Question: Please help me with the 2 questions in the attachment They are from McMaster commerce 3FB3 course Thank you! Numerical Problems (60 points) 1. (30

Please help me with the 2 questions in the attachment

They are from McMaster commerce 3FB3 course

Thank you!

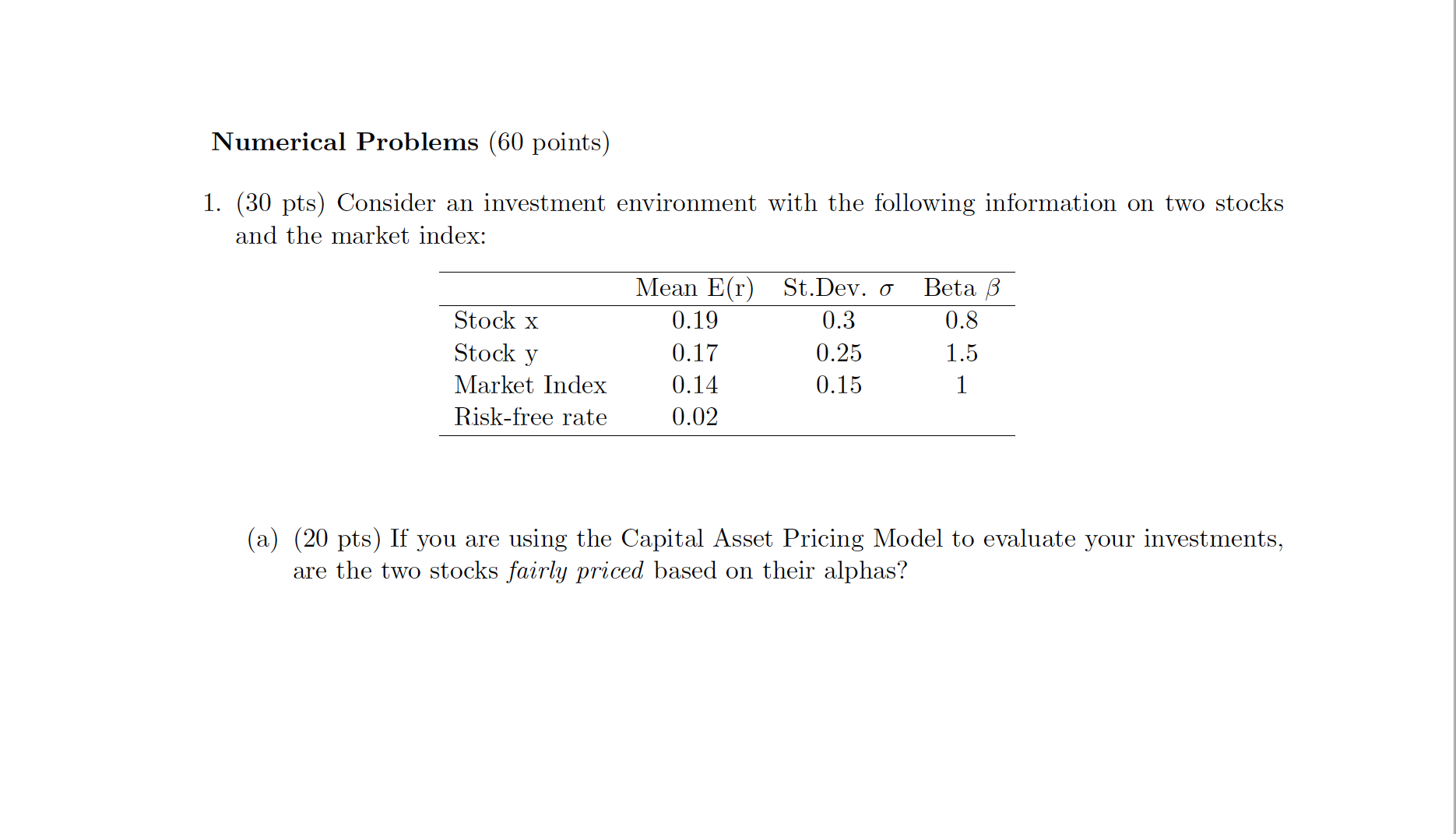

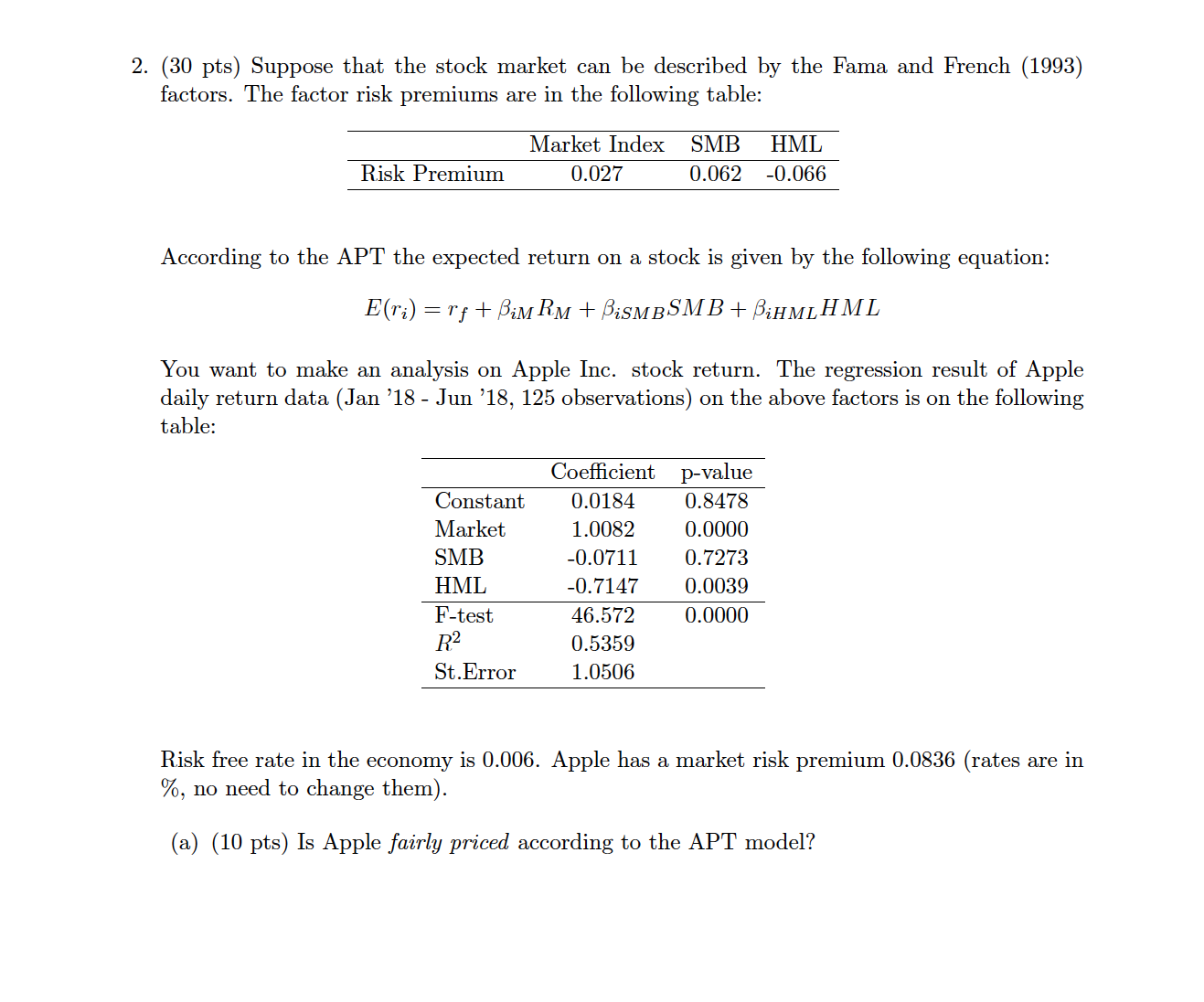

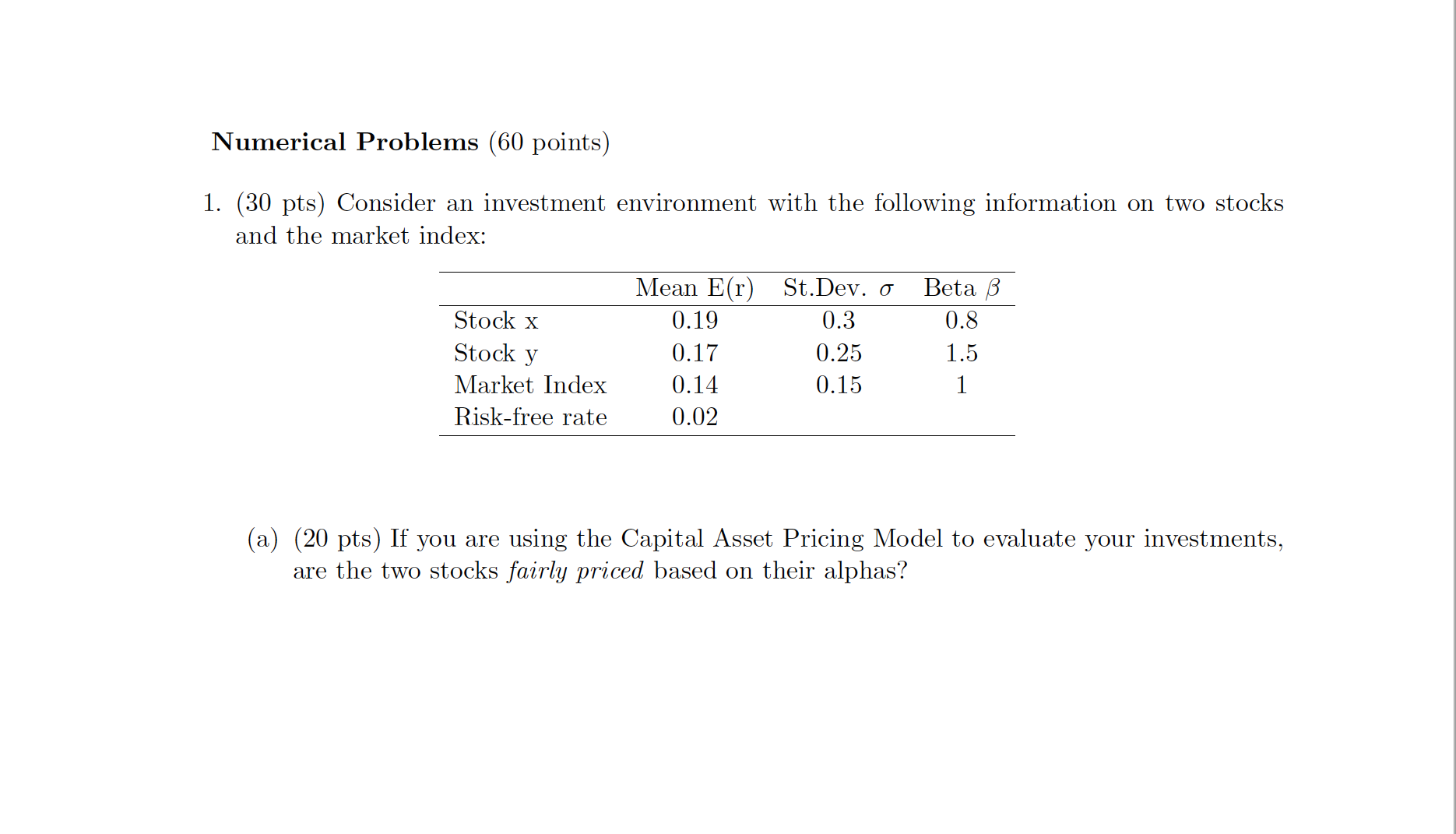

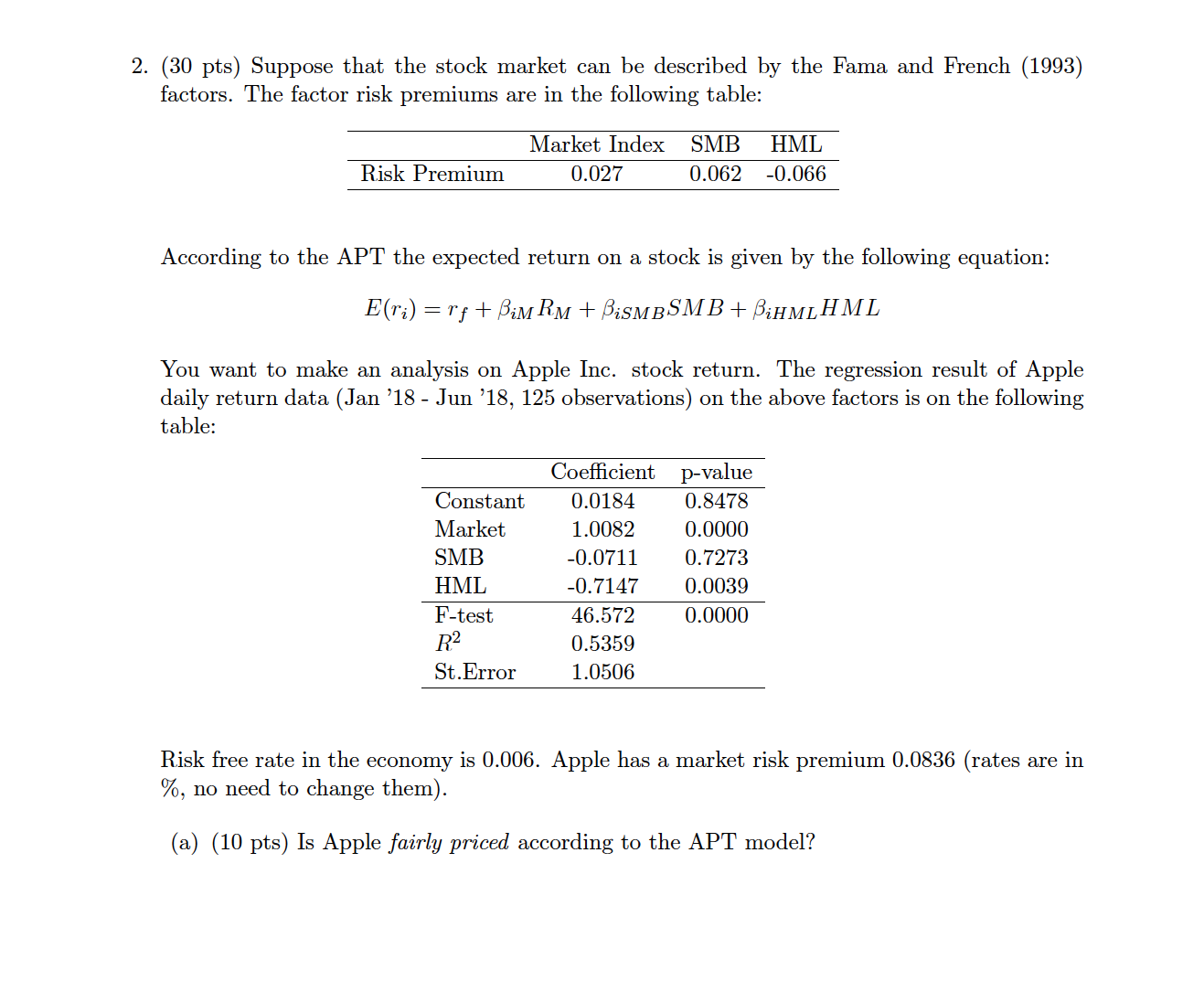

Numerical Problems (60 points) 1. (30 pts) Consider an investment environment with the following information on two stocks and the market index: Mean E(r) St.Dev. a Beta ,8 Stock x 0.19 0.3 08 Stock y 0.17 0.25 1.5 Market Index 0.14 0.15 1 Risk-free rate 0.02 (a) (20 pts) If you are using the Capital Asset Pricing Model to evaluate your investments, are the two stocks fairly priced based on their alphas? (b) (5 pts) Based on the result on (a) which of the two stocks would you buy to include in a welldiversied portfolio? (c) (5 pts) If you want to form a singlestock portfolio, based on return per risk, in which stock would you invest? 2. (30 pts) Suppose that the stock market can be described by the Fama and French (1993) factors. The factor risk premiums are in the following table: Market Index SMB HML Risk Premium 0.027 0.062 -0.066 According to the APT the expected return on a stock is given by the following equation: EUR) : T; + Bill/[RM + iSMBSMB + iHMLHML You want to make an analysis on Apple Inc. stock return. The regression result of Apple daily return data (J an '18 - Jun '18, 125 observations) on the above factors is on the following table: Coeicient pvalue Constant 0.0184 0.8478 Market 1.0082 0.0000 SMB -0.0711 0.7273 HML -07147 0.0039 Ftest 40.572 0.0000 R2 0.5359 St.Error 1.0506 Risk free rate in the economy is 0.006. Apple has a market risk premium 0.0836 (rates are in 970, no need to change them). (a) (10 pts) Is Apple fairly pced according to the APT model? (b) (5 pts) In what percentage does the above model explain the variation of Apple daily stock returns? (c) (15 pts) Are there any statistically insignicant factors from the regression result? What would be the expected return of Apple if you exclude those factors from the analysis

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts