Question: PLEASE HELP, ILL UPVOTE YOUR ANSWER ASAP. THANK YOU Question 3 1 pts Based on the following information, and assuming the risk-free rate is 1.2%...

PLEASE HELP, ILL UPVOTE YOUR ANSWER ASAP. THANK YOU

PLEASE HELP, ILL UPVOTE YOUR ANSWER ASAP. THANK YOU

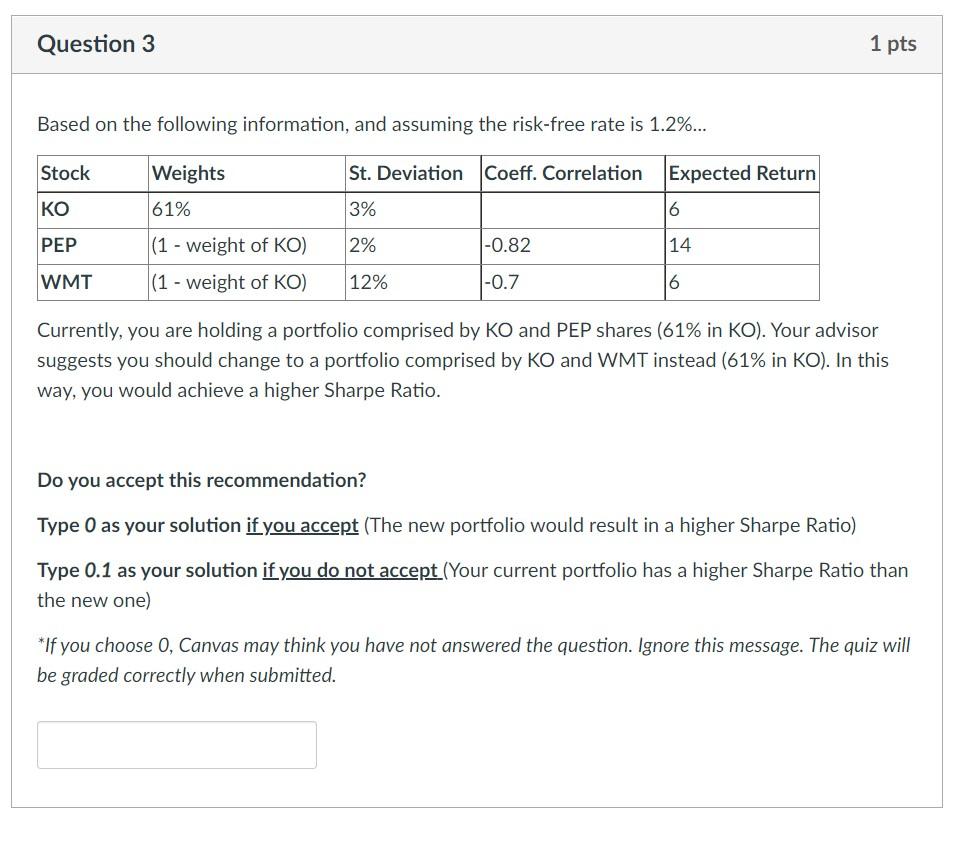

Question 3 1 pts Based on the following information, and assuming the risk-free rate is 1.2%... Stock St. Deviation Coeff. Correlation Expected Return Weights 61% KO 3% 6 PEP 2% -0.82 14 (1 - weight of KO) (1 - weight of KO) WMT 12% |-0.7 6 Currently, you are holding a portfolio comprised by KO and PEP shares (61% in KO). Your advisor suggests you should change to a portfolio comprised by KO and WMT instead (61% in KO). In this way, you would achieve a higher Sharpe Ratio. Do you accept this recommendation? Type 0 as your solution if you accept (The new portfolio would result in a higher Sharpe Ratio) Type 0.1 as your solution if you do not accept (Your current portfolio has a higher Sharpe Ratio than the new one) *If you choose 0, Canvas may think you have not answered the question. Ignore this message. The quiz will be graded correctly when submitted

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts