Question: Please help me with all steps of this practice problems. Thanks! A portfolio is created out of three risky assets with expected returns 71 =

Please help me with all steps of this practice problems. Thanks!

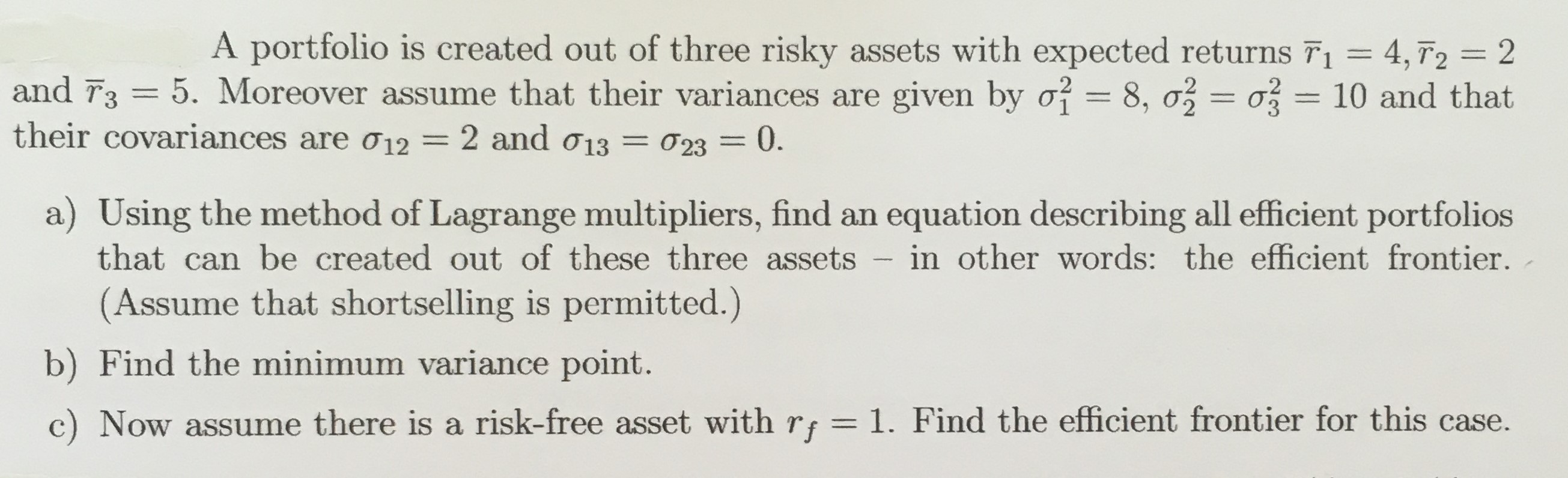

A portfolio is created out of three risky assets with expected returns 71 = 4, T2 = 2 and T3 = 5. Moreover assume that their variances are given by of = 8, 0? = 03 = 10 and that their covariances are 012 = 2 and 013 = 023 = 0. a) Using the method of Lagrange multipliers, find an equation describing all efficient portfolios that can be created out of these three assets - in other words: the efficient frontier. (Assume that shortselling is permitted.) b) Find the minimum variance point. c) Now assume there is a risk-free asset with r = 1. Find the efficient frontier for this case

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock