Question: PLEASE HELP ME! Carlos Altuve is a manager-of-managers at an investment company that use4s quantitative models extensively. Altuve seeks to construct a multi-manager portfolio using

PLEASE HELP ME!

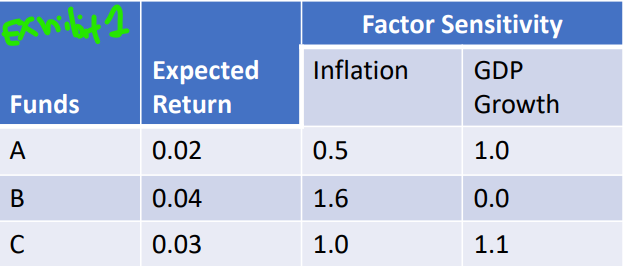

Carlos Altuve is a manager-of-managers at an investment company that use4s quantitative models extensively. Altuve seeks to construct a multi-manager portfolio using some of the funds managers by portfolio managers within the firm. Maya Zapata is assisting him. Using Arbitrage Pricing theory (APT) to evaluate strategies and managering risk for three funds. Using a two-factor Model Zapata now estimates the three funds sensitivity to inflation and GDP growth. The information is presented in Exhibit 1. Zapata assumes a zero value for the error terms when working with the selected two factor model. Altuve Asks Zapata to calculate the return for Portfolio AC, composed of a 60 percent allocation to Fund A and 40 percent allocation to Fund C, using the surprises in in inflation and GDP growth in Exhibit 2.

\begin{tabular}{|l|l|l|l|} \hline Funds & & \multicolumn{2}{|c|}{ Factor Sensitivity } \\ \hline Funds & \begin{tabular}{l} Expected \\ Return \end{tabular} & Inflation & \begin{tabular}{l} GDP \\ Growth \end{tabular} \\ \hline A & 0.02 & 0.5 & 1.0 \\ \hline B & 0.04 & 1.6 & 0.0 \\ \hline C & 0.03 & 1.0 & 1.1 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|} \hline Factor Exhibi & Forecast & Actual Value \\ \hline Inflation & 2.0% & 2.2% \\ \hline GDP Growth & 1.5% & 1.0% \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts