Question: please help me and please explain the process. Assume you have been hired by a hypothetical client, XYZ Corporation, to prepare its Form 1120, U.S.

please help me and please explain the process.

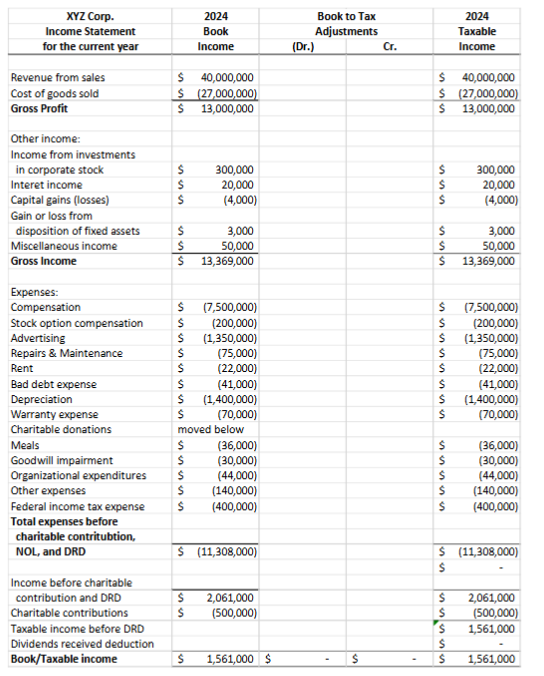

Assume you have been hired by a hypothetical client, XYZ Corporation, to prepare its Form 1120, U.S. Corporation Income Tax Return, for the 2024 tax year. Requirements: Part 1: On McGraw-Hill's Connect, complete Problem #65 from Ch05 of our text, parts (a), (b), (c), and (e). For your convenience, the information provided in the problem also appears below and on the following pages: XYZ is a calendar-year corporation that began business on January 1, 2024. For the year, it reported the following information in its current year audited income statement. Notes with important tax information are provided below. a. Reconcile book income to taxable income and identify each book-tax difference as temporary or permanent. b. Compute XYZ's income tax liability. c. Complete XYZ's Schedule M-1. e. Determine the quarters for which XYZ is subject to penalties for the underpayment of estimated taxes (see assumptions and estimated tax information on the next page). Notes: 1. XYZ owns 30 percent of the outstanding Hobble Corp. (HC) stock. HC reported $1,000,000 of income for the year. XYZ accounted for its investment in HC under the equity method, and it recorded its pro rata share of HC's earnings for the year. HC also distributed a $200,000 dividend to XYZ. For tax purposes, XYZ reports the actual dividend received as income, not the pro rata share of HC's earnings. 2. Of the $20,000 interest income, $5,000 was from a City of Seattle bond, $7,000 was from a Tacoma City bond, $6,000 was from a fully taxable corporate bond, and the remaining $2,000 was from a money market account. 3. This gain is from equipment that XYZ purchased in February and sold in December (i.e., it does not qualify as 1231 gain). 4. This includes total officer compensation of $2,500,000 (no one officer received more than $1,000,000 compensation). 5. This amount is the portion of incentive stock option compensation that was expensed during the year (recipients are officers). 6. XYZ actually wrote off $27,000 of its accounts receivable as uncollectible. 7. Tax depreciation was $1,900,000. 8. In the current year, XYZ did not make any actual payments on warranties it provided to customers. 9. XYZ made $500,000 of cash contributions to charities during the year. 10. On July 1 of this year, XYZ acquired the assets of another business. In the process, it acquired $300,000 of goodwill. At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of organizational expenditures allowed for tax purposes. 12. The other expenses do not contain any items with book-tax differences. 13. This is an estimated tax provision (federal tax expense) for the year. Assume that XYZ is not subject to state income taxes.

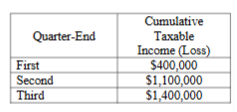

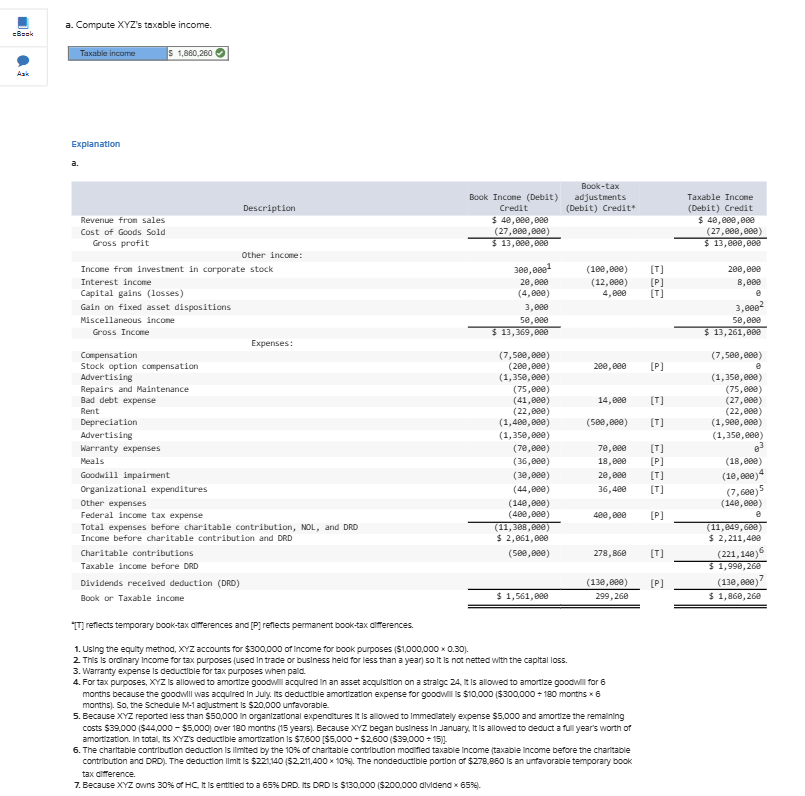

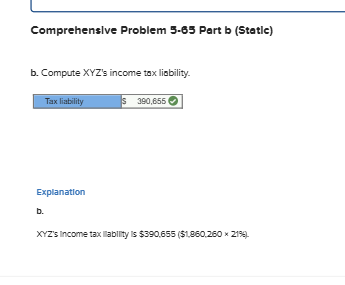

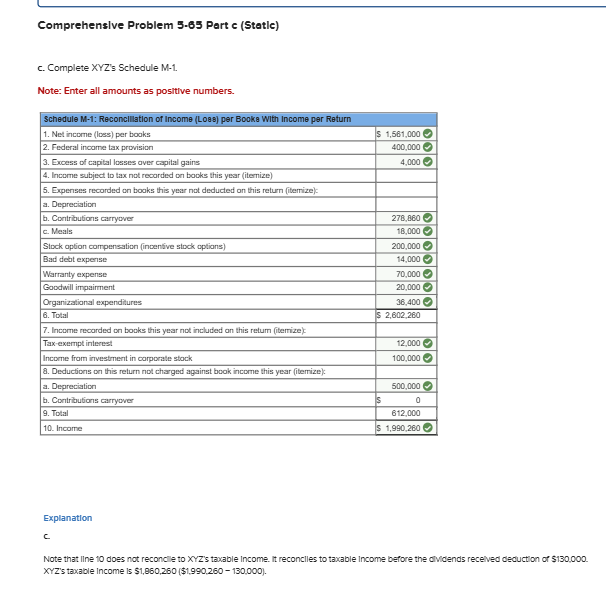

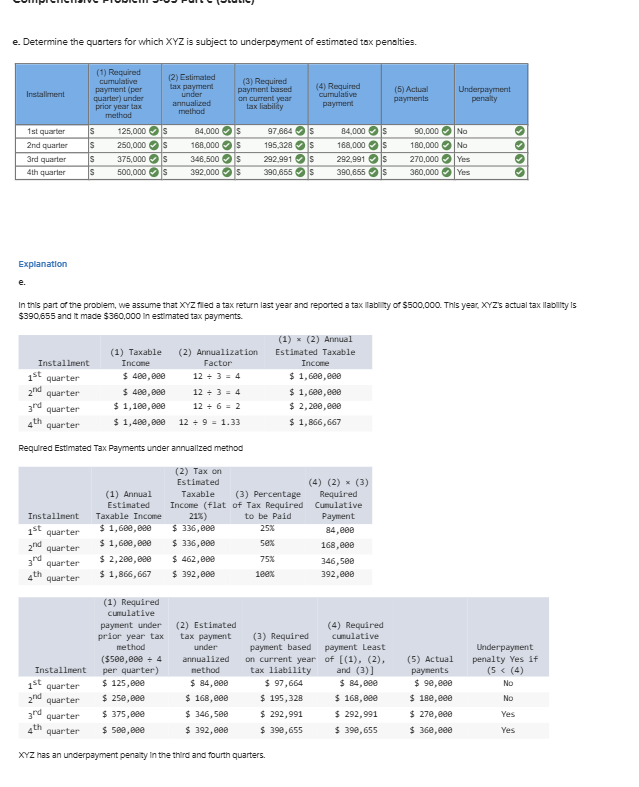

\fXYZ Corp. Income Statement for the current year Revenue from sales Cost of goods sold Gross Profit Other income: Income from investments in corporate stock Interet income Capital gains (losses) Gain or loss from disposition of fined assets Miscellaneous income Gross Income Expenses: Compensation Stock option compensation Advertising Repairs & Maintenance Rent Bad debt expense Depreciation Warranty expense Charitable donations Meals Goodwill impairment Organizational expenditures Other expenses Federal income tax expense Total expenses before charitable contritubtion, NOL, and DRD Income before charitable contribution and DRD Charitable contributions Taxable income before DRD Dividends received deduction Book/Taxable income 2024 Book to Tax 2024 Book Adjustments Taxable Income (Dr.) cr. Income $ 40,000,000 $ 40,000,000 $ (27,000,000) $ (27,000,000) $ 13,000,000 $ 13,000,000 $ 300,000 $ 300,000: $ 20,000 s 20,000: 3 (4,000) 5 (4,000) $ 3,000 $s 3,000 $ 50,000 $ 50,000: $ 13,369,000 $ 13,369,000 (7,500,000) (7,500,000) $ (200,000) $ (200,000) $ (1,350,000) $ (1,350,000) $ (75,000) (75,000) $ (22,000) $ (22,000) $ (41,000) $ (41,000) $ (1,400,000) $ (1,400,000) $ (70,000) $ (70,000) moved below $ (36,000) $ (36,000) $ (30,000) $ (30,000) $ (44,000) $ (44,000) $ (140,000) $ (140,000) S (400,000) $ (400,000) $ (11,308,000) $ (11,308,000) s - $ = 2,061,000 $ 2,061,000 S$ (500,000) s (500,000) "S 1,561,000 s - $ 1,561,000 $ $ 1,561,000 a. Compute XYZ's taxable income. =Back Taxable income $ 1,880,260 Explanation Book-tax Book Income (Debit) adjustments Taxable Income Description Credit [Debit) Credit* Debit) Credit Revenue from sales $ 40, 090, 0BE $ 40, 009, 080 Cost of Goods Sold (27, 080, 680) (27 ,800, 609) Gross profit $ 13, 020, 680 $ 13,060,069 Other income: Income from investment in corporate stock 300, 060 (109, 090) [T] 206, 060 Interest income 20, 090 12, egg) [P ] 8,90 Capital gains (losses) (4, 090) 4,090 Gain on fixed asset dispositions 3,090 3,090- Miscellaneous income 50, 080 50,090 Gross Income $ 13, 369, 680 $ 13, 261, 069 Expenses: Compensation (7,500, 600) (7,500, 060) Stock option compensation (209, 090) 280, 030 [P] e Advertising (1, 350, 080) (1,350,809) Repairs and Maintenance (75,090) (75,060) Bad debt expense (41, 020) 14,080 [T] (27, 060) Rent (22,Bee) (22, 609) Depreciation (1,409,020) (580,080) [T] (1,900, 809) Advertising 1,350,020) (1,350,800) Warranty expenses 70,680 [T] Meals (36,090) 18, 090 [P ] (18,069) Goodwill impairment (30,090) 20, 080 [T] (10, 890) 4 Organizational expenditures (44, 090) 36,480 [T] (7,680)5 Other expenses 140,020) (140,009) Federal income tax expense (409, 020) 480, 036 [P ] Total expenses before charitable contribution, NOL, and DRD (11,308, 620) (11,849, 609) Income before charitable contribution and DRD $ 2, 061, 090 $ 2, 211, 409 Charitable contributions (509, 090) 278, 860 [T] (221,140)6 Taxable income before DRD $ 1, 990, 260 Dividends received deduction (DRD) (130, 680) [P ] (130, 890) Book or Taxable income $ 1,561, 080 299,260 $ 1, 860, 260 "IT reflects temporary book-tax differences and [P] reflects permanent book-tax differences. 1. Using the equity method, XYZ accounts for $300.000 of Income for book purposes ($1,000,000 x 0.30]. 2. This Is ordinary Income for tax purposes (used In trade or business held for less than a year) so It Is not netted with the capital loss. 3. Warranty expense Is deductible for tax purposes when paid. 4. For tax purposes, XYZ Is allowed to amortize goodw acquired in an asset acquisition on a stralge 24, It Is allowed to amortize goodwill for 6 months because the goodwill was acquired In July. Its deductible amortization expense for goodwill is $10,000 ($300,000 + 180 months x 6 months). So, the Schedule M-1 adjustment is $20,000 unfavorable. 5. Because XYZ reported less than $50,000 in organizational expenditures it Is allowed to Immediately expense $5,000 and amortize the remaining costs $39.000 ($44,000 - $5.000) over 180 months (15 years). Because XYZ began business In January, It Is allowed to deduct a full year's worth of amortization. In total, Its XYZ's deductible amortization Is $7.600 [$5,000 + $2.600 ($39.000 = 15)] 6. The charitable contribution deduction Is limited by the 10%% of charitable contribution modified taxable Income (taxable Income before the charitable contribution and DRD). The deduction limit Is $221,140 ($2,211,400 * 1098). The nondeductible portion of $278,860 Is an unfavorable temporary book tax difference. . Because XYZ owns 30% of HC, It Is entitled to a 65%% DRD. Its DRD Is $130.000 ($200.000 dividend x 6539).Comprehensive Problem 5-65 Part b (Statle) b. Compute XYZ's income tax liability Tax liability S 380,655) Explanation b. XYZ's Income tax "ability Is $390.655 ($1.860.260 x 219%)Comprehensive Problem 5-65 Part c (Statle) C. Complete XYZ's Schedule M-1. Note: Enter all amounts as positive numbers. Schedule M-1: Reconciliation of Income (Loss] per Booke With Income per Return 1. Net income (loss) per books $ 1,561,000 2. Federal income tax provision 400,000 3. Excess of capital losses over capital gains 4,000 4. Income subject to tax not recorded on books this year (itemize) 5. Expenses recorded on books this year not deducted on this return (itemize): a. Depreciation b. Contributions carryover 278 860 c. Meal: 18,000 Stock option compensation (incentive stock options) 200,000 Bad debt expense 14,000 Warranty expense 70,000 Goodwill impairment 20,000 Organizational expenditures 36.400 6. Total $ 2,602 260 7. Income recorded on books this year not included on this return (itemize) Tax-exempt interest 12,000 Income from investment in corporate stock 100,000 8. Deductions on this return not charged against book income this year (itemize) a. Depreciation 500,000 b. Contributions carryover 9. Total 812 000 10. Income $ 1,990 260 Explanation C Note that line 10 does not reconcile to XYZ's taxable Income. It reconciles to taxable Income before the dividends received deduction of $130.000. XYZ's taxable Income Is $1,860,260 ($1.990.260 - 130.000).e. Determine the quarters for which XYZ is subject to underpayment of estimated tox penalties. 1) Required cumulative (2) Estimated payment (per tax payment (3) Required payment based (4) Required Installment (5) Actual Underpayment quarter) under under on current year cumulative prior year lax annualized payment payments penalty method method tax liability 1st quarter 125,000\\S 34 000 3 97 684 5 84,000 5 40,000 No 2nd quarter 250,000 168.000 195,328 5 188,000 180,000 No ard quarter 375,000 348 500 292.991 292,991 270,000 Yes 4th quarter 500,000 392,000 390 655 5 390.855 5 380,000 Yes Explanation e. In this part of the problem, we assume that XYZ filed a tax return last year and reported a tax liability of $500,000. This year, XYZ's actual tax llability Is $390,655 and It made $360,000 In estimated tax payments. (1) = (2) Annual (1) Taxable (2) Armualization Estimated Taxable Installment Income Factor Income 152 quarter $ 480,090 12 + 3 = 4 $ 1, 600,800 grid quarter $ 483,030 12 + 3 = 4 $ 1, 620,800 quarter $ 1,160,090 12 + 6 = 2 $ 2,206,090 quarter $ 1, 403, 080 12 + 9 = 1.31 $ 1, 866, 667 Required Estimated Tax Payments under annualized method (2) Tax on Estimated (4) (2) = (3) (1) Annual Taxable (3) Percentage Required Estimated Income (flat of Tax Required Cumulative Installment Taxable Income 21%) to be Paid Payment 12 quarter $ 1, 603, 630 $ 336,068 25% 84, 200 2nidd quarter $ 1, 603, 030 $ 336, 909 Sex 168,090 and quarter $ 2,260, 680 $ 462, 060 75% 346,508 ath quarter $ 1, 866, 667 $ 392, 909 392,809 (1) Required cumulative payment under (2) Estimated (4) Required prior year tax tax payment (3) Required cumulative method under payment based payment Least Underpayment ($500, 080 + 4 annualized on current year of [(1), (2), (5) Actual penalty Yes if Installment per quarter) method tax liability and (3)] payments (5 * (4) ist quarter $ 125,080 $ 84,060 $ 97, 664 $ 84,090 $ 90,800 No and quarter $ 250,090 $ 168, 090 $ 195,328 $ 168, 080 $ 180,806 NO quarter $ 375,090 $ 346,506 $ 292,991 $ 292, 991 $ 279,800 Yes quarter $ 509,080 $ 392, 090 $ 390, 655 $ 390, 655 $ 360,880 Yes XYZ has an underpayment penalty in the third and fourth quarters

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!