Question: Please help me solve a, b, c and d 1. (Currency Futures and Hedging) Trident (US) wishes to manage a 800,000 account payable arising from

Please help me solve a, b, c and d

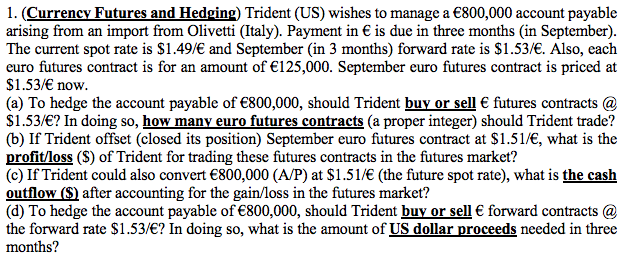

1. (Currency Futures and Hedging) Trident (US) wishes to manage a 800,000 account payable arising from an import from Olivetti (Italy). Payment in is due in three months (in September). The current spot rate is S1.49/ and September (in 3 months) forward rate is S1.53/. Also, each euro futures contract is for an amount of 125,000. September euro futures contract is priced at S1.53/ now. (a) To hedge the account payable of 800,000, should Trident buy or sell futures contracts @ $1.53/? In doing so, how many euro futures contracts (a proper integer) should Trident trade? (b) If Trident offset (closed its position) September euro futures contract at S1.51/E, what is the profitloss (S) of Trident for trading these futures contracts in the futures market? (c) If Trident could also convert 800,000 (A/P) at $1.51/ (the future spot rate), what is the cash outflow (S after accounting for the gain/loss in the futures market? (d) To hedge the account payable of 800,000, should Trident buy or sell forward contracts @ the forward rate S1.53/e? In doing so, what is the amount of US dollar proceeds needed in three months? 5 1 1 (a) Buv euro futures contracts: 6 (b) -15,000 (S; loss) (c) $1,223,000 d) Buy forward contracts: $1,224,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts