Question: Please help Consider the multivariate AR(1) process X, = (At1, At2, At3, At4 ) defined as follows Xt = QXt-1+Zt, Zt ~ WN(0, E) a

Please help

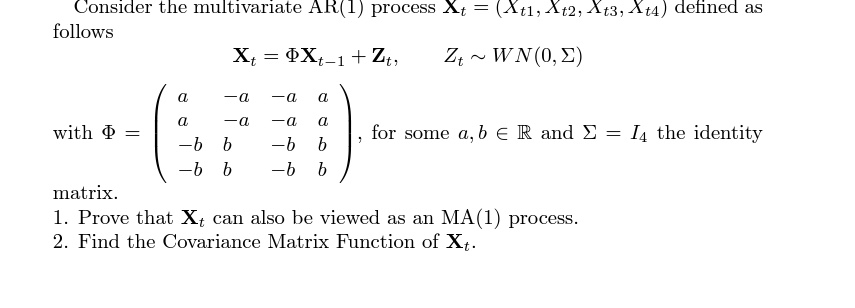

Consider the multivariate AR(1) process X, = (At1, At2, At3, At4 ) defined as follows Xt = QXt-1+Zt, Zt ~ WN(0, E) a - a - a a with & - Q - a b b -b for some a, b E R and E = 14 the identity -b b -b b matrix. 1. Prove that Xt can also be viewed as an MA(1) process. 2. Find the Covariance Matrix Function of Xt

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock