Question: Please help me answer this finance question. Need back as soon as possible. Thank you Ignoring the negligible interest you might earn on T-Bills over

Please help me answer this finance question. Need back as soon as possible. Thank you

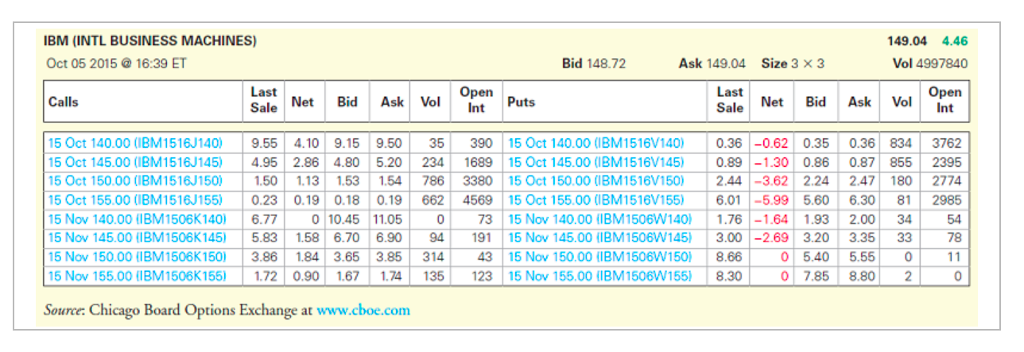

Ignoring the negligible interest you might earn on T-Bills over the remaining few days' life Consider the October 2015 IBM call and put options in the table, of the options, show that there is no arbitrage opportunity using put-call parity for the options with a $140 strike price. Specifically: a. What is your profitloss if you buy a call and T-Bills, and sell IBM stock and a put option? b. What is your profit/loss if you buy IBM stock and a put option, and sell a call and T-Bills? c. Explain why your answers to (a) and (b) are not both zero. d. Do the same calculation for the October options with a strike price of $150. What do you find? How can you explain this? a. What is your profitloss if you buy a call and T-Bills, and sell IBM stock and a put option? (Select the best choice below.) 0 A. O B. ( C. O D. Buy call and T-Bills, sell stock and put--$9.50 + $140.00-$148.72 + $0.35--$17.87 Sell call and T-Bills, buy stock and put = + $9.15-$140.00 + $149.04-$0.36-$17.83 Sell call and T-Bills, buy stock and put = + $9.15 + $140.00-$14904-$0.36--S025 Buy call and T-Bills, sell stock and put=-$9.50-$140.00 + $148.72 + SO.35--$0.43 b. What is your profitloss if you buy IBM stock and a put option, and sell a call and T-Bills? (Select the best choice below.) A. Sell call and T-Bills, buv stock and outs + $9.15-$140.00 + $149.04-$0.36-$17.83 Click to select your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts