Question: please help, I need it as as possible, and please answer those questions 2 and 3. and please show your work. Thank you very much.

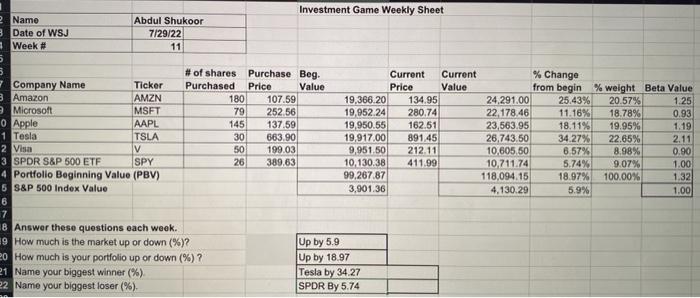

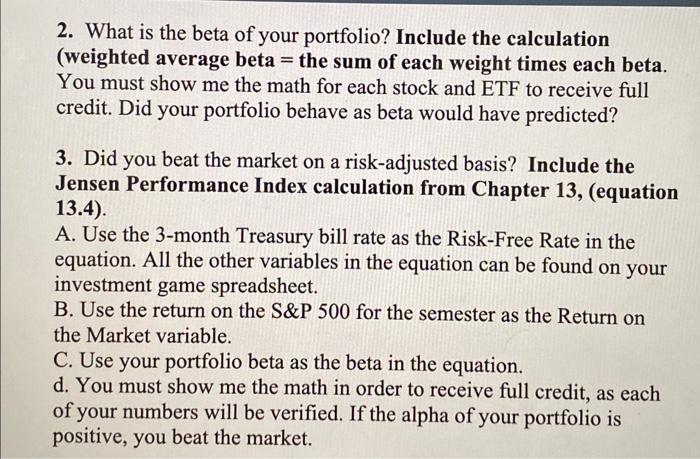

Investment Game Weekly Sheet 2. What is the beta of your portfolio? Include the calculation (weighted average beta = the sum of each weight times each beta. You must show me the math for each stock and ETF to receive full credit. Did your portfolio behave as beta would have predicted? 3. Did you beat the market on a risk-adjusted basis? Include the Jensen Performance Index calculation from Chapter 13, (equation 13.4). A. Use the 3-month Treasury bill rate as the Risk-Free Rate in the equation. All the other variables in the equation can be found on your investment game spreadsheet. B. Use the return on the S\&P 500 for the semester as the Return on the Market variable. C. Use your portfolio beta as the beta in the equation. d. You must show me the math in order to receive full credit, as each of your numbers will be verified. If the alpha of your portfolio is Investment Game Weekly Sheet 2. What is the beta of your portfolio? Include the calculation (weighted average beta = the sum of each weight times each beta. You must show me the math for each stock and ETF to receive full credit. Did your portfolio behave as beta would have predicted? 3. Did you beat the market on a risk-adjusted basis? Include the Jensen Performance Index calculation from Chapter 13, (equation 13.4). A. Use the 3-month Treasury bill rate as the Risk-Free Rate in the equation. All the other variables in the equation can be found on your investment game spreadsheet. B. Use the return on the S\&P 500 for the semester as the Return on the Market variable. C. Use your portfolio beta as the beta in the equation. d. You must show me the math in order to receive full credit, as each of your numbers will be verified. If the alpha of your portfolio is

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts