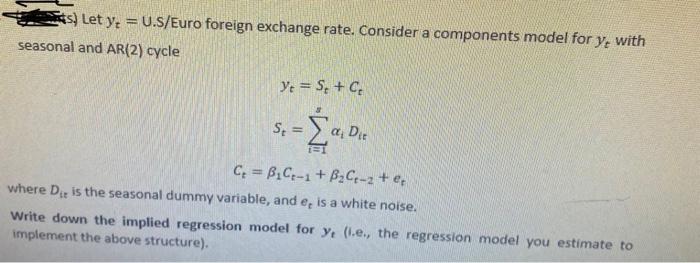

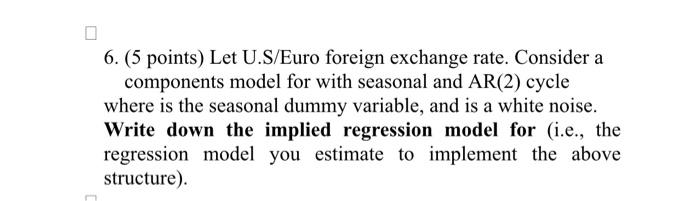

Question: please help asap. I will upvote AS) Let y: =U.S/Euro foreign exchange rate. Consider a components model for y, with seasonal and AR(2) cycle y

AS) Let y: =U.S/Euro foreign exchange rate. Consider a components model for y, with seasonal and AR(2) cycle y = S. + S = a, Die C = B.C:-1 + B2C-2+er where Dir is the seasonal dummy variable, and er is a white noise. Write down the implied regression model for y (.e., the regression model you estimate to implement the above structure), D 6. (5 points) Let U.S/Euro foreign exchange rate. Consider a components model for with seasonal and AR(2) cycle where is the seasonal dummy variable, and is a white noise. Write down the implied regression model for (i.e., the regression model you estimate to implement the above structure) AS) Let y: =U.S/Euro foreign exchange rate. Consider a components model for y, with seasonal and AR(2) cycle y = S. + S = a, Die C = B.C:-1 + B2C-2+er where Dir is the seasonal dummy variable, and er is a white noise. Write down the implied regression model for y (.e., the regression model you estimate to implement the above structure), D 6. (5 points) Let U.S/Euro foreign exchange rate. Consider a components model for with seasonal and AR(2) cycle where is the seasonal dummy variable, and is a white noise. Write down the implied regression model for (i.e., the regression model you estimate to implement the above structure)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts