Question: please help!!!!!! FIN 623 Semester Project Option 2: Written Portfolio Asset Allocation Review and Risk Management Strategy Your task: Prepare a written report recommending an

please help!!!!!!

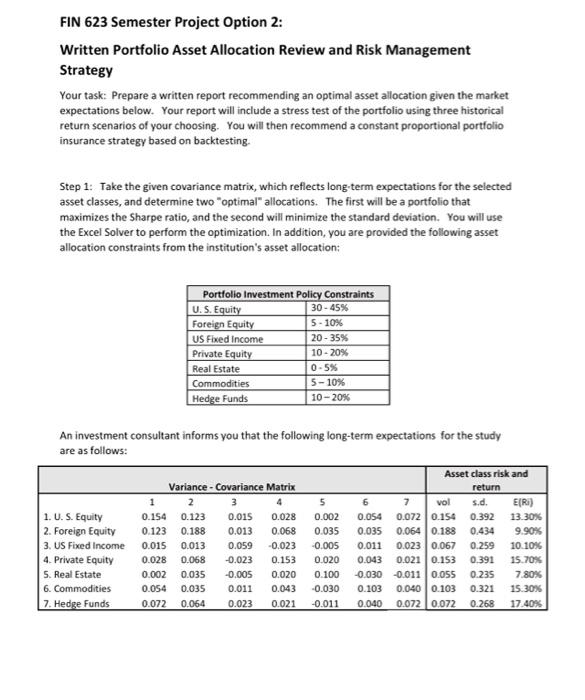

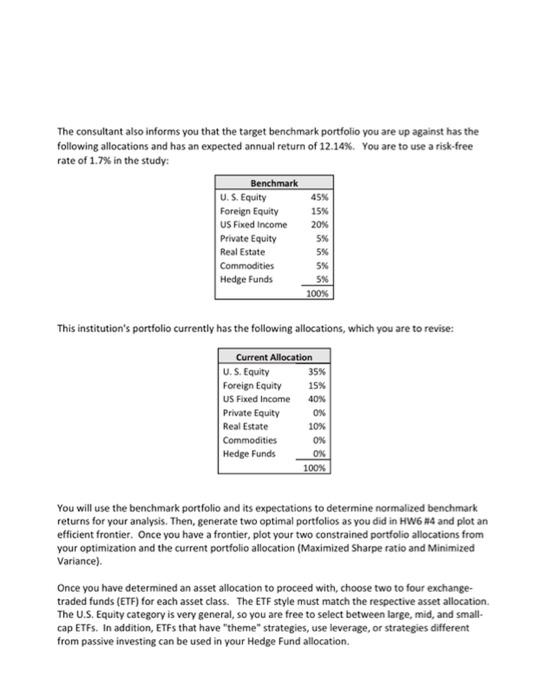

FIN 623 Semester Project Option 2: Written Portfolio Asset Allocation Review and Risk Management Strategy Your task: Prepare a written report recommending an optimal asset allocation given the market expectations below. Your report will include a stress test of the portfolio using three historical return scenarios of your choosing. You will then recommend a constant proportional portfolio insurance strategy based on backtesting. Step 1: Take the given covariance matrix, which reflects long-term expectations for the selected asset classes, and determine two optimal" allocations. The first will be a portfolio that maximizes the Sharpe ratio, and the second will minimize the standard deviation. You will use the Excel Solver to perform the optimization. In addition, you are provided the following asset allocation constraints from the institution's asset allocation: Portfolio Investment Policy Constraints U.S. Equity 30-45% Foreign Equity 5 - 10% US Fixed Income 20 - 35% Private Equity 10 - 20% Real Estate 0-5% Commodities 5-10% Hedge Funds 10-20% An investment consultant informs you that the following long-term expectations for the study are as follows: Asset class risk and Variance - Covariance Matrix return 1 2 3 4 5 6 7 vol s.d. E[R) 1. U.S. Equity 0.154 0.123 0.015 0.028 0.002 0.054 0.072 0.154 0.392 13.30% 2. Foreign Equity 0.123 0.188 0.013 0.068 0.035 0.035 0.064 0.188 0.434 9.90% 3. US Fixed Income 0.015 0.013 0.059 -0.023 -0.005 0.011 0.023 0.067 0.259 10.10% 4. Private Equity 0.028 0.068 -0.023 0.153 0.020 0.043 0.021 0.153 0.391 15.70% 5. Real Estate 0.002 0.035 -0.005 0.020 0.100 -0.030 -0.0110.055 0.235 7.80% 6. Commodities 0.054 0.035 0.011 0.043 -0.030 0.103 0.040 0.103 0.321 15.30% 7. Hedge Funds 0.072 0.064 0.023 0.021 -0.011 0.040 0.072 0.072 0.268 17.40% The consultant also inform you that the target benchmark portfolio you are up against has the following allocations and has an expected annual return of 12.14%. You are to use a risk-free rate of 1.7% in the study: Benchmark U.S. Equity Foreign Equity US Fixed Income 20% Private Equity 5% Real Estate Commodities Hedge Funds 5% 100% 45% 15% 5% 5% This institution's portfolio currently has the following allocations, which you are to revise: Current Allocation U.S. Equity 35% Foreign Equity 15% US Fixed Income 40% Private Equity 0% Real Estate 10% Commodities OX Hedge Funds OX 100% You will use the benchmark portfolio and its expectations to determine normalized benchmark returns for your analysis. Then, generate two optimal portfolios as you did in HW6 H4 and plot an efficient frontier. Once you have a frontier, plot your two constrained portfolio allocations from your optimization and the current portfolio allocation (Maximized Sharpe ratio and Minimized Variance). Once you have determined an asset allocation to proceed with, choose two to four exchange- traded funds (ETF) for each asset class. The ETF style must match the respective asset allocation. The U.S. Equity category is very general, so you are free to select between large, mid, and small- cap ETFs. In addition, ETFs that have "theme" strategies, use leverage, or strategies different from passive investing can be used in your Hedge Fund allocation. Determine the percent of the portfolio that will be invested in each ETF. You are free to choose weightings per ETF within the asset class. However, the total asset class weighting must match your recommended allocation. Report your portfolio allocation percentage by ETF and asset class. Step 2: Now that you have determined an optimal risky portfolio (consisting of ETFs), you will backtest a constant proportional portfolio insurance strategy (CPP). Gather three one-year periods of ETF returns (from any period) for all the ETFs in your portfolio. Try to pick three periods that reflect a down market, rising market, and volatile market. For example, one period should cover the pandemic crisis covering January 2020 through May 2020. Once you have return streams for each scenario, use your ETF %weights to simulate how your portfolio would perform during each period under three strategies on a daily basis: 1. 100% invested in your portfolio (Buy and Hold). 2. A 50/50 constant mix between your portfolio and the 10-year treasury. 3. A CPPI strategy which starts with a 50% exposure to your optimal portfolio and 50% in the 10-year treasury, 80% floor, and a 2.5 multiplier. You are to determine a trading threshold based on your testing (For simplicity, you may use a constant 1.7% annual return fr the 10-year treasury reserve asset). Comment on each strategy across your three scenarios. What do you observe regarding the return, volatility, and drawdowns? 4. Suggest an improvement to the model that might resolve any problem you see in the analysis. This may be altering the reserve asset or any modification of the CPPI trading decision you see fit. Test your model. The written report must: Be approximately 10 - 15 pages. Reference page at the end using a generally accepted citation system for any documents and data sources Be your work. Your report must have the following sections: Introduction on what your report is ("Asset allocation study") Summary of results/recommendation This section of your paper will summarize key facts about your recommended asset allocation, past performance under the three managed risk strategies. Analysis of Asset Allocations This section should be about two/three pages long. First, list the descriptions of each ETF in the respective asset classes. (i.e., #number of stocks, institution managing the ETF, and any fact you feel relevant). A reader should have a general overview of what each ETF does after reading this section. Portfolio Optimization This section of the paper concerns the asset allocation optimization process. First, you should show benchmark adjust returns, var-covariance matrix, and the efficient frontier. Then, discuss how your portfolio is superior to the existing. Results of the stress test and managed risk strategies Discuss the results of testing the performance of your portfolio against the three scenarios you gathered. Test the 100% buy and hold, 50/50 buy and hold, and CPPI strategy. Report expected returns, standard deviations, maximum drawdowns, min/max portfolio values, and Sharpe Ratio. Discuss findings and parameters for the CPPI strategy. Be sure to show price graphs for your three scenarios. Modification of the Model Compare and discuss the performance of your modification. Appendix Technical details of your worksheet. Any more detailed information that a reader might want to see Grading: 15% Presentation, overall appearance, and effort. 25% Implementation of the portfolio optimization procedure. 40% Stress tests of the portfolio and alternative managed risk strategies. 20% Your write-up and discussion of findings, gratuitous use of graphs and tables to tell a story. FIN 623 Semester Project Option 2: Written Portfolio Asset Allocation Review and Risk Management Strategy Your task: Prepare a written report recommending an optimal asset allocation given the market expectations below. Your report will include a stress test of the portfolio using three historical return scenarios of your choosing. You will then recommend a constant proportional portfolio insurance strategy based on backtesting. Step 1: Take the given covariance matrix, which reflects long-term expectations for the selected asset classes, and determine two optimal" allocations. The first will be a portfolio that maximizes the Sharpe ratio, and the second will minimize the standard deviation. You will use the Excel Solver to perform the optimization. In addition, you are provided the following asset allocation constraints from the institution's asset allocation: Portfolio Investment Policy Constraints U.S. Equity 30-45% Foreign Equity 5 - 10% US Fixed Income 20 - 35% Private Equity 10 - 20% Real Estate 0-5% Commodities 5-10% Hedge Funds 10-20% An investment consultant informs you that the following long-term expectations for the study are as follows: Asset class risk and Variance - Covariance Matrix return 1 2 3 4 5 6 7 vol s.d. E[R) 1. U.S. Equity 0.154 0.123 0.015 0.028 0.002 0.054 0.072 0.154 0.392 13.30% 2. Foreign Equity 0.123 0.188 0.013 0.068 0.035 0.035 0.064 0.188 0.434 9.90% 3. US Fixed Income 0.015 0.013 0.059 -0.023 -0.005 0.011 0.023 0.067 0.259 10.10% 4. Private Equity 0.028 0.068 -0.023 0.153 0.020 0.043 0.021 0.153 0.391 15.70% 5. Real Estate 0.002 0.035 -0.005 0.020 0.100 -0.030 -0.0110.055 0.235 7.80% 6. Commodities 0.054 0.035 0.011 0.043 -0.030 0.103 0.040 0.103 0.321 15.30% 7. Hedge Funds 0.072 0.064 0.023 0.021 -0.011 0.040 0.072 0.072 0.268 17.40% The consultant also inform you that the target benchmark portfolio you are up against has the following allocations and has an expected annual return of 12.14%. You are to use a risk-free rate of 1.7% in the study: Benchmark U.S. Equity Foreign Equity US Fixed Income 20% Private Equity 5% Real Estate Commodities Hedge Funds 5% 100% 45% 15% 5% 5% This institution's portfolio currently has the following allocations, which you are to revise: Current Allocation U.S. Equity 35% Foreign Equity 15% US Fixed Income 40% Private Equity 0% Real Estate 10% Commodities OX Hedge Funds OX 100% You will use the benchmark portfolio and its expectations to determine normalized benchmark returns for your analysis. Then, generate two optimal portfolios as you did in HW6 H4 and plot an efficient frontier. Once you have a frontier, plot your two constrained portfolio allocations from your optimization and the current portfolio allocation (Maximized Sharpe ratio and Minimized Variance). Once you have determined an asset allocation to proceed with, choose two to four exchange- traded funds (ETF) for each asset class. The ETF style must match the respective asset allocation. The U.S. Equity category is very general, so you are free to select between large, mid, and small- cap ETFs. In addition, ETFs that have "theme" strategies, use leverage, or strategies different from passive investing can be used in your Hedge Fund allocation. Determine the percent of the portfolio that will be invested in each ETF. You are free to choose weightings per ETF within the asset class. However, the total asset class weighting must match your recommended allocation. Report your portfolio allocation percentage by ETF and asset class. Step 2: Now that you have determined an optimal risky portfolio (consisting of ETFs), you will backtest a constant proportional portfolio insurance strategy (CPP). Gather three one-year periods of ETF returns (from any period) for all the ETFs in your portfolio. Try to pick three periods that reflect a down market, rising market, and volatile market. For example, one period should cover the pandemic crisis covering January 2020 through May 2020. Once you have return streams for each scenario, use your ETF %weights to simulate how your portfolio would perform during each period under three strategies on a daily basis: 1. 100% invested in your portfolio (Buy and Hold). 2. A 50/50 constant mix between your portfolio and the 10-year treasury. 3. A CPPI strategy which starts with a 50% exposure to your optimal portfolio and 50% in the 10-year treasury, 80% floor, and a 2.5 multiplier. You are to determine a trading threshold based on your testing (For simplicity, you may use a constant 1.7% annual return fr the 10-year treasury reserve asset). Comment on each strategy across your three scenarios. What do you observe regarding the return, volatility, and drawdowns? 4. Suggest an improvement to the model that might resolve any problem you see in the analysis. This may be altering the reserve asset or any modification of the CPPI trading decision you see fit. Test your model. The written report must: Be approximately 10 - 15 pages. Reference page at the end using a generally accepted citation system for any documents and data sources Be your work. Your report must have the following sections: Introduction on what your report is ("Asset allocation study") Summary of results/recommendation This section of your paper will summarize key facts about your recommended asset allocation, past performance under the three managed risk strategies. Analysis of Asset Allocations This section should be about two/three pages long. First, list the descriptions of each ETF in the respective asset classes. (i.e., #number of stocks, institution managing the ETF, and any fact you feel relevant). A reader should have a general overview of what each ETF does after reading this section. Portfolio Optimization This section of the paper concerns the asset allocation optimization process. First, you should show benchmark adjust returns, var-covariance matrix, and the efficient frontier. Then, discuss how your portfolio is superior to the existing. Results of the stress test and managed risk strategies Discuss the results of testing the performance of your portfolio against the three scenarios you gathered. Test the 100% buy and hold, 50/50 buy and hold, and CPPI strategy. Report expected returns, standard deviations, maximum drawdowns, min/max portfolio values, and Sharpe Ratio. Discuss findings and parameters for the CPPI strategy. Be sure to show price graphs for your three scenarios. Modification of the Model Compare and discuss the performance of your modification. Appendix Technical details of your worksheet. Any more detailed information that a reader might want to see Grading: 15% Presentation, overall appearance, and effort. 25% Implementation of the portfolio optimization procedure. 40% Stress tests of the portfolio and alternative managed risk strategies. 20% Your write-up and discussion of findings, gratuitous use of graphs and tables to tell a story Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock