Question: Please help me (& DO NOT USE AI PLEASE). I have been trying to figure this out for hours. I will thumbs up!!! A U.S.

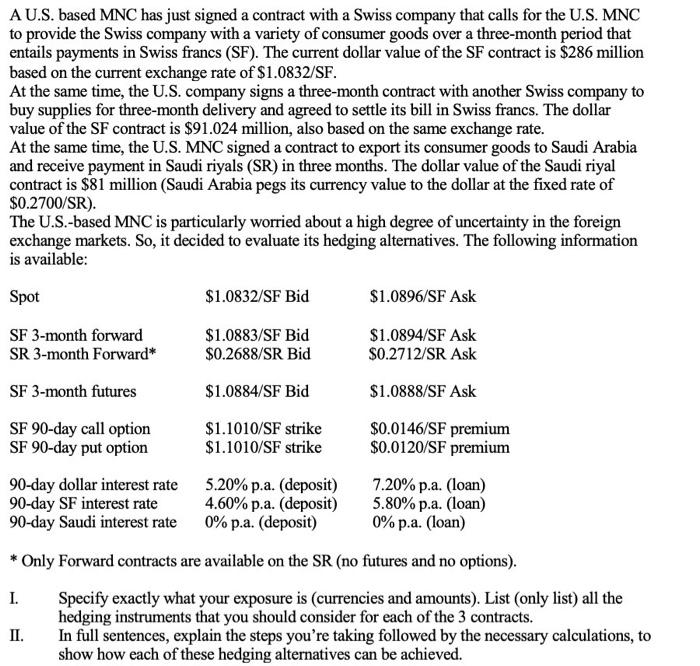

A U.S. based MNC has just signed a contract with a Swiss company that calls for the U.S. MNC to provide the Swiss company with a variety of consumer goods over a three-month period that entails payments in Swiss francs (SF). The current dollar value of the SF contract is \$286 million based on the current exchange rate of $1.0832/SF. At the same time, the U.S. company signs a three-month contract with another Swiss company to buy supplies for three-month delivery and agreed to settle its bill in Swiss francs. The dollar value of the SF contract is $91.024 million, also based on the same exchange rate. At the same time, the U.S. MNC signed a contract to export its consumer goods to Saudi Arabia and receive payment in Saudi riyals (SR) in three months. The dollar value of the Saudi riyal contract is $81 million (Saudi Arabia pegs its currency value to the dollar at the fixed rate of $0.2700/SR). The U.S.-based MNC is particularly worried about a high degree of uncertainty in the foreign exchange markets. So, it decided to evaluate its hedging alternatives. The following information is available: * Only Forward contracts are available on the SR (no futures and no options). I. Specify exactly what your exposure is (currencies and amounts). List (only list) all the hedging instruments that you should consider for each of the 3 contracts. II. In full sentences, explain the steps you're taking followed by the necessary calculations, to show how each of these hedging alternatives can be achieved

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts