Question: Please help me explain those answer. 4. You write one IBM July 120 call contract for a premium of S4. You hold the option until

Please help me explain those answer.

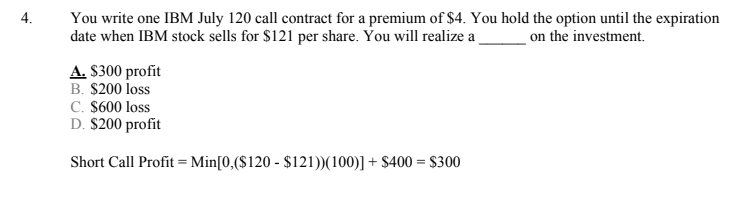

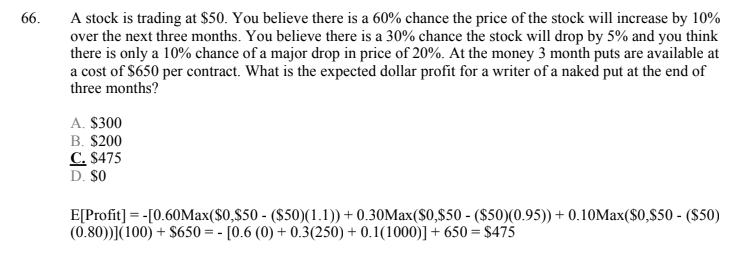

4. You write one IBM July 120 call contract for a premium of S4. You hold the option until the expiration date when IBM stock sells for $121 per share. You will realize a on the investment. A. S300 profit B. $200 loss C. $600 loss D. $200 profit Short Call Profit-Min[O, (S120 $121)100)]+ $400 $300

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock