Question: Please help solve P8-3A I have attached a sample answer sheet thank you accounts receivable indicates that estimated bad debts are $46,000, (d) Compute the

Please help solve P8-3A

I have attached a sample answer sheet

thank you

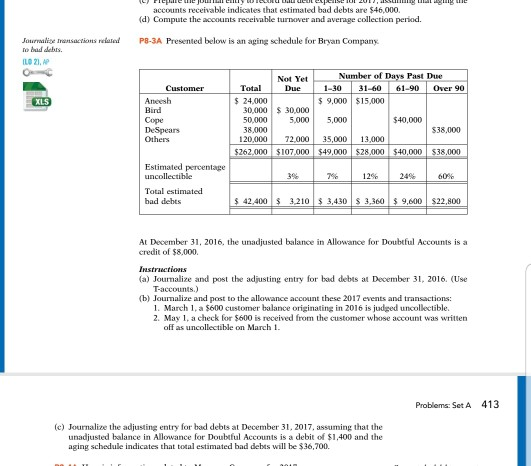

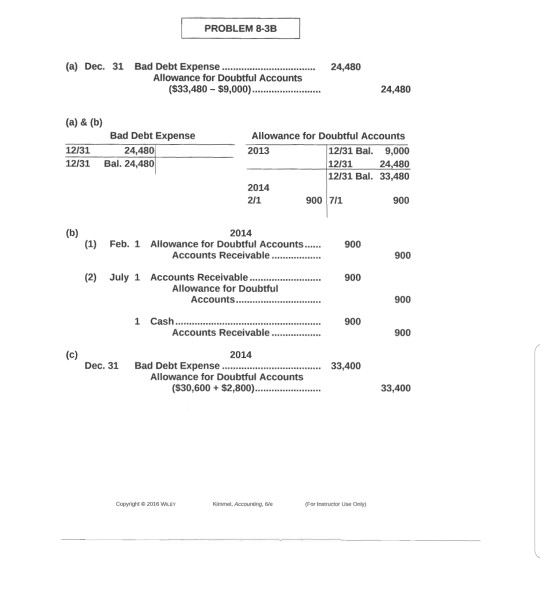

accounts receivable indicates that estimated bad debts are $46,000, (d) Compute the accounts receivable turnover and average collection periad. ouralie Iransactions r ro bad dets. P8-3A Presented below is an aging schedule for Bryan Company LO 21, AP Number of Days Past Due Not Yet Due Total 1-30 31-60 61-90 Over 90 24,000 9,000 $15,000 Bird Cope 30,00030,000 50,0005,000 38,000 5,000 $40,000 $38,000 Others 120,00072,000 35,00013,000 8,000 $262,000 $107,000 000 $38,000 3% 7% 12% 24% 60% Total estimated bad dehts 42,4003,2103,430 3,3609,600 $22,800 At December 31, 2016, the unadjusted balance in Allowance for Doubeful Accounts is a credit of $8,000. (a) Journalize and post the adjusting entry for bad debts at December 31, 2016. (Use T-accounts.) (b) Journalize and post to the allowance account these 2017 events and transactions: 1. March 1, a $600 customer balance originating in 2016 is judged uncollectible. 2. May1, a check for $600 is received from the customer whose account was written off as uncollectible on March 1 Problems: StA 413 (c) Journalize the adjusting entry for bad debts at December 31, 2017, assuming that the unadjusted balance in Allowance for Doubtful Accounts is a debit of $1,400 and the aging schedule indicates that total estimated bad debts will be $36,700. PROBLEM 8-3B (a) Dec. 31 Bad Debt Expense24,480 Allowance for Doubtful Accounts ($33,480 $9,000) (a) & (b) Bad Debt Expense Allowance for Doubtful Accounts 2013 12/31 12/31 Bal. 12/31 Bal. 9,000 12/3124,480 12131 Bal. 33,480 24, 2014 211 900 7/1 900 2014 900 (2) July 1 Accounts Receivable .900 Allowance for Doubtful 1 Cash 900 900 2014 Dec. 31 Bad Debt Expense33,400 Allowance for Doubtful Accounts ($30,600 $2,8

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts