Question: Please help me with the following question based on the given article, there is only one option that is correct. Please also explain why is

Please help me with the following question based on the given article, there is only one option that is correct. Please also explain why is the option correct and other options are wrong.

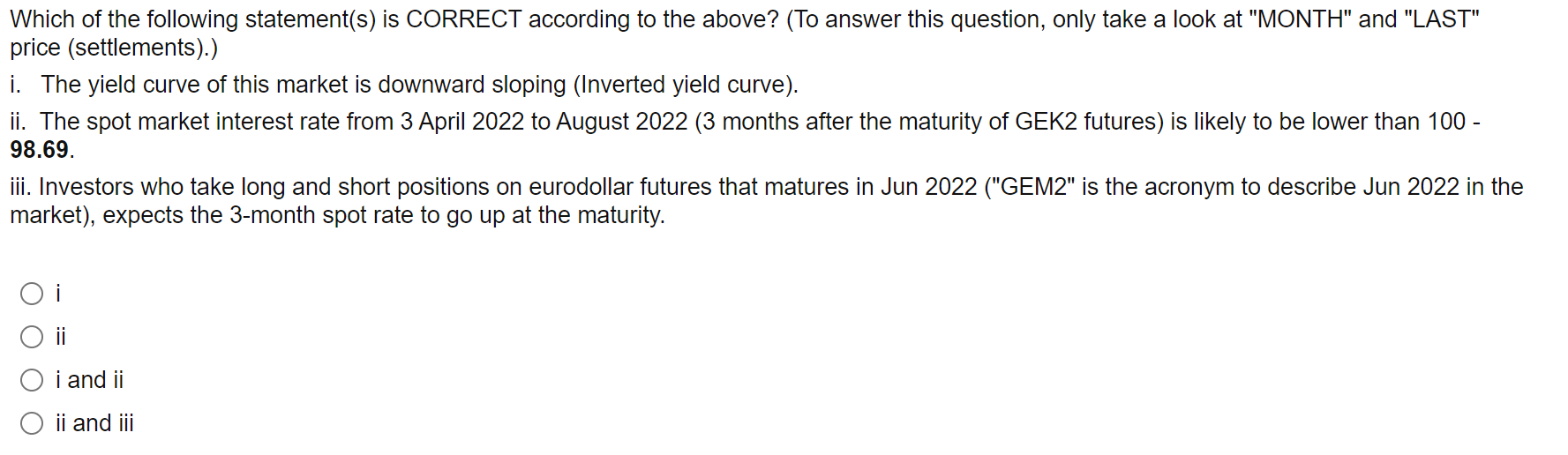

Eurodollar typically indicates U.S. dollar deposits outside of the U.S. (In nancial markets, "Euro" often indicates foreign currency denominated interest rate or assets. For example, eurobonds are bonds that are issued in foreign currency [foreign often indiates U.S. dollars]). In the meantime, futures contracts, just like fomrard contracts (i.e. "forward" interest rate), are contracts of which actual transactions occur (exchange of cash flow) in the future. The difference between forward contracts and futures contracts is that futures contracts are standardized and traded publicly in exchanges where fen/yard contracts are usually private contracts between nancial institutions (as it is not standardized, fon/vard contracts can be exible in terms of size of the deal. terms, etc but it will have higher level of counterparty risk as these are not managed by public exchanges). The following table is price quotes on Eurodollarfutures. It can be deemed as futures contracts on short-term (3-month) zero-coupon bonds (long position on a bond ~ lending). If you take a long position on an Eurodollarfutures contract, it will be as if you will have to purchase the underlying 3-month zero-coupon bond at the contract price below (refer to "LAST") at the maturity (refer to "MONTH"). Price quote convention is Principal - 3-month Yield (3-month Interest). For example, if the yield (Interest) is 1.5%, the quote of the futures contract will be 100 (%) 1.5(/a) = 98.5. If the 3month spot rate becomes 1%, thus the price quote becomes 99.0, this difference (times the contract size) will be the profit of the investors who took long positions on this contract. This is one way of managing interest rate risk in short-term borrowing and lending. EURODOLLAR FUTURES - QUOTES AUTO- R EFRESH I5 OFF Last Updated 03 Apr 2022 05 5343 AM CT Market data is delayed by at (east 70 mrnutes APR 2922 GEJ2 .u 99. 99 ,3, 9975 t a. 91%) 9a 9975 93. 9975 99. 9925 9e. 9e 36. 611 22122322 Ei'l .1| 95.69 49.935 (-9.94%) 98.725 98.71 98.71 98.68 6,684 3322922 m ..| 99.42 a.95 (-6.85%) 99.47 99.45 99.45 93.49 153,399 g'zzm m .11 99.195 43.665 (-9.97%) 93.25 99.19 99.21 99.17 5.449 (* Fed Funds rate futures is similar to Eurodollar futures.) ** Month: Maturity. Last: Last closing price (as of 3 April 2022). (HINT: refer to the relationship between spot rates and fonrvard rates in the lecture note.) Which of the following statement(s) is CORRECT according to the above? (To answer this question, only take a look at "MONTH" and "LAST" price (settlements).) i. The yield curve of this market is downward sloping (Inverted yield curve). ii. The spot market interest rate from 3 April 2022 to August 2022 (3 months after the maturity of GEK2 futures) is likely to be lower than 100 - 98.69. iii. Investors who take long and short positions on eurodollar futures that matures in Jun 2022 ("GEM2" is the acronym to describe Jun 2022 in the market), expects the 3-month spot rate to go up at the maturity. O i 0 ii 0 iand ii 0 ii and

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!