CsdBs) = So E[C3]ds where Ct is adapted to the natural filtration associated with the Brownian motion Bt: n 1. Consider the finite sum Sn = _ Cuz, (Bu, - Bu;,) so that lim, to Sn = fo CsdBs. Show that n Var(Sn) = > Var(Ct, ,(Bu, - Bui-1)) 2. Write Var(Ct: 1 (Bu. - Bui-1)) = E[(Ct, , (Bu, - Bu-.))'] -(E[Cho, (Bu, - Bui-)])2 Use the law of iterated expectation to show that E[Ct, , (Br, - Bu;,)] = 0 and E[(Ct, , (B - Bu-1))?] = E[C2 ,1(t; - ti-1). 3. Take the limit when n - co to conclude that Var(fo CsdBs) = fo E[C3]ds

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts