Question: please help me answer the questions. Question 1 (10 points) An Italian company, New Century Corp, enters into a 2-year interest rate swap with Northern

please help me answer the questions.

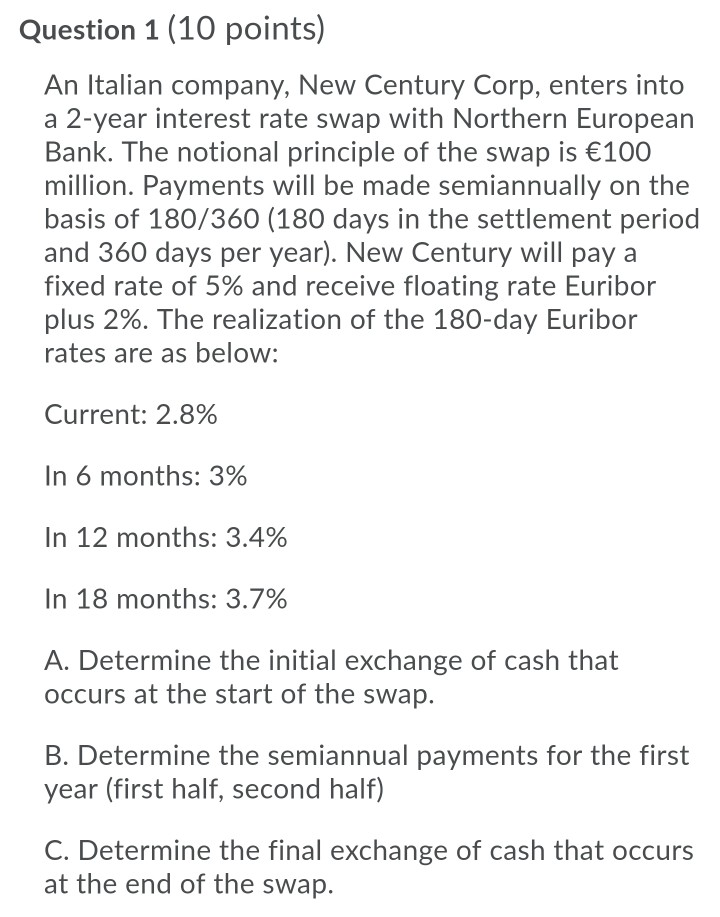

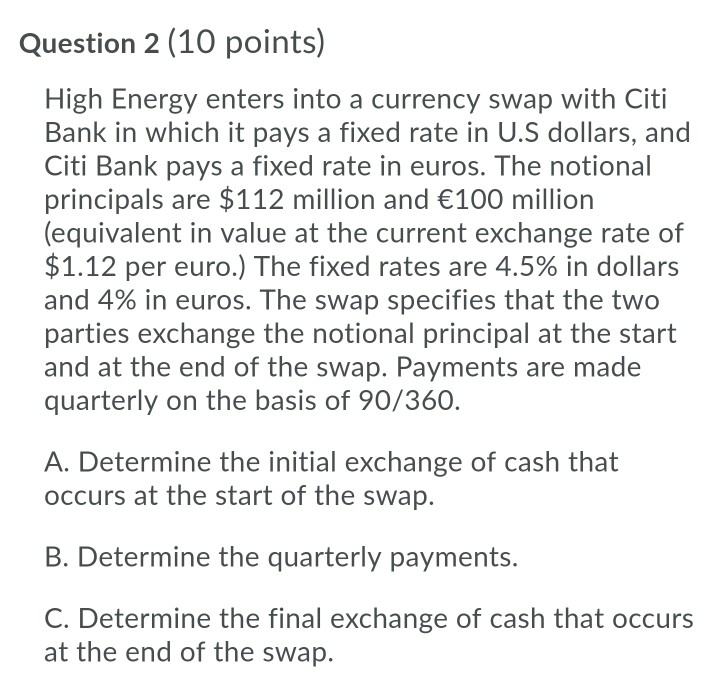

Question 1 (10 points) An Italian company, New Century Corp, enters into a 2-year interest rate swap with Northern European Bank. The notional principle of the swap is 100 million. Payments will be made semiannually on the basis of 180/360 (180 days in the settlement period and 360 days per year). New Century will pay a fixed rate of 5% and receive floating rate Euribor plus 2%. The realization of the 180-day Euribor rates are as below: Current: 2.8% In 6 months: 3% In 12 months: 3.4% In 18 months: 3.7% A. Determine the initial exchange of cash that occurs at the start of the swap. B. Determine the semiannual payments for the first year (first half, second half) C. Determine the final exchange of cash that occurs at the end of the swap. Question 2 (10 points) High Energy enters into a currency swap with Citi Bank in which it pays a fixed rate in U.S dollars, and Citi Bank pays a fixed rate in euros. The notional principals are $112 million and 100 million (equivalent in value at the current exchange rate of $1.12 per euro.) The fixed rates are 4.5% in dollars and 4% in euros. The swap specifies that the two parties exchange the notional principal at the start and at the end of the swap. Payments are made quarterly on the basis of 90/360. A. Determine the initial exchange of cash that occurs at the start of the swap. B. Determine the quarterly payments. C. Determine the final exchange of cash that occurs at the end of the swap

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts