Question: PLEASE HELP ME WITH FOLLOWINGS : The spread between the two 10-year bonds A and C in the chart below is bps while the yield

PLEASE HELP ME WITH FOLLOWINGS :

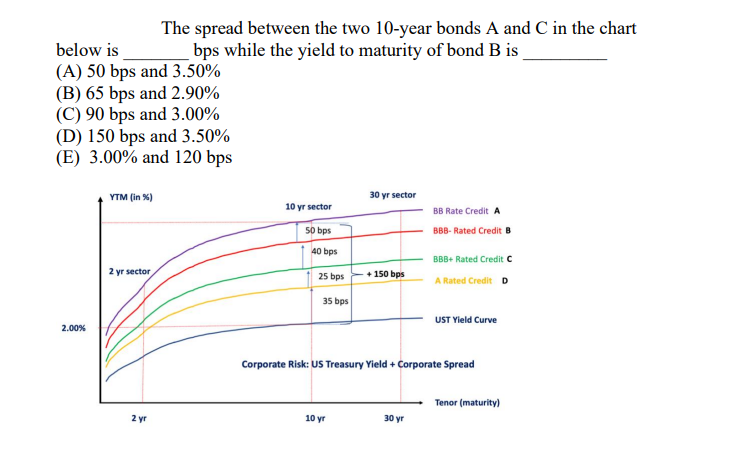

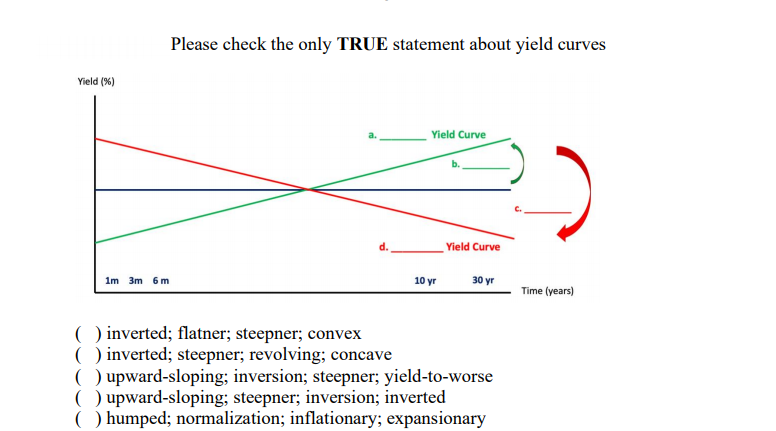

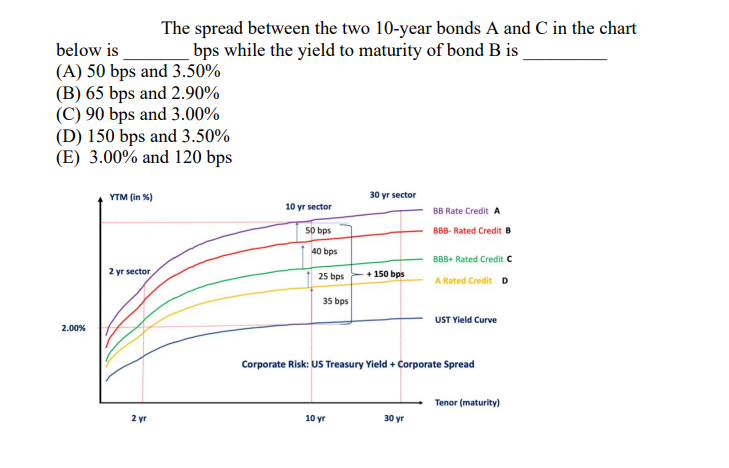

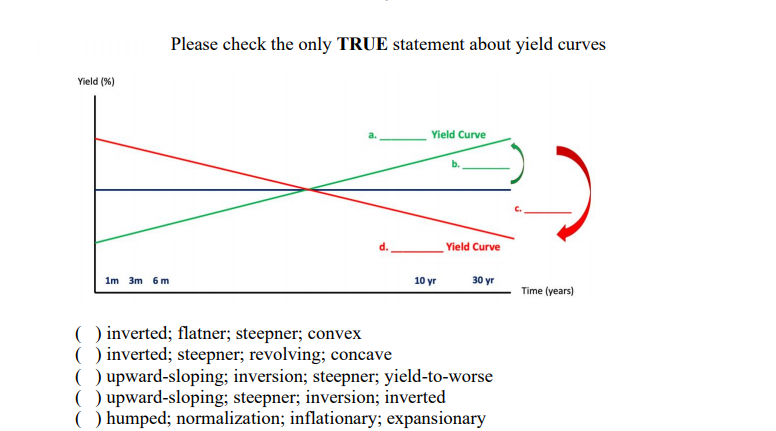

The spread between the two 10-year bonds A and C in the chart below is bps while the yield to maturity of bond B is (A) 50 bps and 3.50% (B) 65 bps and 2.90% (C) 90 bps and 3.00% (D) 150 bps and 3.50% (E) 3.00% and 120 bps YTM [in %) 30 yr sector 10 yr sector BB Rate Credit A 50 bps BBB- Rated Credit B 40 bps BBB+ Rated Credit C 2 yr sector 25 bps + 150 bps A Rated Credit D 35 bps UST Yield Curve 2.00% Corporate Risk: US Treasury Yield + Corporate Spread Tenor (maturity) 2 yr 10 yr 30 yrPlease check the only TRUE statement about yield curves Yield (%) Yield Curve b. C. d. Yield Curve 1m 3m 6m 10 yr 30 yr Time (years) ( ) inverted; flatner; steepner; convex ( ) inverted; steepner; revolving; concave ( ) upward-sloping; inversion; steepner; yield-to-worse ( ) upward-sloping; steepner; inversion; inverted ( ) humped; normalization; inflationary; expansionary

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts