Question: Please help me solve the following problem. Thanks. Problem 8 Consider an n x p matrix X with standardized variables, a response variable y E

Please help me solve the following problem. Thanks.

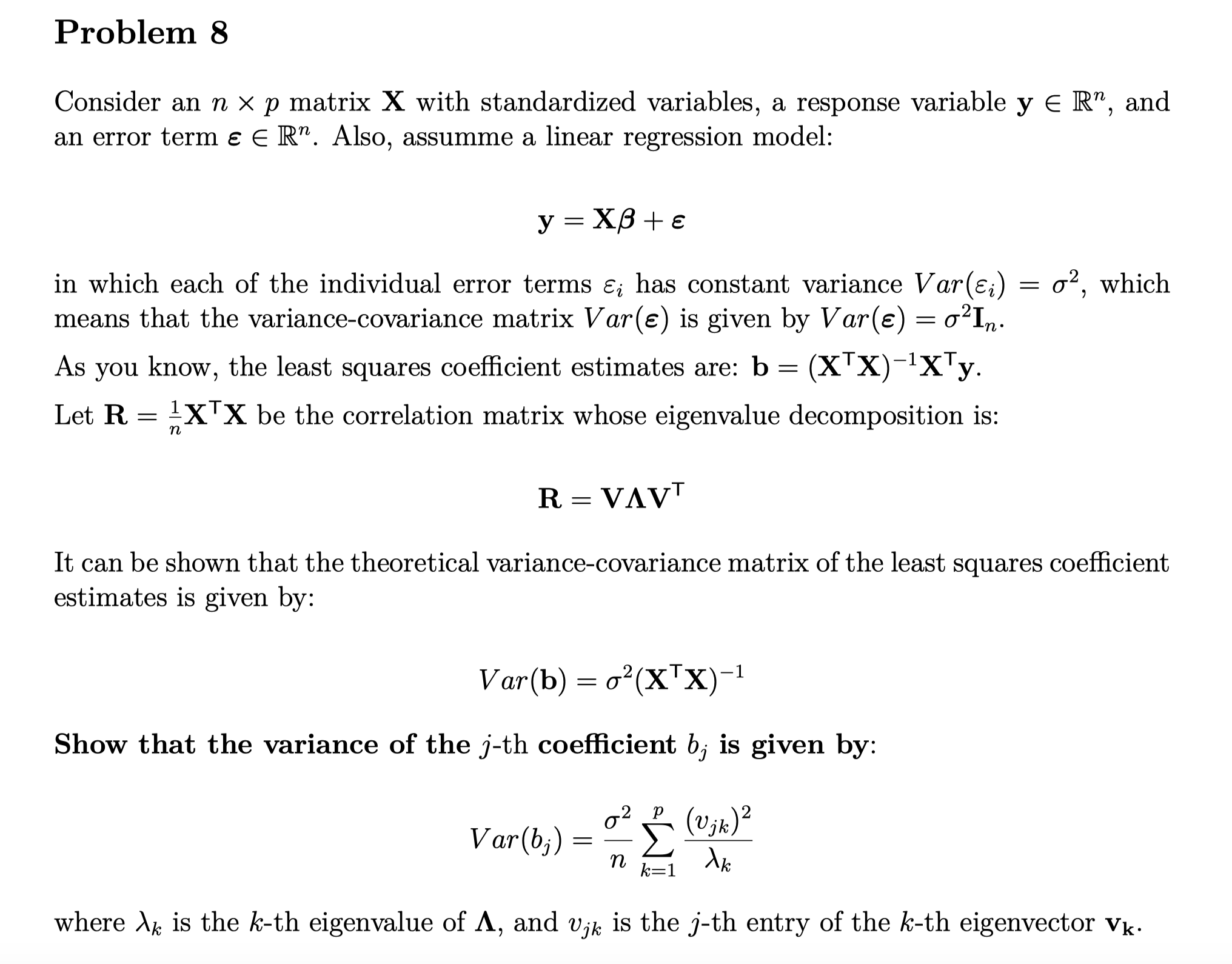

Problem 8 Consider an n x p matrix X with standardized variables, a response variable y E R", and an error term & E R". Also, assumme a linear regression model: y = XB+ in which each of the individual error terms &; has constant variance Var(Ei) = 02, which means that the variance-covariance matrix Var(E) is given by Var(E) = 02In. As you know, the least squares coefficient estimates are: b = (XTX)-iXTy. Let R = 1X X be the correlation matrix whose eigenvalue decomposition is: R = VAVT It can be shown that the theoretical variance-covariance matrix of the least squares coefficient estimates is given by: Var(b) = 02(XX)-1 Show that the variance of the j-th coefficient bj is given by: Var(b;) = 0 z 1 jk ) 2 n K= 1 where Ax is the k-th eigenvalue of A, and vik is the j-th entry of the k-th eigenvector Vk

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts