Question: please help me for this A Friday 12:10 AM Edit Burn * Open 1. A portfolio consists of 1,000 identical and independent risks. Given that

please help me for this

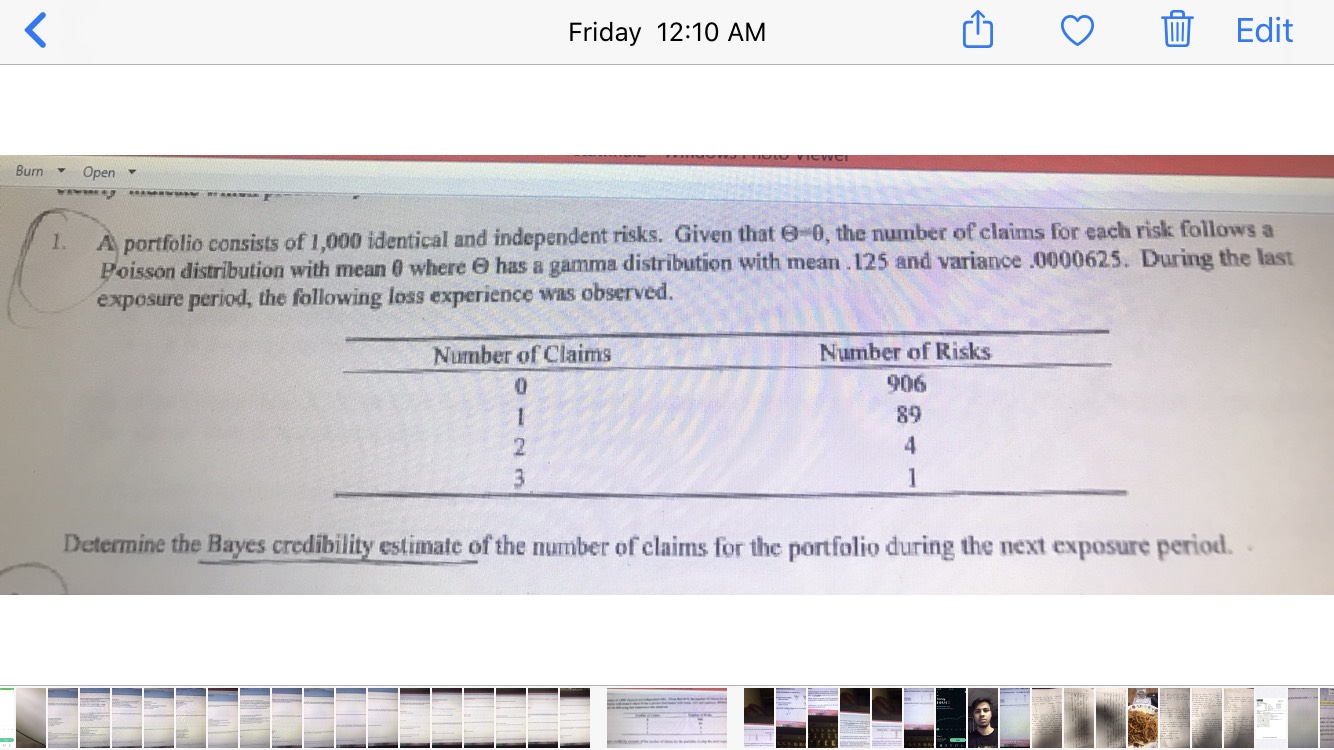

A Friday 12:10 AM Edit Burn * Open 1. A portfolio consists of 1,000 identical and independent risks. Given that 6-0, the number of claims for each risk follows a Poisson distribution with mean 0 where @ has a gamma distribution with mean . 125 and variance .0000625. During the last exposure period, the following loss experience was observed. Number of Claims Number of Risks WN - E 906 89 Determine the Bayes credibility estimate of the number of claims for the portfolio during the next exposure period

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock