Question: please help Tax Drill - Section 1244 Complete the following statements regarding worthless Securities and $ 1244 stock. If a security that is a capital

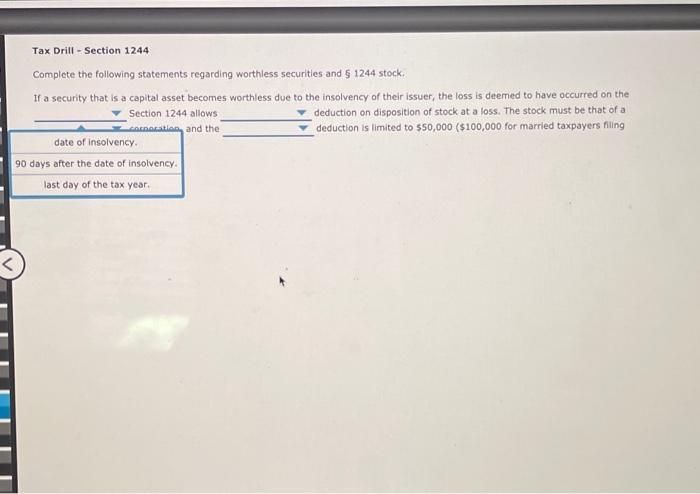

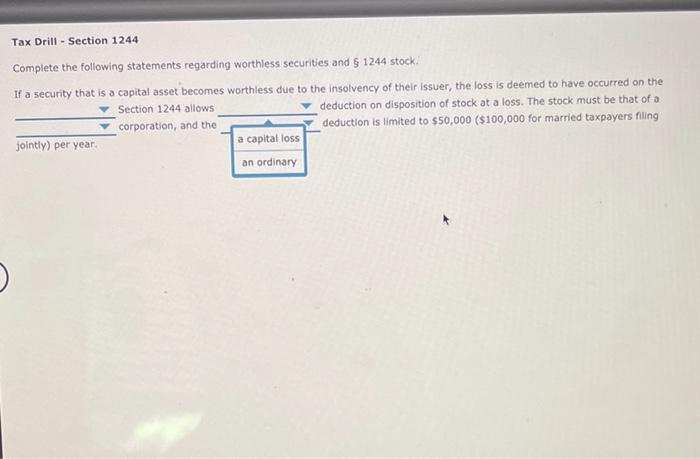

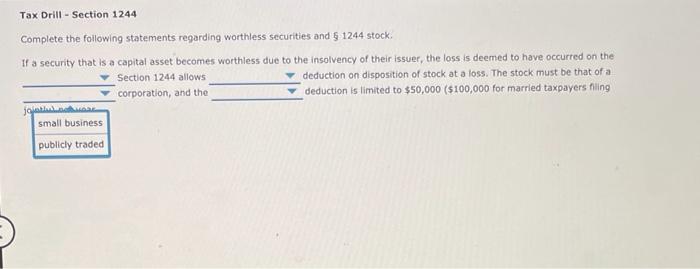

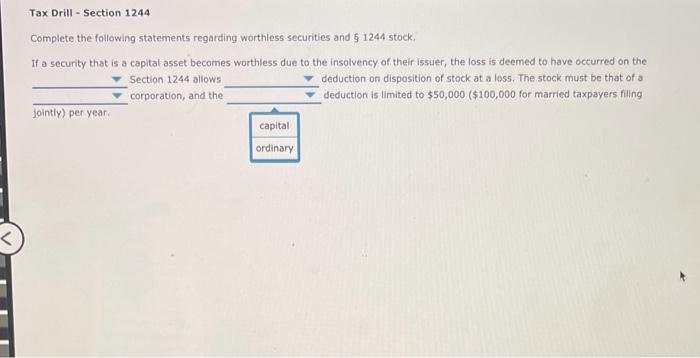

Tax Drill - Section 1244 Complete the following statements regarding worthless Securities and $ 1244 stock. If a security that is a capital asset becomes worthless due to the Insolvency of their issuer, the loss is deemed to have occurred on the Section 1244 allows deduction on disposition of stock at a loss. The stock must be that of a and the deduction is limited to $50,000 ($100,000 for married taxpayers filing date of insolvency 90 days after the date of insolvency. last day of the tax year Tax Drill - Section 1244 Complete the following statements regarding worthless securities and $ 1244 stock. If a security that is a capital asset becomes worthless due to the Insolvency of their issuer, the loss is deemed to have occurred on the Section 1244 allows deduction on disposition of stock at a loss. The stock must be that of a corporation, and the deduction is limited to $50,000 ($100,000 for married taxpayers fling jointly) per year a capital loss an ordinary Tax Drill - Section 1244 Complete the following statements regarding worthless securities and 1244 stock If a security that is a capital asset becomes worthless due to the insolvency of their issuer, the loss is deemed to have occurred on the Section 1244 allows deduction on disposition of stock at a loss. The stock must be that of a corporation, and the deduction is limited to $50,000 ($100,000 for married taxpayers filing small business publicly traded Tax Drill - Section 1244 Complete the following statements regarding worthless securities and 1244 stock If a security that is a capital asset becomes worthless due to the insolvency of their issuer, the loss is deemed to have occurred on the Section 1244 allows deduction on disposition of stock at a loss. The stock must be that of a corporation, and the deduction is limited to $50,000 ($100,000 for married taxpayers filing jointly) per year capital ordinary

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts