Question: please help me.. i have the answer but I want you to paraphrase these answers, use your own words, I don't want to copy and

please help me.. i have the answer but I want you to paraphrase these answers, use your own words, I don't want to copy and paste please. Thank you ..

Q1. In Riyadh City Road traffic congestion is increasing day by day. As an economist how you see this problem? Suggest and explain an economists solution to this problem.

Economist have their own point of view and analyzing power to judge the efficiency of any decision . They always check the cost of taking any decision ,impact of efficiency of the decision on output and at last required profit or actual profit gain from the implementation of the decision . Now if Riyadh road congestion is increasing day by day it is not good for Riyadh economy . Due to heavy congestion Riyadh might suffer from big economical loss. A data published by economic times shows that due to traffic congestion across the different countries world loose its 2% of its GDP. It means alone traffic congestion cause loss of 2% in world GDP. Do you ever think that how traffic congestion cause loss to economy . We are going to follow multidimensional economical approach to calculate the loss caused due to traffic. These loss can be accounted in the following ways

(a ) Congestion of traffic decrease the working hours in the economy and productivity too.

( b ) Due to congestion economy is tends to spends more dollars on fuel expenses . It means due to congestion GDP expenditure on fuels may rise .

( c ) Due to heavy congestion on road , the life span of the road get decreased it means now government have to spends more on building roads

(d) Congestion cause extreme pollution. Due to high pollution economy may loose on its natural resources like effects on crop production , health infrastructure, ecological degradation and at last imbalance of eco system due to high pollution .

Solutions to mitigate the risk of heavy congestion or effect of congestion on road.

As we discussed above that economist have different perception to look after any decisions . He/she can not suggest such solutions whose implementation cost would be more as compared to benefits. So just to solve the problem of congestion we will follow balance approach which may not cause any adverse selection . To solve the problem of congestion economist have suggested following things .

(1) Proper management of traffic light system on roads. Mean we can use AI algorithm to manage the traffic lights on roads

(2) Impose heavy fine on road side parking. Due reduce such instances government can build dedicated parking areas. Which will not decrease congestion but also will be will generate revenue for the Riyadh government.

(3 ) Incorporate lane system for driving . Government should build dedicated lanes for different vehicles .

( 4) Promote green energy and green transport, it will reduce or cut fuel expenses

(5 ) Plant more and more tress along the road. It will exhaust the extra pollution and protect biodiversity degradation

(6) Government should make a call and promote the use of public transport .It is one of the best way of cost cutting on travel expenses and reduce traffic congestion

Q2. What is opportunity cost? Draw a Production Possibility curve for a country producing two goods and show with help of an example, how principle of opportunity is applied in explaining the changes in production possibilities for the country. (3 marks)

Opportunity Cost is a concept used in microeconomic theory that denotes the loss of benefit that can be enjoyed when choosing the best alternative. Most of the day-to-day decisions are based directly or indirectly on the concept of opportunity cost. It is the excess of returns on the best-foregone option over the returns on the chosen option

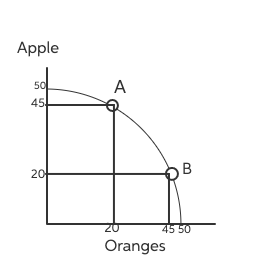

Above PPF shows combination of Oranges and Apple that can be produced by an economy.

As we can see that there are two production possibilities points A and B .

Opportunity is cost is defined as the amount of good that is sacrificed when additional amount of other is produced.

Now assume if economy is producing at point A that is 45 Apples 20 Oranges.

Now if economy want to produce 45 Oranges than production of Apple will fall to 20 this means economy has to sacrifice 25 apples (45 -20) .

The loss of production of 25 Apples is known as opportunity cost.

As a result of which economy will move to point B.

So above is an example of opportunity cost with the help of PPF consisting two goods apple and oranges.

Therefore, change in production possibilities result in opportunity cost that is some goods have to be sacrificed to produce more of other.

Q3. What is market equilibrium? Take an example of pizza (assume its price and quantity demanded) and analyse graphically, what happens to the equilibrium price and quantity when, (a) there is increase in demand and (b) there is increase in supply. (4 Marks)

Market equilibrium is a market state where the supply in the market is equal to the demand in the market. The equilibrium price is the price of a good or service when the supply of it is equal to the demand for it in the market. If a market is at equilibrium, the price will not change unless an external factor changes the supply or demand, which results in a disruption of the equilibrium.

Examples of Market Equilibrium:-

1} Flat Screen TVs:-- Imagine that you make flat screen televisions. Your flagship model is a 72-inch plasma that currently wholesales to your retailers at $2,500. Unfortunately, your warehouse has recently been filling a bit too quickly with 72-inch plasmas. This is probably because each of your three largest competitors has finally gotten around to introducing their own 72-inch televisions, which means that there are a bunch more 72-inch televisions on the market. You decide to lower your wholesale price to $2,250 and see what happens. You also decide to cut production down by 25% for the next month to clear out existing inventory.

Supply, Demand & Equilibrium

If a market is not at equilibrium, market forces tend to move it to equilibrium. Let's break this concept down.

If the market price is above the equilibrium value, there is an excess supply in the market (a surplus), which means there is more supply than demand. In this situation, sellers will tend to reduce the price of their good or service to clear their inventories. They probably will also slow down their production or stop ordering new inventory. The lower price entices more people to buy, which will reduce the supply further. This process will result in demand increasing and supply decreasing until the market price equals the equilibrium price.

If the market price is below the equilibrium value, then there is excess in demand (supply shortage). In this case, buyers will bid up the price of the good or service in order to obtain the good or service in short supply. As the price goes up, some buyers will quit trying because they don't want to, or can't, pay the higher price. Additionally, sellers, more than happy to see the demand, will start to supply more of it. Eventually, the upward pressure on price and supply will stabilize at market equilibrium.

Apple AppleStep by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts