Question: Please help me to answer number 3 completely. Thanks A non-dividend-paying stock has the current price of pound 60. Each month the price rises by

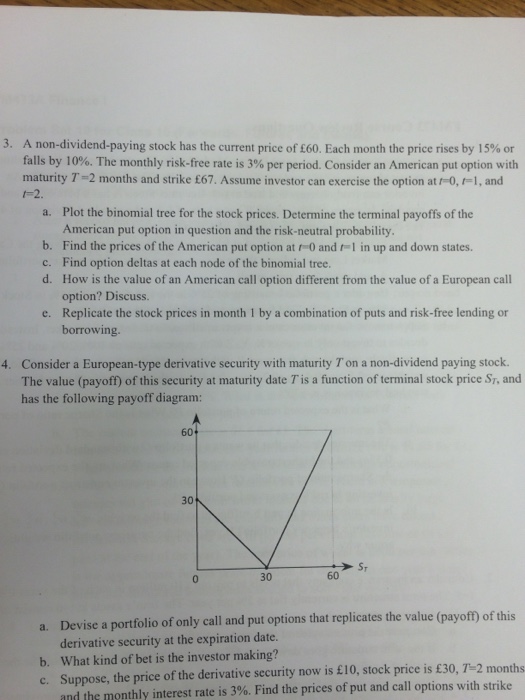

A non-dividend-paying stock has the current price of pound 60. Each month the price rises by 15% or falls by 10%. The monthly risk-free rate is 3% per period. Consider an American put option with maturity T = 2 months and strike pound 67. Assume investor can exercise the option at t=0, t=1, and t=2. Plot the binomial tree for the stock prices. Determine the terminal payoffs of the American put option in question and the risk-neutral probability. Find the prices of the American put option at t=0 and t=1 in up and down states. Find option deltas at each node of the binomial tree. How is the value of an American call option different from the value of a European call option? Discuss. Replicate the stock prices in month 1 by a combination of puts and risk-free lending or borrowing. Consider a European-type derivative security with maturity T on a non-dividend paying stock. The value (payoff) of this security at maturity date T is a function of terminal stock price S_T, and has the following payoff diagram: Devise a portfolio of only call and put options that replicates the value (payoff) of this derivative security at the expiration date. What kind of bet is the investor making? Suppose, the price of the derivative security now is pound 10, stock price is pound 30, T = 2 months and the monthly interest rate is 3%. Find the prices of put and call options with strike

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts