Question: please help me with the question (D),(E),(F),(G) Suppose that the risk-free rate is 6.80% per annum and that the market risk premium is 8.30% per

please help me with the question (D),(E),(F),(G)

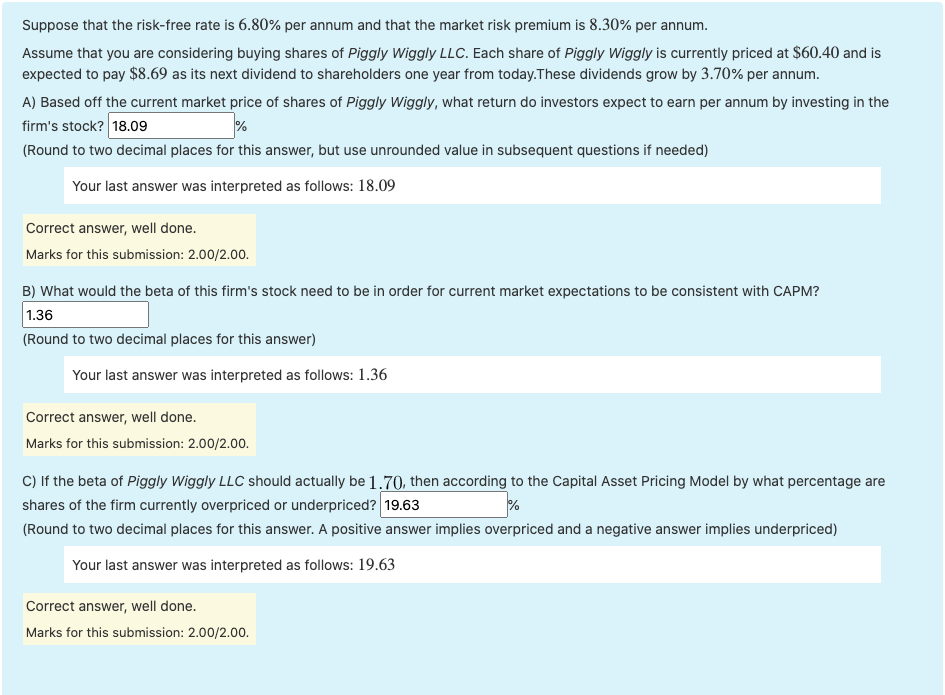

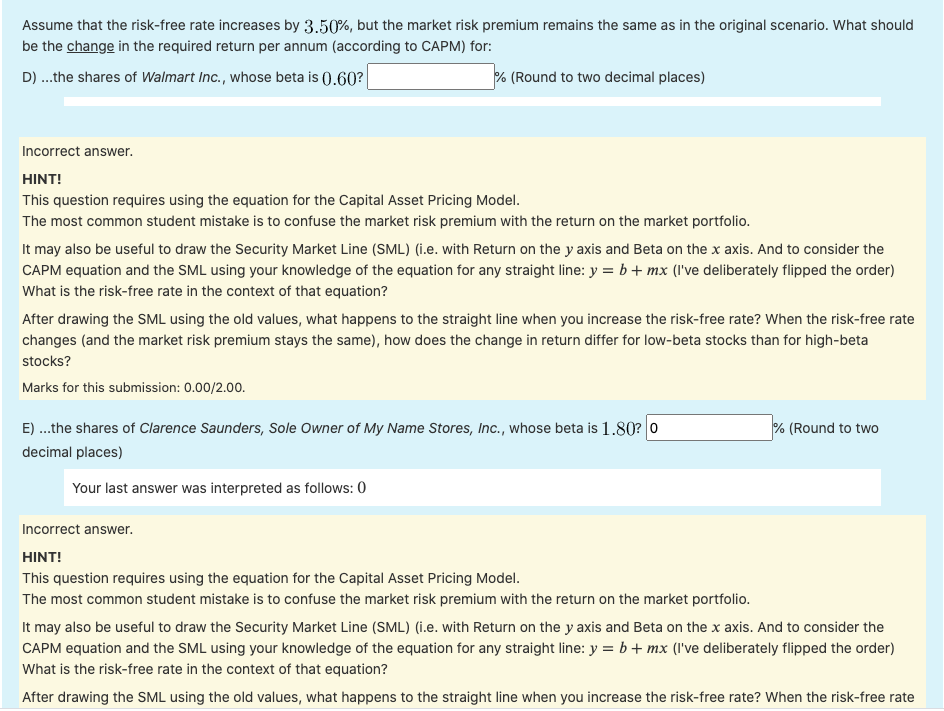

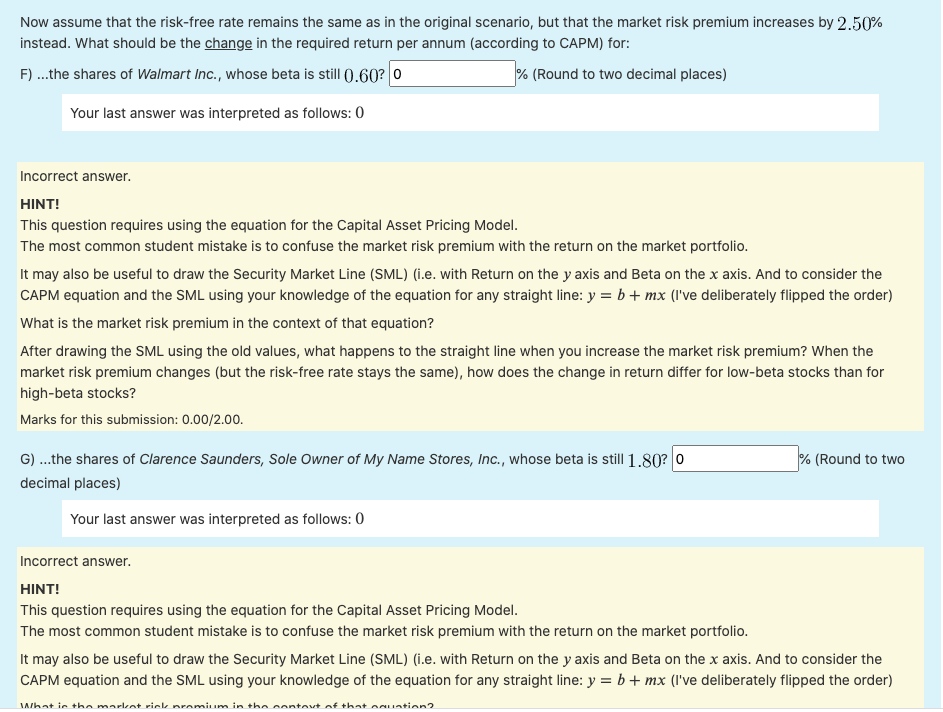

Suppose that the risk-free rate is 6.80% per annum and that the market risk premium is 8.30% per annum. Assume that you are considering buying shares of Piggly Wiggly LLC. Each share of Piggly Wiggly is currently priced at $60.40 and is expected to pay $8.69 as its next dividend to shareholders one year from today.These dividends grow by 3.70% per annum. A) Based off the current market price of shares of Piggly Wiggly, what return do investors expect to earn per annum by investing in the firm's stock? 18.09 % (Round to two decimal places for this answer, but use unrounded value in subsequent questions if needed) Your last answer was interpreted as follows: 18.09 Correct answer, well done. Marks for this submission: 2.00/2.00. B) What would the beta of this firm's stock need to be in order for current market expectations to be consistent with CAPM? 1.36 (Round to two decimal places for this answer) Your last answer was interpreted as follows: 1.36 Correct answer, well done. Marks for this submission: 2.00/2.00. C) If the beta of Piggly Wiggly LLC should actually be 1.70, then according to the Capital Asset Pricing Model by what percentage are shares of the firm currently overpriced or underpriced? 19.63 % (Round to two decimal places for this answer. A positive answer implies overpriced and a negative answer implies underpriced) Your last answer was interpreted as follows: 19.63 Correct answer, well done. Marks for this submission: 2.00/2.00. Assume that the risk-free rate increases by 3.50%, but the market risk premium remains the same as in the original scenario. What should be the change in the required return per annum (according to CAPM) for: D)...the shares of Walmart Inc., whose beta is 0.60? % (Round to two decimal places) Incorrect answer. HINT! This question requires using the equation for the Capital Asset Pricing Model. The most common student mistake is to confuse the market risk premium with the return on the market portfolio. It may also be useful to draw the Security Market Line (SML) (i.e. with Return on the y axis and Beta on the x axis. And to consider the CAPM equation and the SML using your knowledge of the equation for any straight line: y = b + mx (I've deliberately flipped the order) What is the risk-free rate in the context of that equation? After drawing the SML using the old values, what happens to the straight line when you increase the risk-free rate? When the risk-free rate changes and the market risk premium stays the same), how does the change in return differ for low-beta stocks than for high-beta stocks? Marks for this submission: 0.00/2.00. % (Round to two E) ...the shares of Clarence Saunders, Sole Owner of My Name Stores, Inc., whose beta is 1.80? 0 decimal places) Your last answer was interpreted as follows: 0 Incorrect answer. HINT! This question requires using the equation for the Capital Asset Pricing Model. The most common student mistake is to confuse the market risk premium with the return on the market portfolio. It may also be useful to draw the Security Market Line (SML) (i.e. with Return on the y axis and Beta on the x axis. And to consider the CAPM equation and the SML using your knowledge of the equation for any straight line: y = b + mx (I've deliberately flipped the order) What is the risk-free rate in the context of that equation? After drawing the SML using the old values, what happens to the straight line when you increase the risk-free rate? When the risk-free rate Now assume that the risk-free rate remains the same as in the original scenario, but that the market risk premium increases by 2.50% instead. What should be the change in the required return per annum (according to CAPM) for: F) ...the shares of Walmart Inc., whose beta is still 0.60? O % (Round to two decimal places) Your last answer was interpreted as follows: 0 Incorrect answer. HINT! This question requires using the equation for the Capital Asset Pricing Model. The most common student mistake is to confuse the market risk premium with the return on the market portfolio. It may also be useful to draw the Security Market Line (SML) (i.e. with Return on the y axis and Beta on the x axis. And to consider the CAPM equation and the SML using your knowledge of the equation for any straight line: y = b + mx (I've deliberately flipped the order) What is the market risk premium in the context of that equation? After drawing the SML using the old values, what happens to the straight line when you increase the market risk premium? When the market risk premium changes (but the risk-free rate stays the same), how does the change in return differ for low-beta stocks than for high-beta stocks? Marks for this submission: 0.00/2.00. % (Round to two G) ...the shares of Clarence Saunders, Sole Owner of My Name Stores, Inc., whose beta is still 1.80? O decimal places) Your last answer was interpreted as follows: 0 Incorrect answer. HINT! This question requires using the equation for the Capital Asset Pricing Model. The most common student mistake is to confuse the market risk premium with the return on the market portfolio. It may also be useful to draw the Security Market Line (SML) (i.e. with Return on the y axis and Beta on the x axis. And to consider the CAPM equation and the SML using your knowledge of the equation for any straight line: y = b + mx (I've deliberately flipped the order) What in the marlent riele ramium in the contact of that caustian

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts