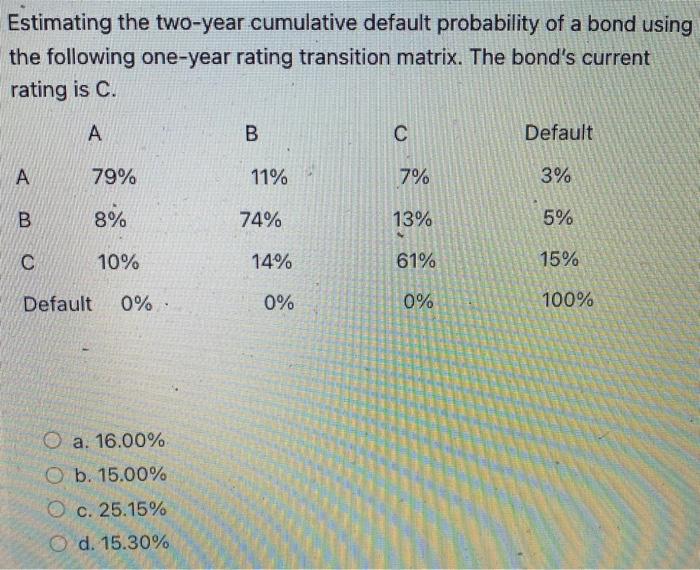

Question: please help and show steps. MC answers below question Estimating the two-year cumulative default probability of a bond using the following one-year rating transition matrix.

please help and show steps. MC answers below question

Estimating the two-year cumulative default probability of a bond using the following one-year rating transition matrix. The bond's current rating is C. a. 16.00% b. 15.00% c. 25.15% d. 15.30%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock