Question: please help me solve this question from part a through g. really appreciate it! Jim Campbell is founder and CEO of OpenStart, an innovative software

please help me solve this question from part a through g. really appreciate it!

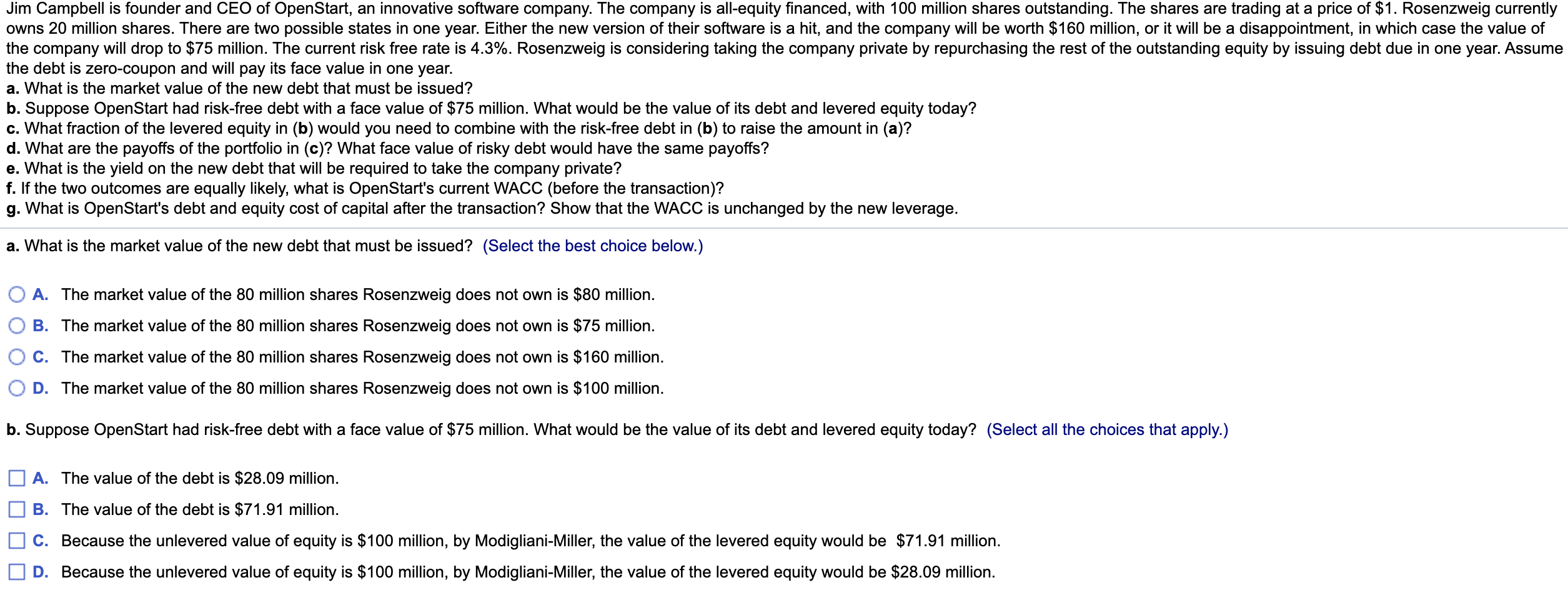

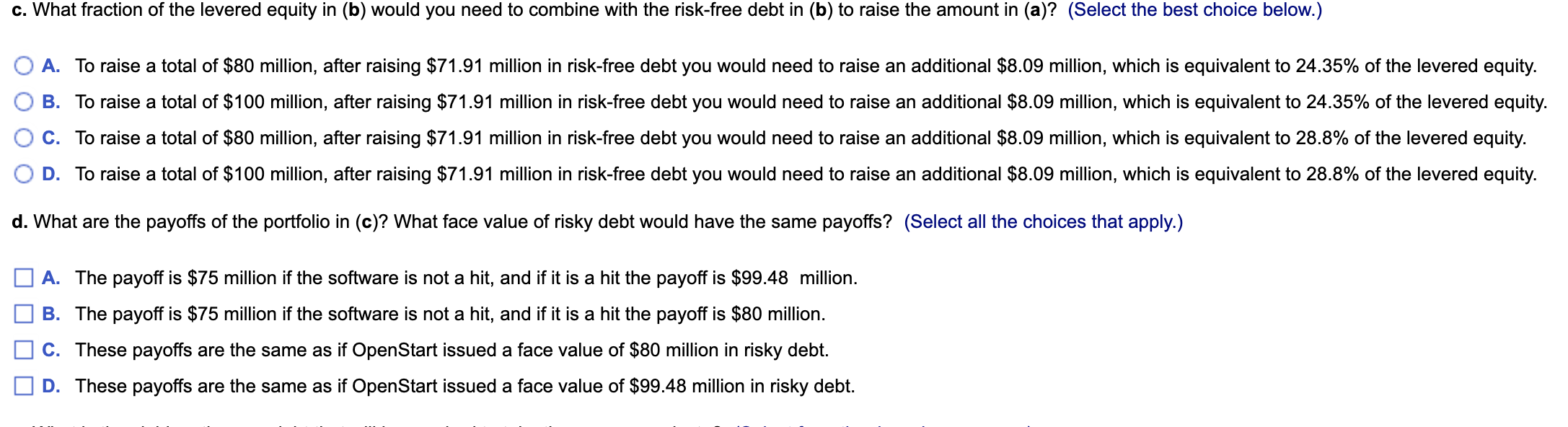

Jim Campbell is founder and CEO of OpenStart, an innovative software company. The company is all-equity financed, with 100 million shares outstanding. The shares are trading at a price of $1. Rosenzweig currently owns 20 million shares. There are two possible states in one year. Either the new version of their software is a hit, and the company will be worth $160 million, or it will be a disappointment, in which case the value of the company will drop to $75 million. The current risk free rate is 4.3%. Rosenzweig is considering taking the company private by repurchasing the rest of the outstanding equity by issuing debt due in one year. Assume the debt is zero-coupon and will pay its face value in one year. a. What is the market value of the new debt that must be issued? b. Suppose OpenStart had risk-free debt with a face value of $75 million. What would be the value of its debt and levered equity today? c. What fraction of the levered equity in (b) would you need to combine with the risk-free debt in (b) to raise the amount in (a)? d. What are the payoffs of the portfolio in (c)? What face value of risky debt would have the same payoffs? e. What is the yield on the new debt that will be required to take the company private? f. If the two outcomes are equally likely, what is OpenStart's current WACC (before the transaction)? g. What is OpenStart's debt and equity cost of capital after the transaction? Show that the WACC is unchanged by the new leverage. a. What is the market value of the new debt that must be issued? (Select the best choice below.) A. The market value of the 80 million shares Rosenzweig does not own is $80 million. B. The market value of the 80 million shares Rosenzweig does not own is $75 million. C. The market value of the 80 million shares Rosenzweig does not own is $160 million. D. The market value of the 80 million shares Rosenzweig does not own is $100 million. b. Suppose OpenStart had risk-free debt with a face value of $75 million. What would be the value of its debt and levered equity today? (Select all the choices that apply.) A. The value of the debt is $28.09 million. B. The value of the debt is $71.91 million. C. Because the unlevered value of equity is $100 million, by Modigliani-Miller, the value of the levered equity would be $71.91 million. D. Because the unlevered value of equity is $100 million, by Modigliani-Miller, the value of the levered equity would be $28.09 million. c. What fraction of the levered equity in (b) would you need to combine with the risk-free debt in (b) to raise the amount in (a)? (Select the best choice below.) A. To raise a total of $80 million, after raising $71.91 million in risk-free debt you would need to raise an additional $8.09 million, which is equivalent to 24.35% of the levered equity. B. To raise a total of $100 million, after raising $71.91 million in risk-free debt you would need to raise an additional $8.09 million, which is equivalent to 24.35% of the levered equity. C. To raise a total of $80 million, after raising $71.91 million in risk-free debt you would need to raise an additional $8.09 million, which is equivalent to 28.8% of the levered equity. D. To raise a total of $100 million, after raising $71.91 million in risk-free debt you would need to raise an additional $8.09 million, which is equivalent to 28.8% of the levered equity. d. What are the payoffs of the portfolio in (c)? What face value of risky debt would have the same payoffs? (Select all the choices that apply.) A. The payoff is $75 million if the software is not a hit, and if it is a hit the payoff is $99.48 million. B. The payoff is $75 million if the software is not a hit, and if it is a hit the payoff is $80 million. C. These payoffs are the same as if OpenStart issued a face value of $80 million in risky debt. D. These payoffs are the same as if OpenStart issued a face value of $99.48 million in risky debt. e. What is the yield on the new debt that will be required to take the company private? (Select from the drop-down menus.) With a face value of million and a market value of million, the yield is f. If the two outcomes are equally likely, what is OpenStart's current WACC (before the transaction)? (Select from the drop-down menus.) Without leverage, the return on equity is when high or when low, for an expected return of As the company is currently all equity, this is its initial WACC. g. What is OpenStart's debt and equity cost of capital after the transaction? Show that the WACC is unchanged by the new leverage. (Select from the drop-down menus.) OpenStart's debt return is in the good state, and in the bad state, for an expected return of OpenStart's remaining equity is worth million, and has a payoff of million or zero, or an expected payoff of million. This corresponds to an expected return of . The WACC is therefore just as in (f)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts